A Visual Breakdown of Gaorong Ventures' Retail Investment Model: Why It Keeps Doubling Down on the Fresh Grocery Sector

What kind of business model can better carry consumers' channel trust? And push closer to the endgame of retail?

In April this year, Gaorong Ventures shared its retail investment model with the industry (see Advanced Retail Formats Need to Intercept Consumers Across Time and Space). Over the past several months, this model has helped Gaorong identify some exciting companies — and the equally exciting founders behind them. These include community group-buying startup Linlinyi, which completed its Series A round during the New Year holiday, and Dingdong Maicai. These entrepreneurs are the real driving force pushing the industry forward.

In a recent in-depth conversation between Rui Han, Managing Director at Gaorong Ventures, and Zhihin Xu, founder of Jianshi Technology, Han elaborated on this retail investment model. Gaorong hopes to work with more industry innovators to stay the course and move together toward the endgame.

Rui Han, Managing Director at Gaorong Ventures

Before discussing the Linlinyi investment, I need to explain our market judgment and framework.

What do we want?

We've been thinking about one thing repeatedly: what kind of business format can better carry consumers' channel trust?

We believe that in China, fresh produce will be the best entry point for this trusted channel. Beyond the commonly cited attributes of high frequency and necessity, fresh produce has several other characteristics: it's non-standardized, product brands have weak stickiness, and there are many pitfalls. The channel must essentially serve as the consumer's buyer, passively taking on their trust.

Based on this, we're very bullish on using fresh produce as an entry point to evolve into a high-frequency, high-trust channel that penetrates the household decision-maker's wallet. This channel will capture the household decision-maker and gradually bring in consumption from the entire kitchen and even living room scenarios — this is what we value most.

So the overarching theme is: enter through fresh produce, build channel trust, and continuously capture greater share of the household decision-maker's wallet. Another important point: from first-tier to fifth-tier cities, different formats will emerge to carry this trust because mainstream consumers prioritize different decision factors.

We see that consumers display different behaviors not just spatially (the commonly cited tier 1-5 city framework) but also temporally. Perhaps we shouldn't use the individual person as the smallest unit of analysis for understanding fresh produce purchasing behavior.

Simply put, when a person is with their whole family on weekends versus living alone on weekdays, the ranking of their decision factors changes. On weekends, the kids are back and the family eats better; Monday through Thursday, they make do with more convenient and quick options. So today we believe we should break things down at the level of scenario-based orders to better understand what constitutes mainstream versus long-tail demand. Our understanding of purchase granularity needs to go down to each individual order.

Only by thinking from the perspective of scenario-based orders can we make global generalizations and thus more confident deductions.

What do we believe?

This dimension of scenario-based orders makes us very confident in several judgments:

First, because consumer decisions are so diverse, no single retail format can achieve monopoly. Even in Shanghai, where convenience stores are highly developed, many mom-and-pop shops persist. Even in South China, where fruit chains are highly developed, independent fruit stores still exist in Guangzhou and Shenzhen. Of course, there are tactical factors like regulatory compliance and owners not counting their own labor costs, but fundamentally, giants cannot satisfy all scenario-based orders.

Second, we believe that so-called advanced formats may not only fail to earn excess profits initially — they may even have to bear excess education costs and self-built infrastructure costs. Whoever advances pays the industry's tuition. That's why we see some new retail formats subsidizing — they need to change users' entrenched habits.

Finally, we ask: what is the endgame of retail? Can anyone reach it? If not, how do we infinitely approach it?

