To B Ten Questions | Jianfeng Du, SAP Cloud Architecture VP: SAP's Cloud Transformation Journey and the Next Generation of SaaS Opportunities

Data, cloud-native, remote work, experience management, low-code/no-code, SaaS going global... What are the emerging opportunities in B2B worldwide?

SAP is the world's largest enterprise software company. Its three-letter name stands for Systems, Applications, and Products — reflecting its founding vision of aligning business processes through systems, empowering global enterprises through applications, and helping customers become "best-run businesses" that contribute to a better future for humanity.

At the 2021 Gaorong To B Growth Camp, Jianfeng Du, SAP's Vice President of Cloud Architecture, shared SAP's cloud transformation journey and emerging global opportunities in the To B space — spanning data, cloud-native infrastructure, remote work, experience management, low-code/no-code, and SaaS globalization — with 46 domestic To B entrepreneurs, offering practical growth advice drawn from real-world experience.

Jianfeng Du currently leads cloud architecture transformation for SAP SuccessFactors, driving improvements in availability, elasticity, performance, and cost to enhance customer experience. Previously, he served as CTO of SAP's Data Business Network, Vice President of Product Architecture, and led the technical integration of Qualtrics following SAP's acquisition of the experience management company.

Ten Questions on To B: Mapping the Next Generation of Innovation Opportunities. Below is Jianfeng Du's sharing.

In the 1970s and 1980s, SAP's five founders left IBM believing that software was the future, founding SAP to enter the ERP space and build business systems for enterprises — what was then foundational software architecture.

The 1990s marked SAP's high-growth period as it expanded internationally. The launch of the SAP R/3 system established SAP's leadership in business applications. By then, SAP's product lines had broadened considerably, covering finance, supply chain management, procurement, human resources, and other domains, forming a comprehensive Business Suite.

After 2000, with the rise of cloud computing — accelerating dramatically after 2010 — SAP established its "4+1" multi-cloud strategy. Internationally, it built deep partnerships with AWS, Azure, and Google Cloud Platform; domestically, it formed a strategic partnership with Alibaba Cloud. Combined with SAP's own cloud platform, this became the "4+1" multi-cloud architecture.

In 2010, as memory hardware costs declined and the speed advantages of memory over disk became clear, SAP developed its in-memory computing platform, SAP HANA.

Meanwhile, through innovation and acquisitions, SAP expanded and integrated across different business lines. In HR, it acquired SuccessFactors; in procurement, SAP Ariba; SAP Fieldglass for contingent workforce management; SAP Concur for expense management; CX for CRM and customer experience; and SAP Digital Supply Chain for managing digital supply chains in the Industry 4.0 space — a concept actually proposed by SAP CEO Henning Kagermann. Additionally, S/4HANA drove core financial innovation.

For these diverse business lines, SAP invested in infrastructure to enable better integration. At the data layer, SAP HANA unified databases; to facilitate collaboration across systems in multi-cloud environments and truly empower developers, SAP also launched Cloud Platform.

