Steering Through Headwinds, Taking Initiative: How Founders Can Navigate Macroeconomic and Capital Market Trends | Ronghui Practical Insights

Ronghui Macro Strategy Quarterly Series — Event No. 1

Since the start of the year, entrepreneurs have faced heightened uncertainty — whether from the ongoing pandemic, geopolitical friction weighing on the global macroeconomy, or volatility rippling through capital markets.

What trajectory will the global and Chinese economies follow in 2022? How have recent shifts in secondary markets affected startups? And amid all this flux, how should founders formulate their strategic plans for the year?

Recently, Gaorong Ventures hosted its Macro Strategy Season series of events, partnering with Futu to help portfolio companies look outward at macro trends and inward at new strategic leverage points — covering macroeconomics, military strategy applied to business, strategic planning methodologies, and government economic governance logic.

At the inaugural online session, Tan Zhuo, Director of the Macro Research Institute at China Merchants Bank, and Wu Biwei, Senior Partner at Futu, drew on the latest economic data and capital market developments to help entrepreneurs cut through complex headlines to the underlying logic — and identify anchor points for strategic thinking.

Below is an edited transcript of their remarks:

PART 1

A "Stagflation-Lite" Lens

on the Global Economic Outlook

I. The Global Macro Theme: The Evolution of "Stagflation-Lite"

The evolution of a "stagflation-lite" configuration is the central thread for understanding the current global macroeconomy.

Stagflation, a portmanteau of stagnation and inflation, describes the simultaneous occurrence of economic contraction and rising prices — stagnation meaning flat or negative growth, inflation meaning climbing price levels.

For macro policymakers, stagflation represents a highly undesirable state. It constrains policy maneuverability, forcing decision-makers into a dilemma: stimulating growth requires expansionary measures, yet already-elevated inflation would further squeeze market participants on the cost side; controlling inflation demands tightening, which only deepens the pain for an already-contracting economy.