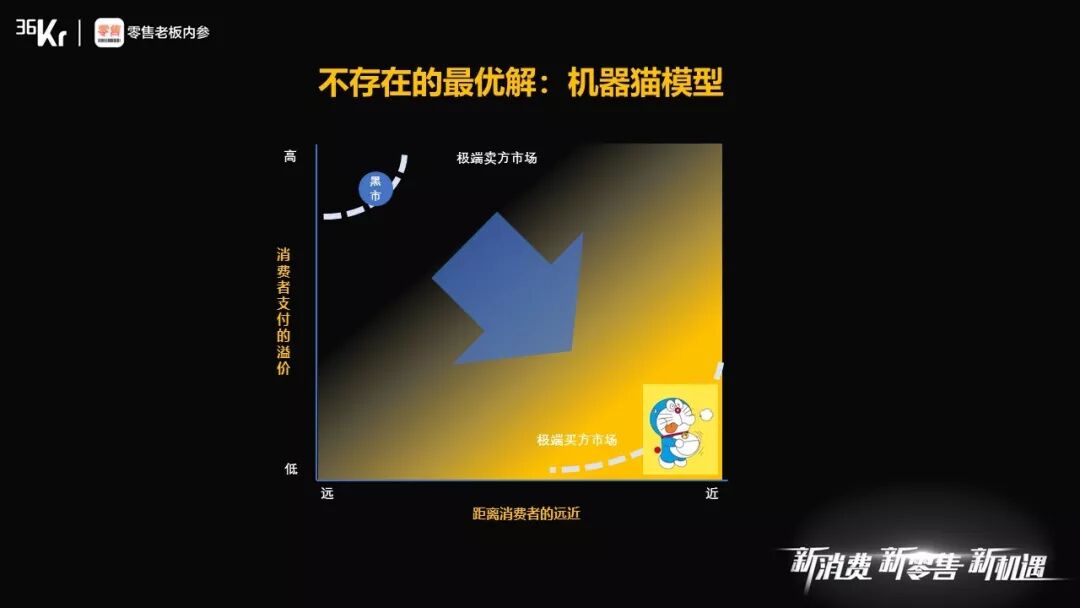

The term we use internally for the endgame is "Doraemon." Imagine it: everyone holding a Doraemon, getting whatever they want, instantly available, infinite shelf space, no fulfillment costs — this is the ultimate ideal. But we know this doesn't exist in any foreseeable future.

Materials from Rui Han's keynote at the 36Kr Retail Summit

Based on these assumptions, we try to put both induction and deduction into one model. Before starting, we break down the retail elements one by one.

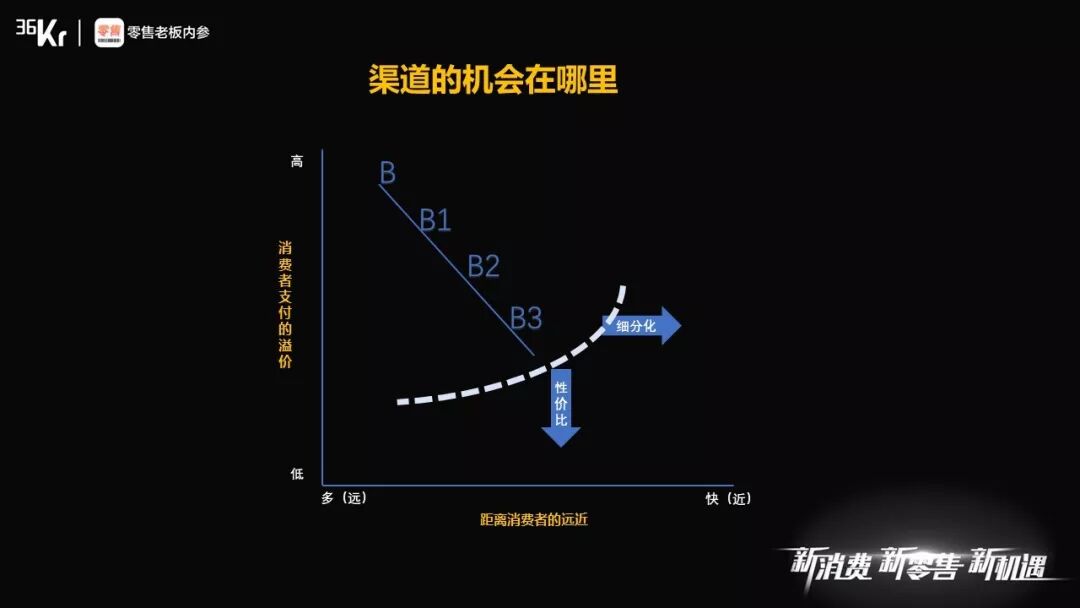

Let's start with four familiar keywords: "more, fast, good, cheap." The great thing is that these four words are pairwise contradictory (which actually well explains why as long as consumer demand isn't unified, monopoly doesn't exist). No one can optimize across all four dimensions simultaneously.