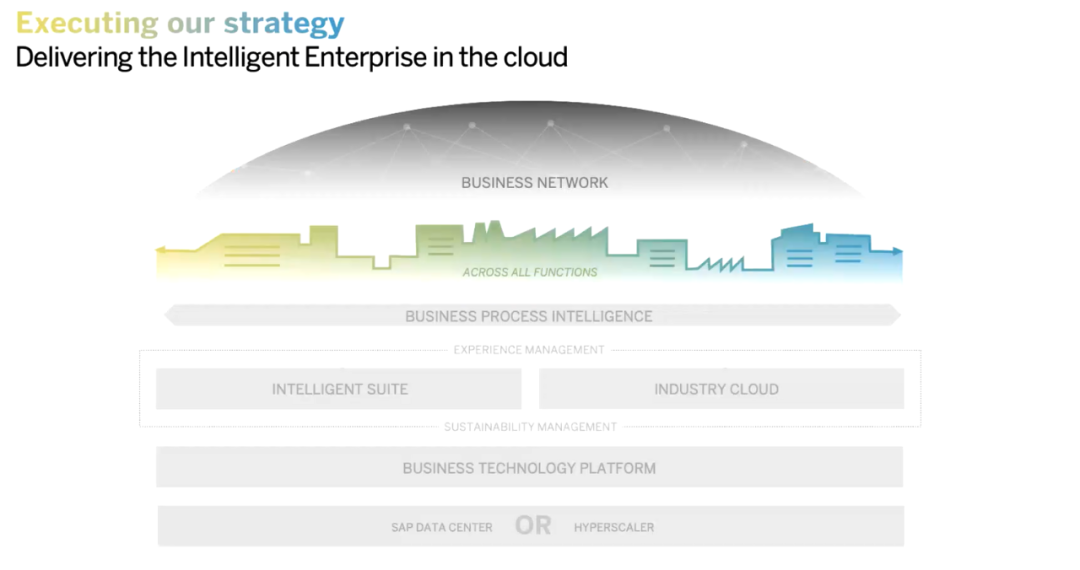

More recently, SAP has distilled a refreshed product and architecture strategy: Delivering the Intelligent Enterprise in the Cloud. According to this strategic map, the foundation is the SAP Data Center.

Above that sits the Business Technology Platform — the PaaS layer encompassing data management, analytics, application development, and intelligent technologies, addressing single sign-on, identity management, data model integration, API calls, business transaction processing, and integration. Of course, SAP's platform differs fundamentally from AWS, Azure, and others in its focus on business application scenarios — how to better empower developers in commercial applications, enable faster development of new functional extensions, and ensure those extensions integrate well with other products.

The application layer comprises two dimensions: the Intelligent Suite and Industry Cloud. The former encompasses the full suite of ERP, CX, HR, and other domains; the latter builds industry ecosystems based on SAP's experience. Here, the greatest opportunity lies in the ecosystem. We deeply recognize that while SAP can provide best practices at the industry level, we must empower the ecosystem and enable vertical innovators to participate in Industry Cloud opportunities.

Surrounding the application layer, SAP has focused increasingly on Experience Management and Sustainability Management. Over the next decade, the world's most valuable companies or best innovations may well emerge from the sustainability space.

Above that is Business Process Intelligence, leveraging AI to fully exploit data advantages.

At the top sits the Business Network, enabling collaboration across different commercial sub-networks to create network effects — a key priority for SAP's future.

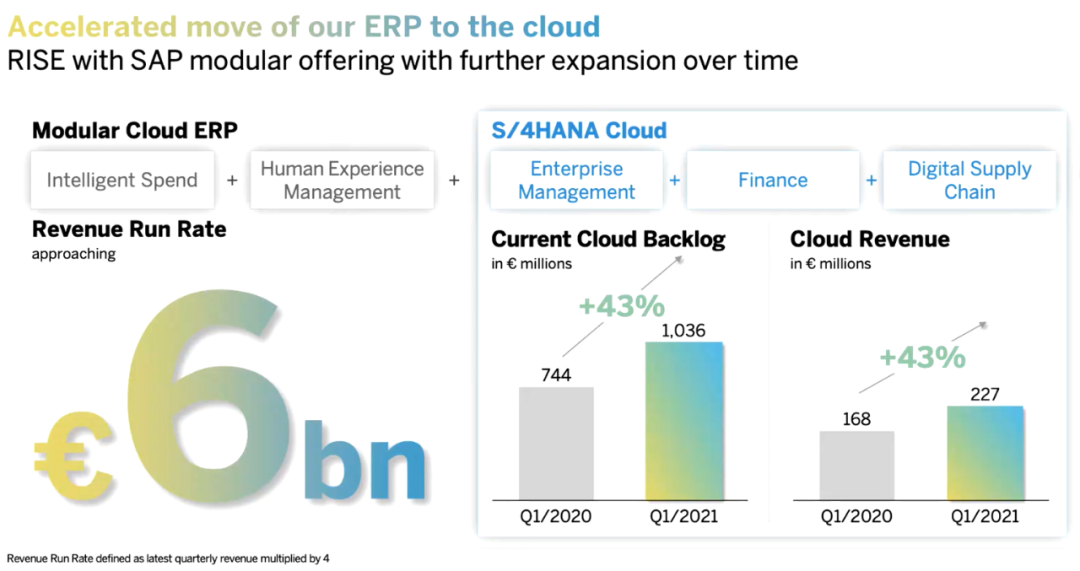

ERP remains perceived as a large-scale product, and indeed it was designed to be comprehensive from the start — the core system for enterprise-wide resource planning that requires some customization for industry-specific and customer-specific scenarios. Best practices cannot be rigidly applied across every industry. Our statistics show that many customers have undertaken extensive, expensive custom development, which has led to increasingly complex systems and uneven customization quality.