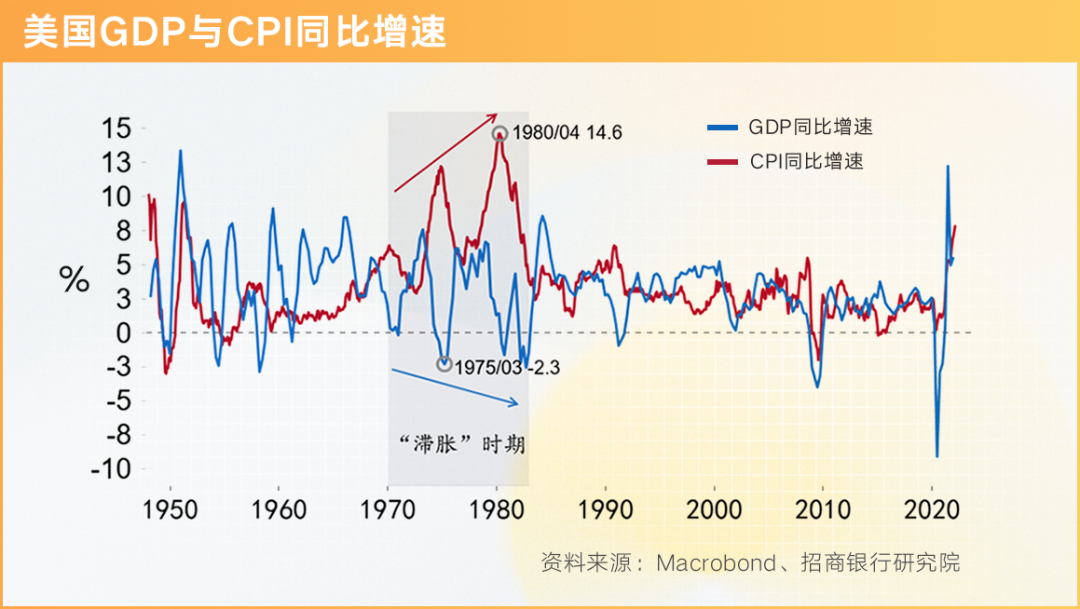

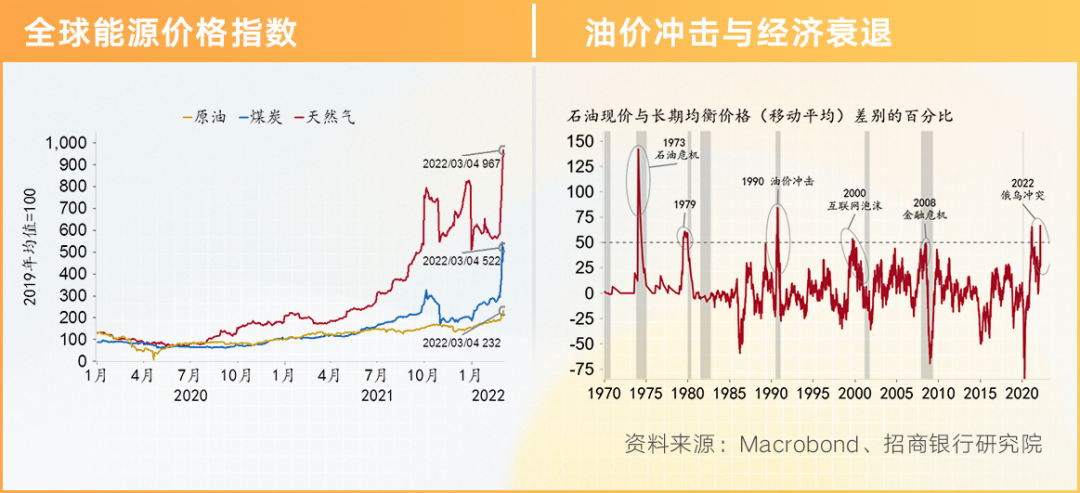

Why characterize the current global economy as "stagflation-lite"? Because while overall global growth remains relatively high — partly a low-base effect — inflation is climbing persistently. Though not yet in negative growth territory, actual economic performance falls far short of expectations. The Russia-Ukraine conflict, bringing energy and food shortages, supply chain disruptions, and financial market turbulence, has further marked down growth and marked up inflation.

From a global perspective, the US, Europe, and China have diverged noticeably in their macroeconomic situations. The primary challenge for the US and Europe is inflation, though endogenous growth momentum remains relatively robust. China faces downward growth pressure but has inflation relatively under control.

II. The US Macroeconomic Situation: High Inflation Has Become the Biggest Headwind

1. The "Stagnation" Side: Supply-Demand Gap Closing Endogenously

Looking at the endogenous drivers of US growth, demand remains vigorous while supply constraints have eased substantially. The global pandemic hit an inflection point in mid-February, and COVID's drag on the US and European economies has weakened. At the March Fed meeting, one particularly notable shift was the Fed's assessment that the Russia-Ukraine conflict has replaced COVID-19 as the biggest source of uncertainty for the US economy.

On the demand side, goods consumption in developed economies recovered first after the pandemic shock, with the US seeing particularly large expansion. This was driven mainly by the most aggressive fiscal and monetary stimulus of any major economy. By 2021, overall US consumption had recovered to pre-pandemic levels, with services consumption significantly suppressed while goods consumption far exceeded pre-pandemic levels. Looking ahead to 2022, we expect US demand to remain strong, supported by substantial government transfer payments during the pandemic that left nominal incomes and disposable wealth well above pre-COVID levels, building up excess savings. On the consumption mix, as the economy normalizes, demand should shift noticeably from goods to services.

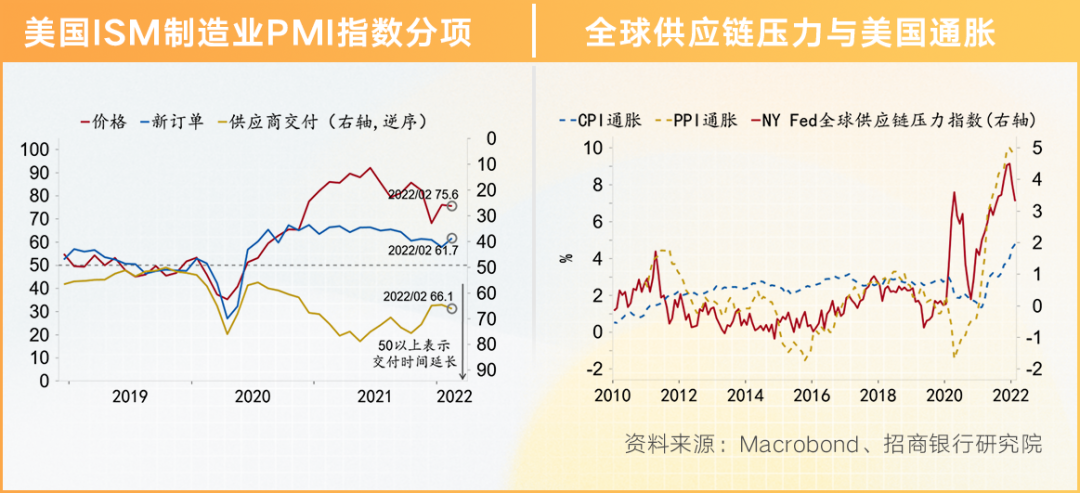

On the supply side, the US faced capacity, employment, and logistics constraints over the past year, with overall capacity utilization below potential, depleting inventories across industries. But entering 2022, as supply chain pressures ease, labor markets heal, and high inflation marginally relaxes "decarbonization" constraints, the US supply-demand gap may close endogenously. The Fed's global supply chain pressure index has peaked and is now in retreat. The US ISM manufacturing PMI also shows the supplier deliveries index declining — meaning shorter delivery times. Of course, the Russia-Ukraine conflict could introduce fresh uncertainty into global supply chain recovery.