First, "fast" and "more" are contradictory. Fast means close — the closer to the consumer, the smaller the shelf needs to be, otherwise inventory turnover becomes unbearable. More means big shelves, which means building big warehouses — impossible to build right next to consumers' homes. We can use another set of metrics to replace "more" and "fast": "far" and "near."

Meanwhile, "good" and "cheap" are also contradictory in the long term. We offer another set of metrics called the consumer premium payment coordinate.

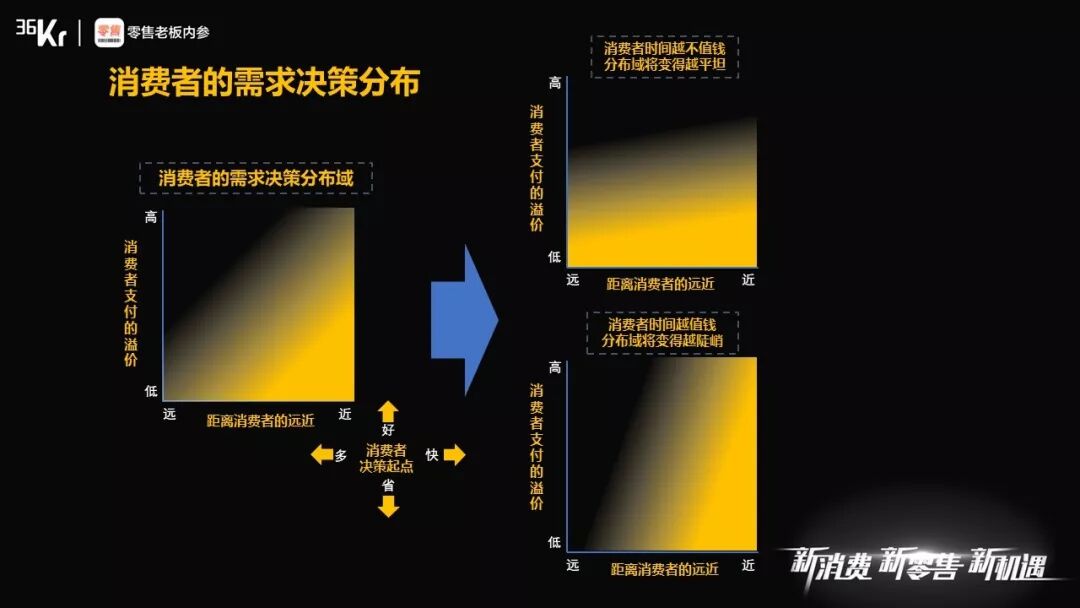

After drawing this coordinate, we imagine the most comfortable state for a consumer: definitely staying in the bottom right corner, with everything delivered to hand, paying minimal or even no time cost or premium. We call this the consumer starting point.

But when a consumer needs to complete a transaction, they must move away from the consumer starting point — which direction? This actually depends on the "time-money exchange rate" for that consumer in that particular order. For example, white-collar workers in first-tier cities typically have fragmented disposable time and some disposable income; they might be willing to pay 3-5 RMB for errand services, paying money to save time. In this coordinate, that's moving upward. Or take our parents' generation — they have relatively abundant time, and derive more happiness from cost-effective products; they're willing to spend half an hour going back and forth seeking better value. Paying time to save money. In this coordinate, that's moving leftward.