But today, under the wave of cloud-native and microservices architectures, modular innovation is becoming inevitable. We're seeing that individual business lines iterate faster than the enterprise as a whole. Traditionally, ERP sales targeted CIOs; going forward, they'll increasingly target business line leaders.

The core insight is that modularity isn't technology-driven — it's driven by business line evolution. Like the relationship between middle platforms and business lines, ERP functions as the commercial operating system at the enterprise level. As business lines accelerate and face intensifying competition, modularity becomes inevitable. SAP's HR, procurement, and core S/4HANA offerings, for instance, are all growing rapidly with fast cloud transformation progress.

China's To B market is enormous. In the US, To B and To C markets are roughly comparable in size; domestically, the gap between To B and To C market scale remains tens of multiples wide, representing massive latent opportunity.

Moreover, from the US To B entrepreneurship perspective, you don't necessarily need to solve comprehensive, large-scale problems like SAP or Salesforce. Sufficient penetration on a single-point problem, surpassing what large enterprises can achieve, creates substantial opportunity. The clearest example is Snowflake, which built a better data warehouse than AWS or Google, solving core pain points around data integration and lifecycle management post-integration, plus a multi-cloud strategy, driving exceptional growth.

Additionally, because of cloud普及, the overall architecture cost for To B entrepreneurship has dropped dramatically. A multi-cloud strategy also gives startups competitive differentiation against tech giants — no need to fear monopolistic dominance.

Of course, cultivating customer habits takes time: willingness to pay, expectations around customization, and so on. Currently, domestic customers are quite unaccustomed to purchasing software from different providers and doing their own integration — though this is already commonplace in Europe and the US. With collective industry effort, I believe this process will accelerate.

Specific emerging opportunities I'm focused on include the following.

First, there remain significant opportunities in data. With the modularization trend, breaking down data silos and achieving data integration is a major pain point. Data compliance is also receiving increasing attention, with Europe, California, India, and China all enacting data-related legislation. From a technical perspective, how to advance data integration while maintaining compliance presents a challenge. Once data is available, better analytics and applications built on that data offer further opportunities.

Second, cloud-native represents a moment that brings To B entrepreneurs onto the same playing field — a complete reshuffling opportunity. Like how China's internet leapfrogged from Web to Mobile and then rose, cloud-native has inherent architectural advantages that, once unleashed, can deliver era-spanning opportunities. Cloud-native remains very early-stage; Kubernetes has only solved resource orchestration. Next come two phases: first, Service Mesh — how microservices better collaborate; second, Federated Service Meshes — solving collaboration between different meshes. As cloud-native evolves toward Serverless — where microservices coordinate regardless of server location — this will bring transformative change.

Third, Customer Success remains a very early concept both domestically and internationally, currently focused mainly among technology companies providing end-to-end full-process coverage. As technology companies proliferate, customer success will become increasingly important, with substantial opportunity embedded.

Additionally, one opportunity connected to the pandemic is Agreement Management. DocuSign, for example, evolved from electronic signatures to a broader agreement cloud strategy encompassing contract management. This domain deals more with relationships between people and between enterprises — an interesting space.

I'll share two examples drawing on products I use and stories from friends who've started companies.