2. The "Inflation" Side: Pressure Easing at the Margin, Expected to Peak in Q2

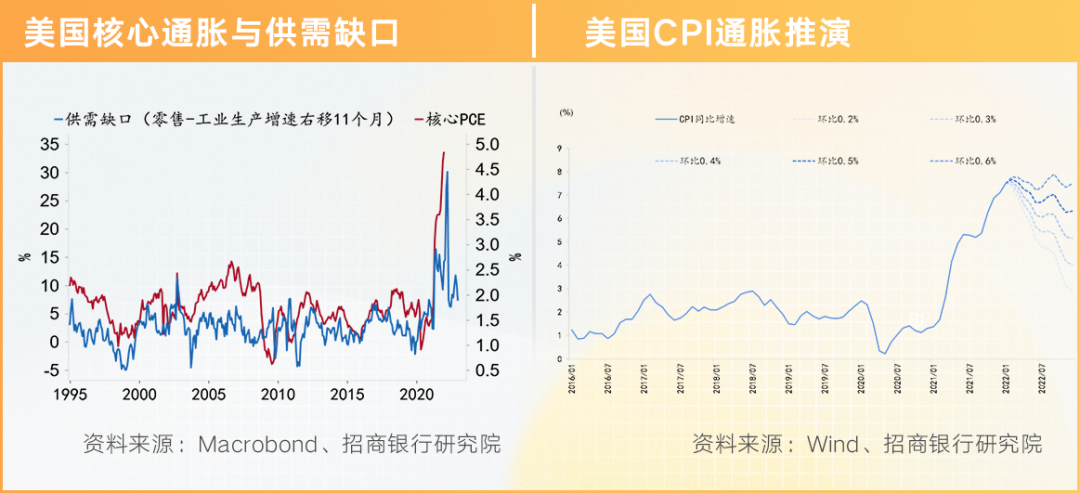

US inflation's evolution through the pandemic has unfolded in three phases. Phase one: early pandemic, when economic activity froze and consumption saw both volumes and prices fall. Phase two: starting June 2020, as fiscal stimulus took hold and real disposable income growth turned positive, consumption rebounded in a V-shape — "volumes and prices rising together." Compared to the prolonged consumption recovery after the subprime crisis, this rebound was remarkably rapid. Phase three: since April 2021, as the US supply-demand gap widened, inventories fell and shortages emerged, pushing prices up sharply — the current "volumes down, prices up" pattern.

At present, US inflation has shifted from concentrated structural increases in certain goods categories to broad-based "universal inflation." Transportation has become the biggest CPI contributor, hit by chip shortages and energy price spikes; home prices and rents have risen rapidly; and food and other necessities have seen elevated growth. Under the Russia-Ukraine conflict, US CPI year-on-year inflation hit 7.9% in February, a nearly 40-year high, with international commodity prices for oil, non-ferrous metals, and agricultural products surging.

This is the main contradiction in the US economy and the top target of US macro policy. Historically, high oil prices and economic recessions have gone hand in hand.

We expect US CPI has not yet peaked and will continue rising for another month or two before entering a downtrend around mid-year. The US supply-demand gap leads core PCE with a clear lag. As global supply chain pressures ease and the US supply-demand gap has already started to narrow, core PCE and CPI should follow downward.

But the US is also watching for a "wage-price spiral." University of Michigan surveys show US consumer inflation expectations continuing to rise; if households' inflation expectations ratchet up and "everyone expects inflation," workers will demand higher wages, forcing firms to raise prices to pass through costs — a vicious cycle of spiraling wages and prices. This is an important reason for the Fed's monetary tightening. However, US average hourly earnings year-on-year did not rise further in February, suggesting the situation remains relatively contained.

3. Fed Monetary Policy: Accelerating Tightening

Since late last year, the Fed's monetary policy stance has shifted hawkish in lurches. The March 17 policy announcement showed very large changes in stance. In Q4 2021, the median Fed dot plot projected 3 rate hikes; the latest median projection is 7. An important reason is that the Russia-Ukraine conflict could push US inflation even higher.