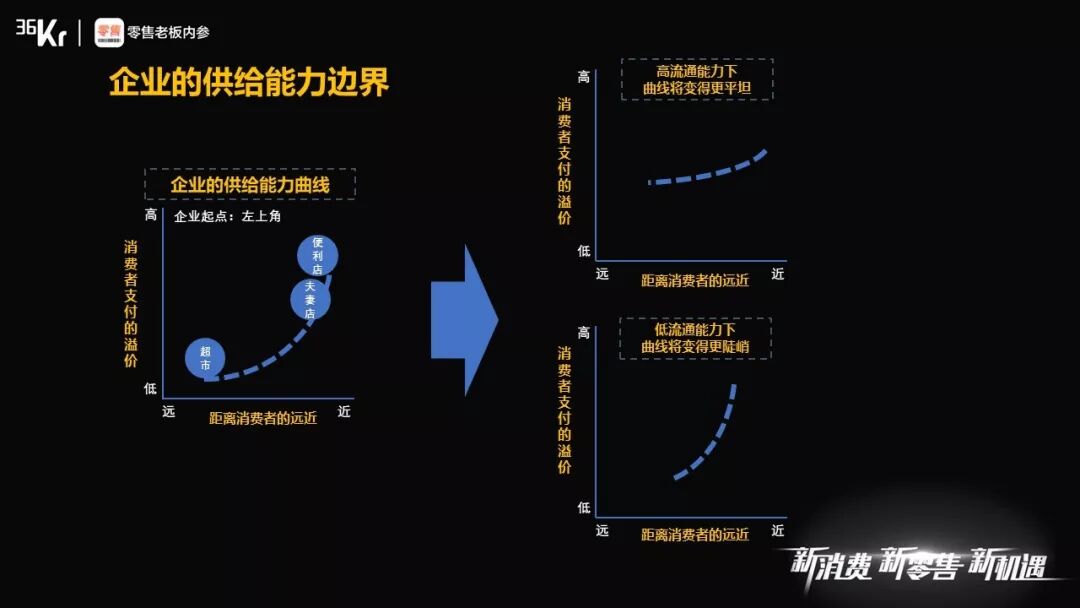

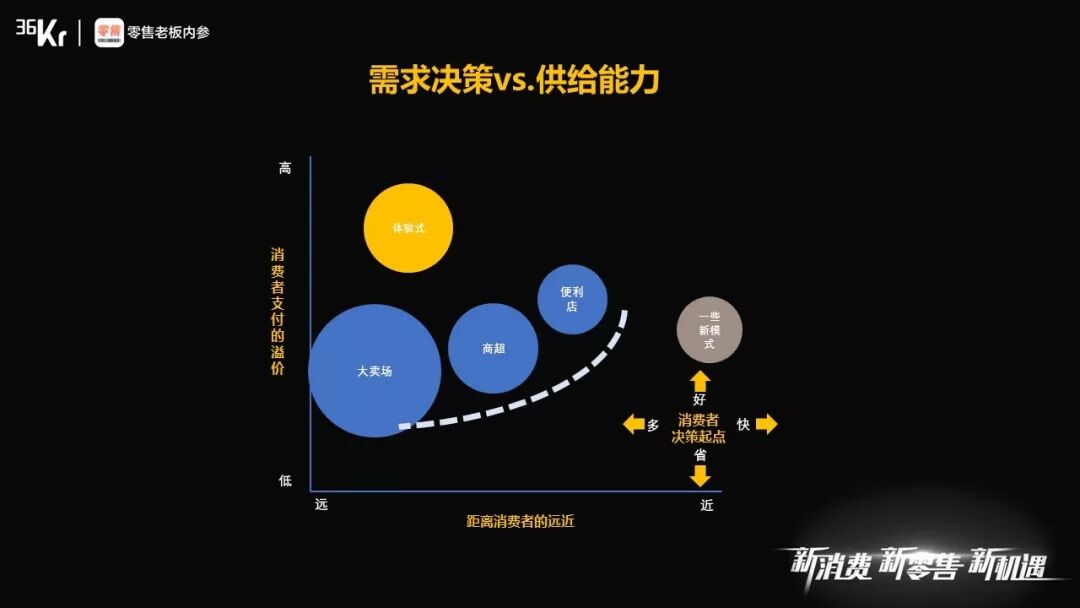

Correspondingly, on the supply side, Metro and outlets sit at "cheap" and "far" — lots of stuff, very economical, but consumers pay time costs. Convenience stores sit at "good" and "near," but users pay a premium for this convenience.

Now let's imagine: what's the most comfortable state for the B-side (sellers)?

In a limited supply situation, i.e., a seller's market, the most comfortable state for a business would definitely be the top left corner of the coordinate: products come off the production line and consumers come pick them up themselves, fruits are picked by themselves, consumers pay time costs and premiums to complete the transaction, while the merchant neither fulfills nor needs to negotiate prices. Past bazaars were essentially this state — once a week, requiring a special trip to the county, and things weren't cheap either. Consumers want the other party to appear before them, convenient and cheap, fast and economical, no need to bargain. But these two are contradictory — no transaction can happen. We call this the business starting point.

Extending this logic: as supply gradually opens up, as seller's markets gradually shift to buyer's markets, as soon as any business moves slightly away from the so-called business starting point toward the bottom right (selling a bit cheaper, getting a bit closer to consumers), consumers will be intercepted. Let's label this "B1." So for the B-side, they'll continuously move forward, creating B2, B3, and so on.