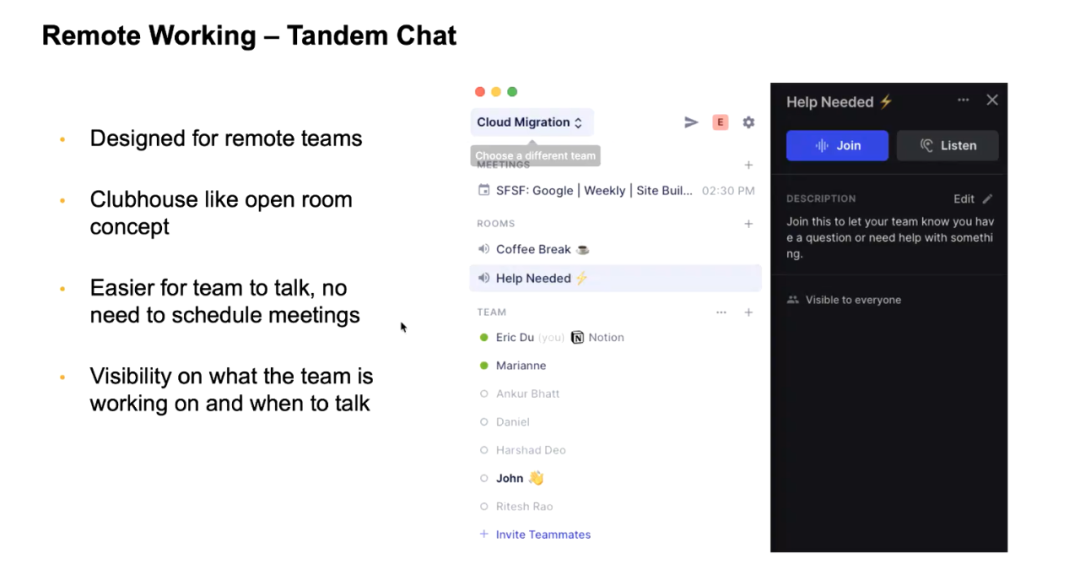

The first product is Tandem Chat. It's somewhat like a voice-based Slack, or an enterprise version of Clubhouse. There's a meeting room; no need to schedule in advance — if someone's in the room, you can jump in and speak anytime. Team members can understand each other's work status and know when a casual conversation is possible. It simulates the open-floor-plan office environment quite well, making it especially suitable for small teams seeking an immersive office-like experience, and works well for brainstorming.

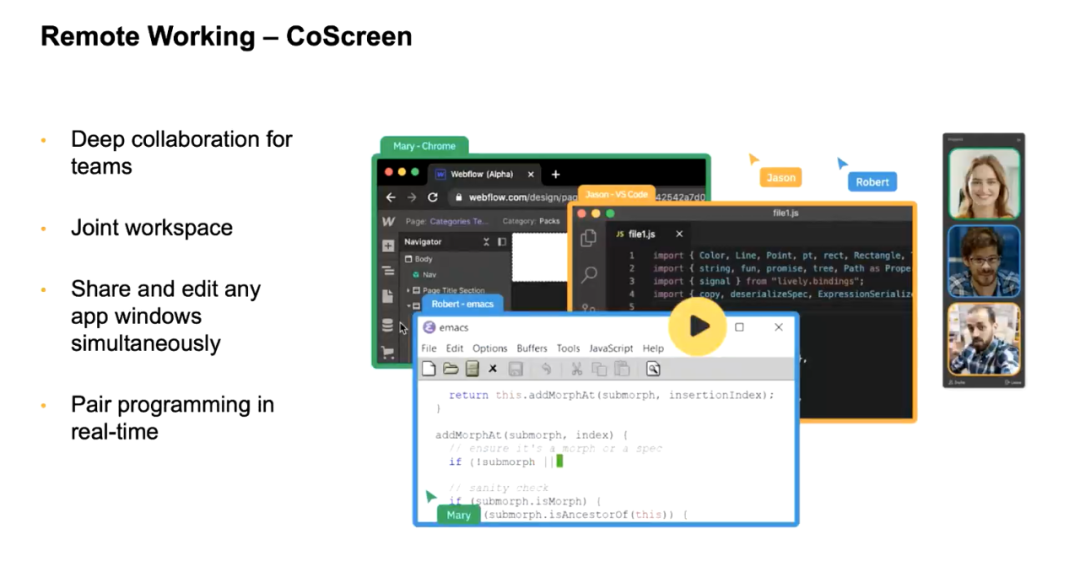

Another product is CoScreen, providing deep collaboration for teams, primarily targeting developers. Users can join shared workspaces, share and edit any application window, and support collaborative programming — improving remote development team efficiency.