Over the past year, the Fed serially misjudged inflation — partly because forecasting difficulty rose non-linearly under pandemic conditions, and partly because the Fed hoped to "tolerate" inflation to create favorable conditions for employment and economic recovery.

But the stance has now reversed: high inflation is seen as the biggest threat to US economic recovery, and curbing inflation has become consensus among macro policymakers. High inflation is driving the Fed to accelerate monetary normalization in three steps — tapering asset purchases, gradual rate hikes, and balance sheet reduction. As the saying goes, "from luxury to frugality is hard"; the Fed's balance sheet reduction may prove difficult, and the balance sheet will likely remain far above pre-pandemic levels.

III. China's Macroeconomic Trajectory: Climbing Uphill, Structural Adjustment

1. The "Stagnation" Side: Investment Will Become the Main Lever for "Stabilizing Growth"

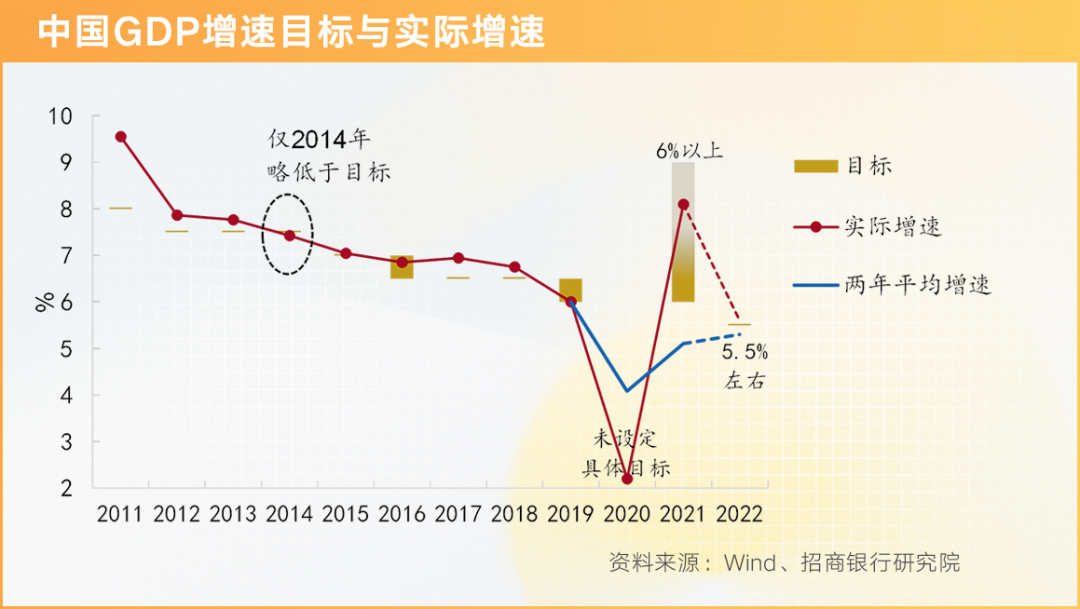

This year's government work report set a 2022 GDP growth target of 5.5% — highly significant for all market participants.

This target sits at the upper bound of market expectations and is well above the 4.0% year-on-year growth seen in Q4 last year. The target first signals resolve to "stabilize growth" and "stabilize expectations"; it also serves the 14th Five-Year Plan's "doubling" goal — namely, doubling China's GDP by 2035 compared to 2020.

We see the government aiming to use proactive policies to push the economy back toward its potential growth rate. This target is extremely challenging and requires comprehensive, forceful policy responses spanning fiscal policy, monetary policy, industrial policy, and dual-carbon policy. We are confident it will be achieved. Looking at China's historical GDP targets versus actual outcomes, targets are highly likely to be met; the Chinese government has a track record of "doing what it says."

But achieving 5.5% growth this year faces enormous pressure. Looking at the three engines of growth: "stabilizing exports" has become harder — as the global pandemic normalizes, goods demand from abroad faces marginal weakening, though the Russia-Ukraine conflict provides some short-term resilience. Consumption remains constrained by COVID outbreaks. With exports and consumption both constrained, investment will become the main lever for "stabilizing growth."