However, the "B" side can only go so far. Beyond a certain point, even when efficiency is maximized, the costs of providing better experience become unbearable. This creates a boundary line. At any given point in time, all B-sides cannot exceed this line — crossing it means losses. This line represents, under given historical conditions, the capability boundary of enterprises.

Enterprises that best balance experience, cost, and efficiency all press against this capability boundary. Some service-oriented and experience-oriented formats can bypass other retail formats' interception to pull consumers out. Meanwhile, many formats that overemphasize "consumer experience," like past O2O models and unmanned shelves, actually ended up outside the enterprise supply capability boundary.

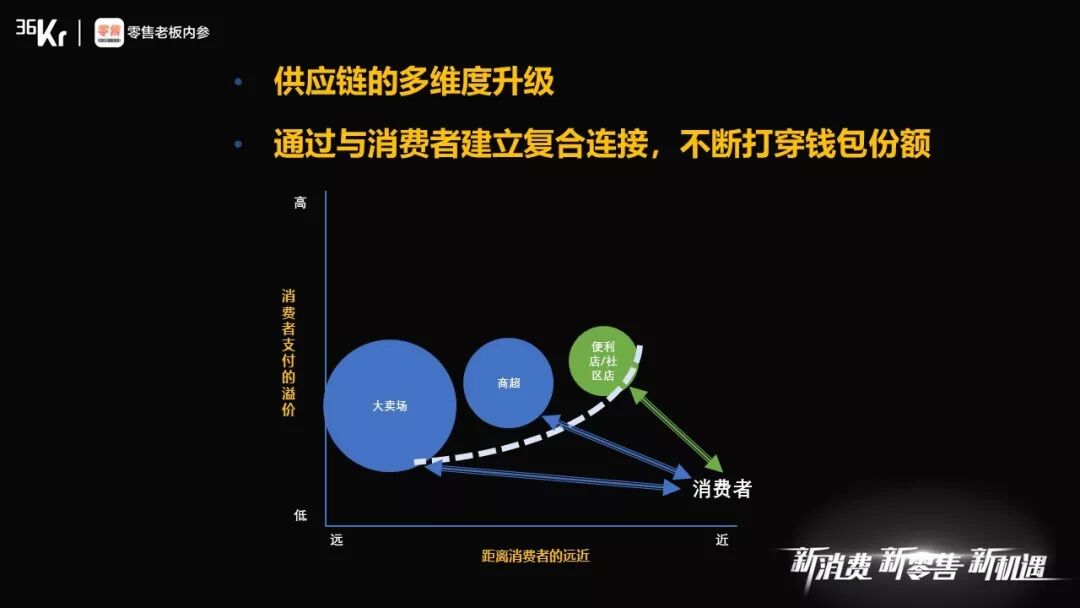

We believe that in the long term, the movement of the enterprise capability boundary toward the bottom right is more a result of progress in society's underlying capabilities, mainly including fulfillment and distribution capabilities, management capabilities, technological capabilities, etc. — not the result of one or two enterprises' efforts in the short term. For enterprises already standing on the boundary, to continue moving toward the consumer starting point, they must build certain core capabilities themselves to break free from the limitations of society's underlying capabilities.

This will give them a supply capability boundary different from their peers — this is the extra cost that advanced formats need to pay, as mentioned earlier. JD.com building its own logistics is a good example. Otherwise, if every link uses socialized resources and third parties, efficiency gains will hit ceilings faster.