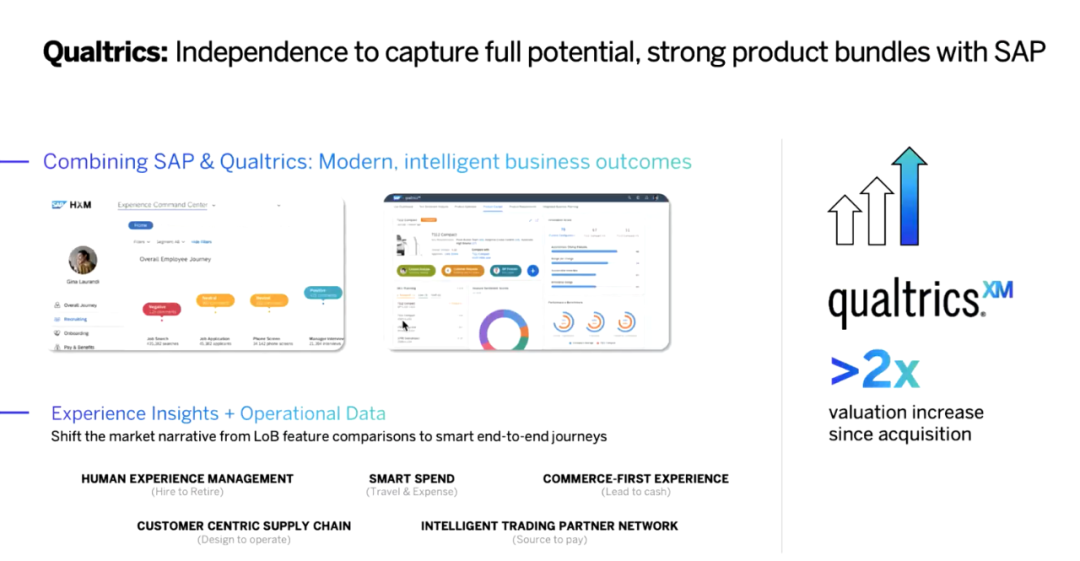

The logic behind Experience Management is the massive Experience Gap between enterprises and their customers. Research shows that 80% of To B CEOs believe they deliver excellent service, yet only 8% of customers agree — a huge chasm.

In 2018, SAP acquired Qualtrics. Originally founded on user research, it expanded platform capabilities to develop a comprehensive experience management suite covering employee experience in HR, customer experience, product experience, and brand experience. Take employee experience: traditionally, enterprises had only historical data — from recruitment through onboarding to promotion — but lacked human, "warm" data: experience data. Why do employees leave? By combining historical data with collected employee experience data (mostly unstructured), analyzing and structuring it, conclusions can help enterprises act, correct, predict, and improve — comprehensively enhancing employee experience. This year, Qualtrics successfully IPO'd with a market cap exceeding $17 billion. Post-acquisition, Qualtrics integrated with SAP in several ways. Qualtrics' experience data (X-Data) is combined with SAP's operational data (O-Data) to provide multi-dimensional insights. This integration is embedded within SAP's HR, expense management, supply chain management, and customer experience modules.

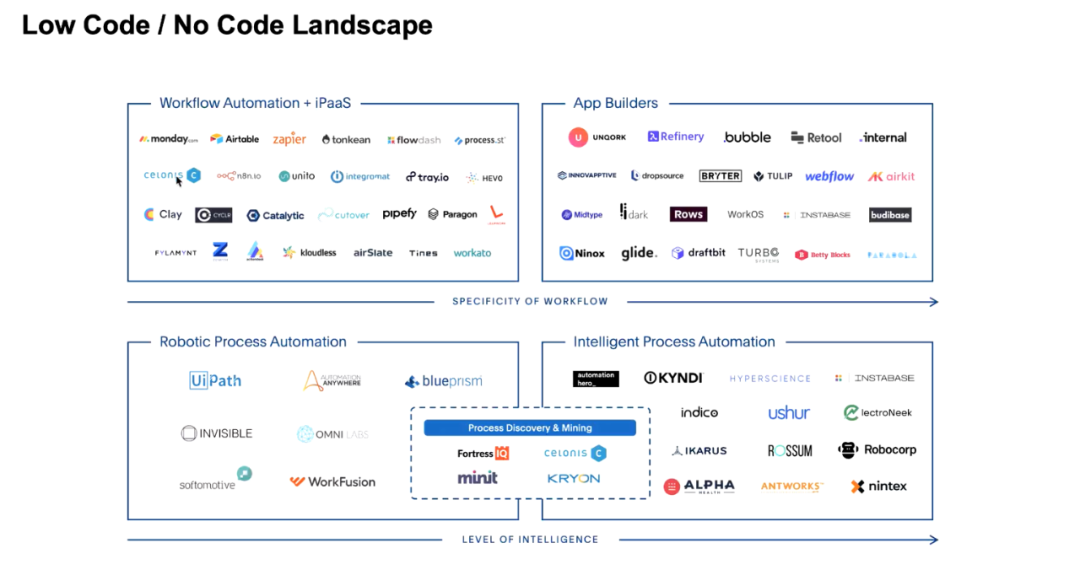

Low-code/no-code has been around for years; the pandemic somewhat gave it new life. Currently, startups in this space fall into four categories.