1) Exports: Downward Trend, Volume-Price Divergence

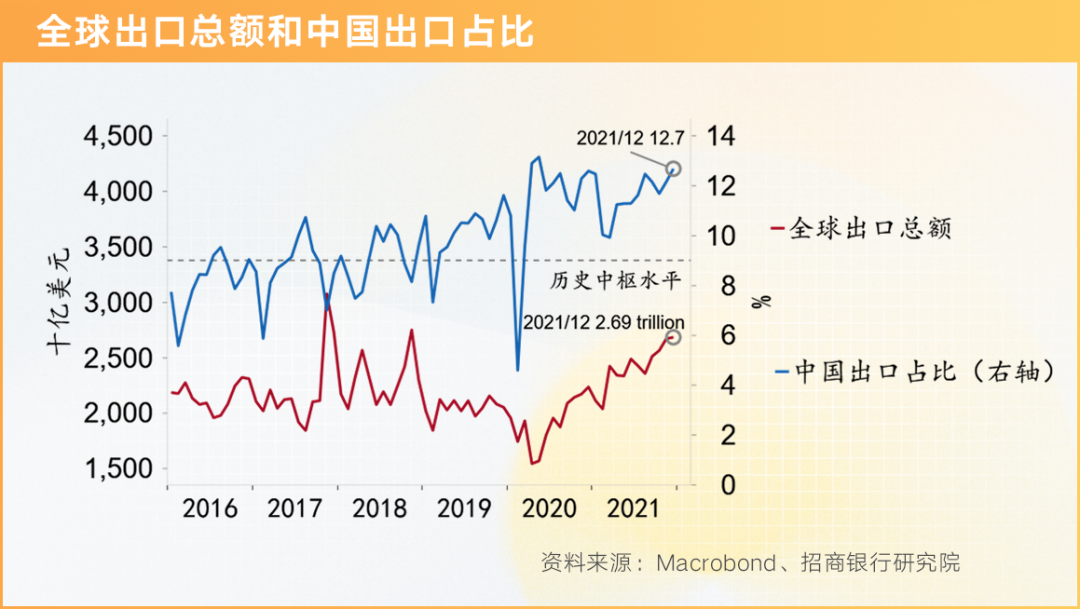

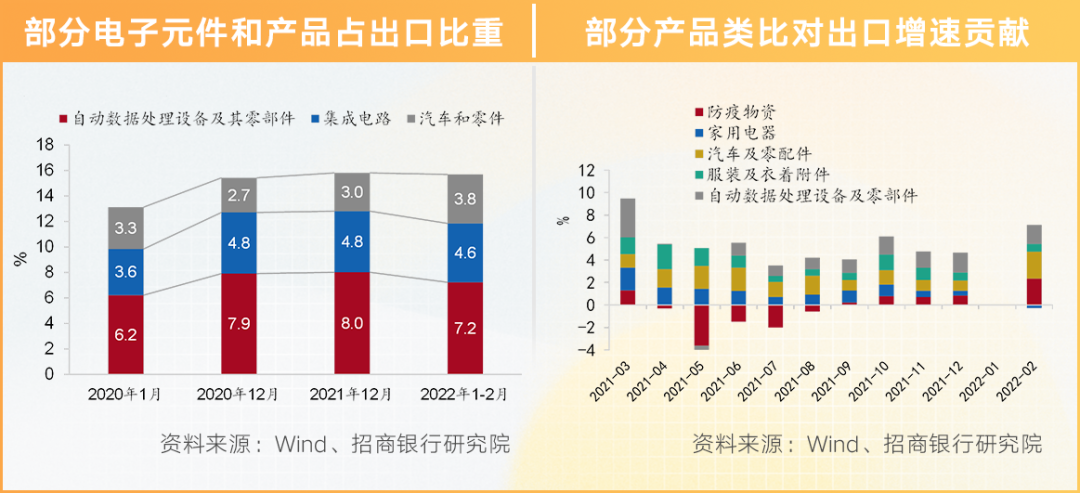

In 2021, Chinese exports remained buoyant, driven by a "double dividend." On one hand, US and European goods consumption spilled over abroad, keeping global export values high — the pie grew larger. Meanwhile, because China controlled the pandemic effectively, China's share of global exports was significantly above historical averages — China got a bigger slice.

But looking ahead, Chinese exports in 2022 face production and profit concerns. On production, order losses have led to rising inventory pressures, with SMEs particularly hard-hit; chip shortages have disrupted downstream industries like autos and consumer electronics. Terms of trade have also squeezed profits, with import prices rising far faster than export prices.

We anticipate that 2022 will see export momentum decline with volume-price divergence. Dollar-denominated export growth will slow due to narrowing overseas supply-demand gaps and the strong RMB exchange rate. Structurally, diverging short-term and long-term foreign demand will shift export composition. Long-term positive trends in digitalization, automation, and new energy vehicles will support exports of related electronics and intermediate goods.

However, the Russia-Ukraine conflict may flatten the slope of China's export decline, with substitution effects potentially exceeding expectations.

2) Real Estate: Measured Policy Easing, "Soft Landing" Achievable This Year

Real estate holds a foundational position in China's national economy. Land transfer fees and other real estate-related tax revenues amount to over 90% of local governments' general public budget revenues.