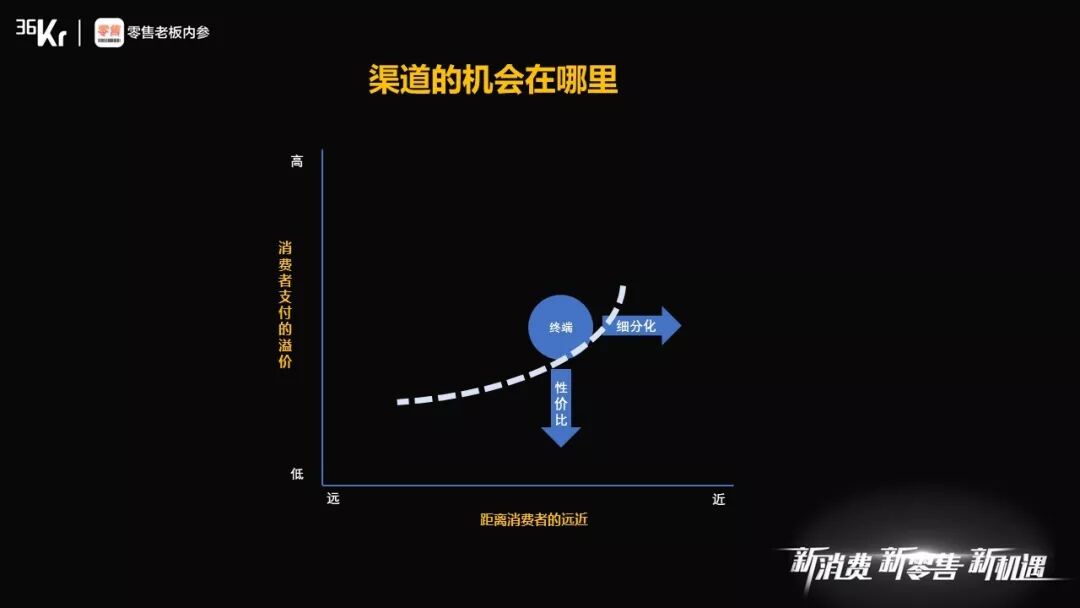

But what excites us tremendously today is that after mobile internet and last-mile infrastructure matured, enterprises originally pressing against the boundary now have the opportunity to directly connect to the consumer starting point. We used to call it "intercepting on the street"; now it has become "intercepting at the bedside." Consumers can place orders lying in bed, and the commercial flow ends right there. From originally single-dimensional spatial interception, it has become temporal interception.

After drawing this diagram ourselves, the deduction becomes clearer. As VCs investing in advanced retail models, we believe we must resolutely penetrate one point among "more, fast, good, cheap," and ideally achieve some structural change in cost.

For example, our investment in Dingdong Maicai resolutely takes the path of trading money for time — extreme convenience, extreme speed. Satisfying instant scenario-based orders in first-tier cities. We firmly believe that in this market, given equivalent product quality, speed will become an increasingly important and mainstream factor. Meanwhile, we also believe that in third-tier cities and below, where life rhythms are relatively slower, users are willing to wait a bit longer, but merchants must provide the best value — even supplying things not locally available. This is the community group-buying we're discussing today.

After figuring this out, we look for entrepreneurial projects in these several areas to execute this vision. Through fresh produce, capture the household decision-maker's wallet — and throughout this process, never lose channel trust. So several metrics are particularly critical.

First is fresh produce share. Too high a fresh produce share means users haven't transferred their trust to other products; wallet penetration hasn't begun. One hundred percent fresh produce means users treat you as a wet market — no one buys stockings at a wet market.

Linlinyi's fresh produce share is 60%, which already proves Linlinyi has established strong trust with users, yet Linlinyi isn't a fresh produce store. It's more like a small membership store at users' doorsteps, satisfying diverse household consumption needs.

Second is frequency. We were very pleasantly surprised to find that both models achieve 6-8 or more purchases per existing customer per month, sometimes even higher.

What does 6-8 times mean? The typical frequency for purchasing at neighborhood convenience stores is 5-6 times per month — this is even higher than visiting physical stores.

Rui Han, Managing Director at Gaorong Ventures

Jianshi: When did this model emerge?

Han: March 2018. We had this model first, then went to deploy these investments.

Jianshi: So you used this model to find investment projects?

Han: This diagram gave us a broad directional guide — looking at the market five, ten years out. We believe new solutions will emerge in lower-tier cities and first-tier cities alike, and these players will be more disruptive than traditional supermarkets because they intercept orders inside the home.

Jianshi: Food delivery is also local service, but in the end, everyone found that national Matthew effects still swept away all geography-related services, becoming different segments under one big Meituan. But you don't think community group-buying will produce national oligopolies?

Han: Let me start with facts. First, in large enough countries worldwide — Europe, America, Japan, Korea — no player has achieved monopoly in the fresh produce dimension. That's the first fact. Second, it depends on whether a business is selling services, virtual goods, or goods that form inventory. Doing fresh produce well is a locally supply-chain-heavy job.