First is Workflow Automation and iPaaS, including Monday.com, Zapier, and Celonis. Second is App Builders — helping create better, faster, more consistent applications. This category has a long history, including Salesforce and to some extent SAP. A notable representative is Retool, specifically targeting internal application development efficiency. For large enterprises, over 35% of development resources actually go to internal systems — massive scale — yet internal application quality is often uneven, which Retool aims to address. Third is Robotic Process Automation (RPA), represented by UiPath. For repeatable tasks, it applies a robot-like approach to classify and repetitively execute business processes. Interestingly, UiPath has an app store concept: beyond solving customer problems, it enables knowledge workers to convert expertise into reusable functions distributed and promoted through the platform. The final category is Intelligent Process Automation, still quite early-stage — helping automate business processes with more timely, accurate insights at critical junctures. Some may ask: won't low-code/no-code eliminate internal developers? If it replaces me, why would I use it? In reality, this is a process of mindset evolution and an inevitable trend. Internal developers themselves are continuously improving in effectiveness and efficiency, and may more actively embrace such tools. There's also opportunity for business personnel to participate in tool development, further empowering more people and bridging the gap between business and technology.

From a CVC perspective, financial metrics are certainly considered in acquisitions — subscription volume, renewal rates, revenue, and so on. For example, when we acquired Qualtrics, the company was already profitable, quite rare among fast-growing SaaS companies. But our primary M&A goal is always to open new business lines and create new categories, with synergy to existing operations. In trendy terms, rather than "involution," our starting point is how to "evolve outward." Previous acquisitions of SuccessFactors and Concur followed this pattern — anticipating the inevitability of modularization in the cloud transformation journey and positioning ahead of it. The Qualtrics acquisition reflected our belief that the future is the experience economy, with complementary data capabilities. For any mature enterprise seeking long-term success, the essential consideration is how to open and create new domains. Apple, for instance, continuously expanded from MP3 to iPhone to iPad to cloud services. We also examine acquired companies' customer distribution from a sales synergy perspective — whether there's potential for mutual customer penetration.

For SMB customers, Qualtrics, Concur, and others have well-developed digital growth channels. Concur has been particularly successful, with numerous small customers paying a few hundred dollars annually, many distributed through travel subscription service partnerships. Of course, SAP's greatest strength remains enterprise sales, with some summarized learnings. First, thought leaders play a crucial role in To B. Endorsements from Gartner and Forrester matter enormously — they have an influencer effect. Behind thought leaders sit CIO communities, the real decision-makers. They communicate within their circles about which companies' products and services they've purchased. Don't underestimate word-of-mouth; much social network promotion represents weak ties, while thought leader relationships are strong ties. For To B, strong ties likely matter far more than weak ties. Additionally, to win large enterprise customers in the future, you must go deep into industries with solutions. Every industry faces unique problems and has its own organizational forms. How to empower industries creates point-to-surface opportunities. Successfully solving one company's problem within an industry can open the entire sector. My recommendation: To B companies should focus on a few industries where they have greater capability and understanding.

In cloud marketplace development, SAP continues investing and has elevated "Business Technology Platform" to company-level strategy. We deeply understand that we cannot solve all customer problems alone — we must better empower the ecosystem. Beyond helping solve specific extension needs, we need the ecosystem to enhance platform stickiness. Because customers don't just use your technology product — they use your business processes. Every ecosystem partner brings the ability to solve problems within business processes, and these problems are sustainable, ever-present, thus helping the platform increase customer retention. For empowerment, we've provided extension APIs, developer tools, and launched the SAP App Center, currently invitation-only to maintain quality rather than fully open. For App Center developers, we also provide customer referral, promotion mechanisms, and other empowerment approaches.

For today's new generation of entrepreneurs, whether through improved cloud infrastructure or the post-pandemic default of remote work as standard collaboration mode, Chinese SaaS companies have greater opportunities to go global. There's also a major dividend: unlike previous SaaS entrepreneurs, China's new generation possesses global vision — including international backgrounds and ambitions for international expansion. Combined with Chinese engineers' advantages in AI and other emerging fields, this can support such ambitions. Of course, the greatest barrier lies in product and market definition — how to better understand market and customer needs, how to enhance product capabilities and build market-fit products. This is the hardest part. My best wishes to entrepreneurs: after establishing yourselves domestically, may you successfully sail abroad.

Innovusion, Global Leader in Image-Grade LiDAR, Completes $64 Million Series B Round