Therefore, under the principle that "housing is for living in, not speculation," the tone of "stabilizing land prices, housing prices, and expectations" remains unchanged — but policy will be appropriately relaxed, with commitments to "timely" study and propose "forceful and effective" measures to prevent and defuse real estate risks. On the household side, this involves purchase restrictions, mortgage rates, and loan quotas; on the developer side, adjustments to presale fund supervision and loan categories subject to the "three red lines" framework.

We expect the real estate market to achieve a "soft landing" within the year, though the rebound slope may be limited given relatively weak expectations.

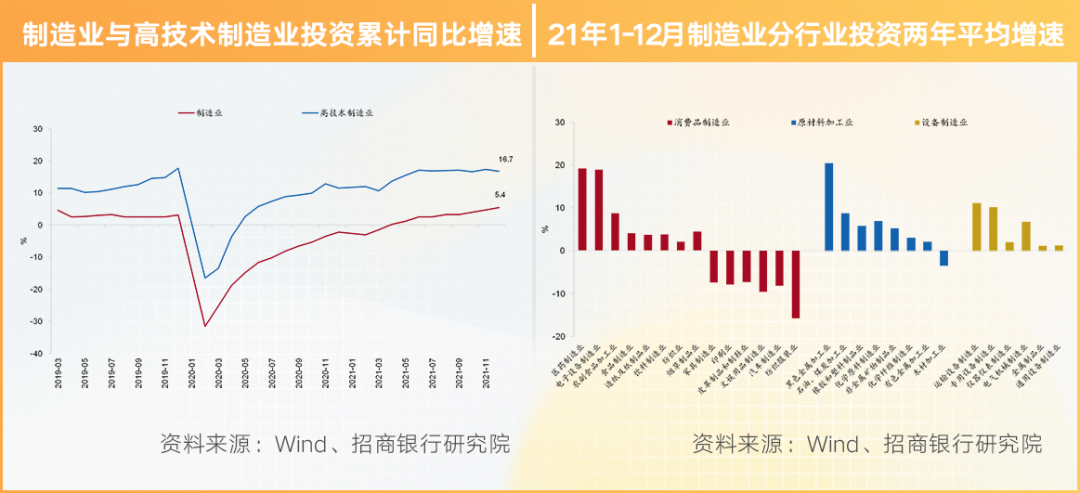

3) Manufacturing: Strengthening Momentum

In 2021, Chinese manufacturing investment maintained high growth. High-tech industries saw year-on-year growth of 22.2% for January-December, with a two-year average of 16.7%.

We expect 2022 manufacturing investment growth to receive clear policy support. Policy support for new-kinetic-energy enterprises is continuous and consistent, including structural monetary policy and tax cuts, with directed support for high-tech manufacturing and green transition enterprises.

Traditional manufacturing investment is also seeing strengthened momentum this year, as "dual-carbon" constraints ease at the margin.

4) Infrastructure Investment: Becoming the "Stabilizing Growth" Lever

Under "triple pressures," infrastructure will be the focal point for "stabilizing growth" and expanding investment. In January-February this year, infrastructure investment rebounded sharply to 8.6% growth. Fiscal acceleration in late last year meant funds and physical project volumes carried into early this year.

We are relatively optimistic on 2022 infrastructure investment growth. On one hand, funding is ample and front-loaded; meanwhile, major project plans for 2022 were issued and started early, with both traditional and new infrastructure contributing. But full-year upside remains constrained, with growth likely front-loaded and tapering later.

5) Consumption: Slow Recovery Continues

On consumption, we expect 2022 to maintain a slow recovery trajectory, constrained by several factors. First, income pressure on market participants — including overall weak household income recovery; fiscal pressure on some local governments highly dependent on land transfer fees; and squeezed consumption by social groups as some industries come under pressure.

Second, COVID resurgences and the "double reduction" policy have constrained services consumption recovery.

Finally, divergence within discretionary consumer goods continues — for example, real estate weakness has constrained furniture and appliance consumption, while new-economy-related goods show strong growth.

2. The "Inflation" Side: Inflation Slowing

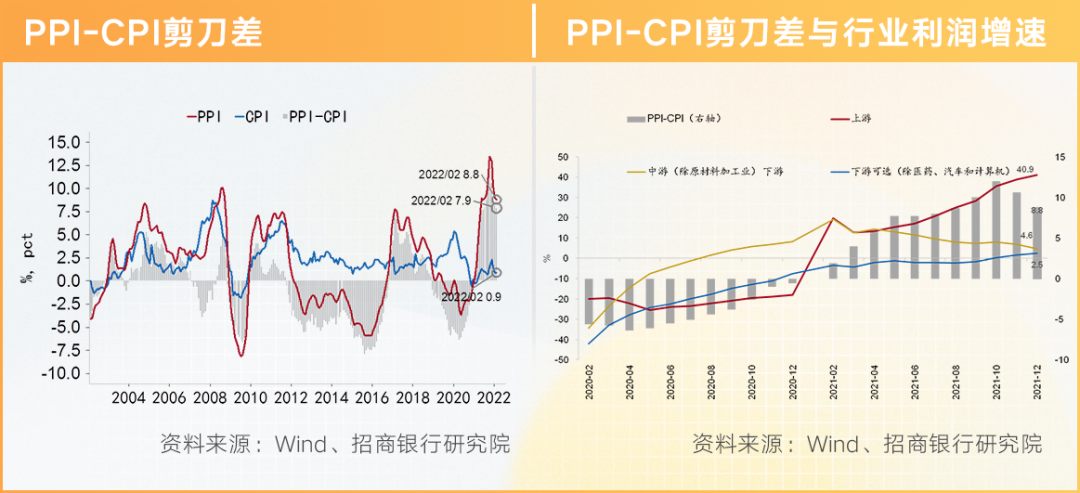

China's overall inflation situation remains controllable. Last year saw pronounced structural inflation, with rapid industrial goods price increases. Under the baseline scenario where domestic supply-stabilization and price-control policies take effect and international commodity prices retreat at the margin, PPI year-on-year growth should steadily decline this year.

On the CPI side, energy prices have relatively muted impact on China's CPI, so CPI inflation should rise only moderately.

With PPI inflation declining and CPI rising moderately, the profit divergence between upstream and downstream enterprises should converge as the PPI-CPI scissors gap narrows. Last year upstream enterprises saw high profit growth while midstream and downstream profits were weak; we expect this situation to improve at the margin this year.

3. Fiscal and Monetary Policy: Greater Force and Efficiency, Appropriately Front-Loaded

On fiscal policy, China was in a "window period with relatively small growth-stabilization pressure" in the first half of last year, with fiscal policy "prudently proactive" focused on "preventing risks" and "stabilizing leverage." As economic downward pressure mounted in the second half, fiscal proactivity rose markedly, creating a "rear-loaded fiscal" pattern.

For 2022, we expect proactive fiscal policy to "enhance efficacy." This year's fiscal policy includes numerous special arrangements; the overall proactivity is in fact higher than last year, including 2.33 trillion yuan from transferred funds and carried-over balances, 1.65 trillion yuan in profits handed over by specific institutions, fiscal expenditure expansion of over 2 trillion yuan, and 2.5 trillion yuan in tax cuts and fee reductions, with both tax cuts and rebates. The rhythm is also front-loaded, with force applied early.

Monetary policy will also step up implementation. Under "triple pressures," China's monetary policy has tilted further toward "stabilizing growth," supporting the real economy through stabilizing aggregate volume, adjusting structure, and reducing costs. Meanwhile, structural policy has grown more important, with increased support for small and micro enterprises, technological innovation, and green development — "actively tapping (small and micro enterprises') reasonable financing needs," elevating support for small and micro enterprises to the level of "stabilizing enterprises and preserving employment, which helps stabilize the macroeconomic foundation."

PART 2

Capital Market Pulse:

Where Should Corporate Financing and IPO Strategy Go?

I. Internal and External Causes of Recent Capital Market Volatility

Recent market volatility has been extremely intense — the most I've encountered in my career.

From February-March 2021, when Chinese concept stocks were at historical highs, to this February-March, the change can only be described as "seas turned into mulberry fields." Since last February-March, many companies have seen their market values cut in half. What's driving this?

On internal causes, mainly a series of events and policies since 2020 have made capital market investors feel uncertain, leading them to pivot toward other markets and assets.

External causes include three main factors. First, Fed rate hikes — the first since December 2018 — with the dollar and US stock indices rising accordingly.

The second external factor is the Holding Foreign Companies Accountable Act, requiring foreign companies listed in the US to submit audit working papers, with potential delisting risk if unable to comply for three years. Particularly on March 8, when the SEC placed five companies on the provisional list under the Act, it triggered a degree of market panic.

Although some companies have already done secondary or dual-primary listings in Hong Kong, because some investors can only invest in US markets and because of Hong Kong's liquidity discount, Hong Kong stocks have also fallen.

But we see Chinese and US regulators actively communicating on this issue; I am optimistic that it can be resolved.

The third external factor is the sudden Russia-Ukraine war, causing international financial market volatility and risk-averse sentiment among long-term capital.

II. How to Formulate IPO and Financing Strategy in 2022

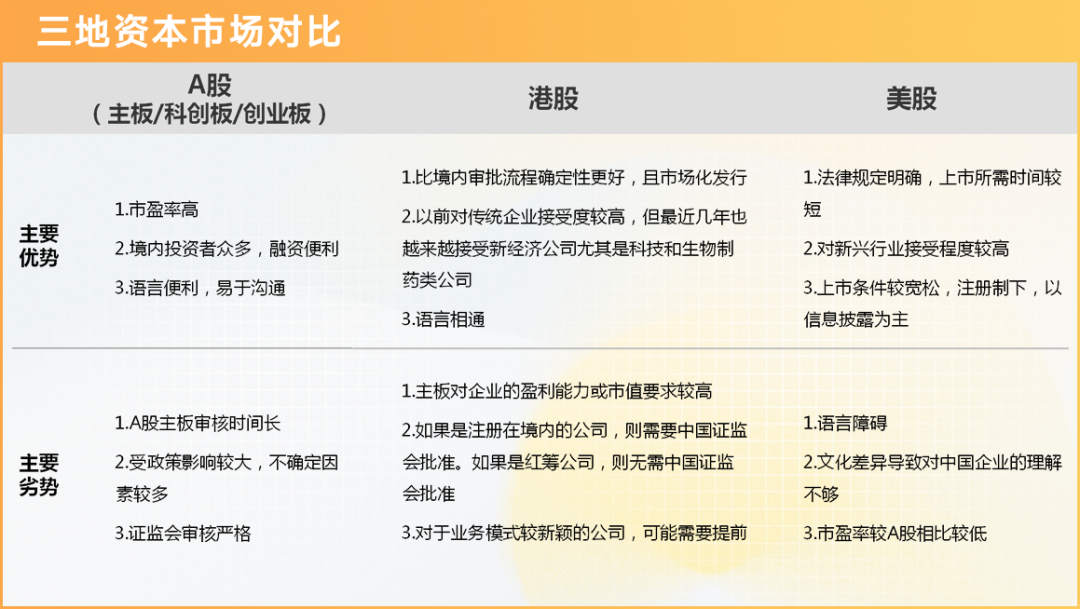

Drawing on Futu's experience, on the question of where to list, companies need to choose the most suitable listing venue based on current market conditions, the advantages of the three markets, and their own financing needs. Comparing the three markets: A-shares have higher P/E ratios but longer approval timelines; Hong Kong is the only market globally accessible to foreign, mainland, and Hong Kong capital, but its liquidity cannot compare to A-shares or US stocks, and trading volume is concentrated in top companies — the top 5% by market cap account for over 70% of total market volume; US markets have mature mechanisms and high acceptance of emerging industries, but the threshold for US listings has risen.

As for timing, there is actually no such thing as perfect timing. From initiating the listing to completion generally takes over 8 months, and future market conditions are highly uncertain. My view is: once listing conditions are met, move to list as quickly as possible; after listing, if difficulties arise, solve them — don't just wait. Moreover, secondary market valuation declines will to some extent transmit to primary markets.

Once listed, a new refinancing window opens. Take Futu itself: listed on Nasdaq in March 2019 with a relatively modest IPO raise; at its peak in 2021, market cap reached nearly $27 billion, and we conducted multiple follow-on offerings along the way. This laid a strong foundation for business development, sustainable operations, and weathering this round of market volatility. As they say, "with grain in hand, the heart is unperturbed."

III. Maintain Confidence — The Future Remains Promising

The March 16 State Council Financial Stability and Development Committee meeting, in my view, was highly visionary and may mark a good beginning for the next year or two or even longer.

On Chinese concept stocks — a major concern — the meeting stated that "Chinese and US regulators have maintained good communication, achieved positive progress, and are working to formulate specific cooperation plans." I judge the probability of resolution to be very high. The meeting also affirmed that "the Chinese government continues to support various enterprises in listing overseas."

On platform economy, it called for "prudently advancing and completing the rectification of large platform companies as soon as possible" — the "as soon as possible" is particularly important.

Furthermore, the meeting stated that "policies with major impact on capital markets should be coordinated with financial regulatory authorities in advance, maintaining policy expectation stability and consistency," and "accountability when necessary," as well as "welcoming long-term institutional investors to increase shareholdings."

This document deserves careful reading. And as various ministries and commissions roll out implementable policies following the Financial Committee meeting spirit, this will be enormously positive for both primary and secondary markets, generating sustained, sizable market momentum.

After the Financial Committee meeting, both Hong Kong stocks and US-listed Chinese concept stocks saw significant rallies — fundamentally, market forces seeing confidence. Including long-term funds with substantial influence on global financial markets, which are currently the dominant force in overseas markets — how to align them with China's economic development and entrepreneurship is very much worth our attention.