Jianshi: In the community group-buying segment, Jianshi has done deep conversations with most players by now, and it feels like the current focus is on goods-side management systems, community leader operation systems, etc. What stage do you see industry competition at now?

Han: This is what we've thought about longest in our investment. It's true that barriers to entry are low — anyone can do it. Changsha alone has two or three hundred group-buying operations. But I think we need to discuss how we define "pitfalls" versus "moats."

A "pitfall" is when no one else attacks you, but you fall into a hole yourself and can't climb out — you kill yourself. A "moat" is when others attack you but can't break through your defenses. This industry clearly has low moats — no one says this is too hard to do. But there are too many pitfalls. Most players, frankly, just need to do their own thing right, persist in doing the right things, and competitors will gradually disappear.

Where are the pitfalls? I think the biggest pitfall is product capability.

In this model, whether it's convenience store owners, stay-at-home moms, or agents — they're selling on your behalf using their face, their personal connections. The last thing they want is for you to put them in hot water. Put another way: between the enterprise and friends, what exists? Human connections. WeChat commerce trades human connections for transaction volume — add your WeChat, sell to you twice, human connections are depleted, done after one or two sales. Sell bad goods once or twice, and that human connection is severed — irreversibly severed. So human connection depletion is a critical point; entrepreneurs must not let agents' and users' human connections be depleted.

How to prevent human connection depletion? The key is still product. So today we see many groups kill themselves — one bad batch, two bad batches, and the group dies. Linlinyi puts product first — this is what we value greatly.

We believe product is the biggest pitfall among them. Do product poorly and you die for certain; but doing product well isn't enough either — it's an absolute necessary condition. But behind product lies your supply chain capability, IT capability, etc., ultimately manifesting in whether consumers can buy cost-effective products through you and gradually trust you. Otherwise I'll go elsewhere.

Thinking about it now, community group-buying also achieves something past mega-trends didn't: "sharing" — sharing moms' time, moms' homes, moms' garages; sharing convenience store space. Community group-buying doesn't bear startup costs. Today's community group-buying adds things onto given commercial entities or physical nodes — no need to bear zero-to-one costs, but rather sharing partners' time and space.

Jianshi: It seems "sharing" is rarely discussed.

Han: Past discussions often confused means and ends. Treating means as ends, ends as means. Sharing is a means, not an end. It's a means to achieve cost reduction and efficiency improvement. Not sharing for sharing's sake.

Jianshi: Community group-buying also involves LBS and O2O.

Han: All means. Can't treat means as investment themes. Investing is like mountain climbing — you still need to reach the summit. The key is finding the right mountain, not finding the right way to climb.

Jianshi: Very interesting. Looking back to previous conversations with Jianshi and Gao Xiang, you said you studied new US e-commerce models, then found there were still new opportunities in e-commerce, and went to look for them domestically.

Han: I think we need a foundation for deduction, and the prerequisite must be deep analysis and understanding of the matter. Without an investment framework produced through research, it's pure gambling. Anyone can make mistakes, but you must understand where you went wrong — there must be a review mechanism, making progress from both successes and failures.

This is essential work. Today it's not about whatever exists in the US we should invest in here. We need to understand why the US has certain products and businesses — these are all surface phenomena. What are the underlying demand and supply structures? What kind of supply would emerge from such demand in China today, especially combined with China's unique background and infrastructure? Investing is more a process of deduction, but the foundation of this deduction is induction. If in this diagram we know where Walmart is, where Costco is, where 7-Eleven is — if we think through all of these, then look at what money they make, what they spend, how their gross margin structures change — this can better help with deduction.

This contains many open questions, like the one just mentioned: is social e-commerce's social aspect a means or an end? Is it a tool for a lifelong e-commerce to grow faster, or in the end is it just people selling to people — a formalized version of WeChat commerce?

Jianshi: You mentioned this model is organized from the retail side, while Pinduoduo belongs to the traffic side. Is there a possibility that looking from the traffic side at your model, it might completely not hold up?

Han: Everything can be explained from multiple angles; the value lies in helping us grasp the big picture and let go of the small stuff.

If everything from ancient bazaars to everything that's happened on Earth can fit inside, and we can confidently see trends as time progresses, plus the endgame of "Doraemon," then perhaps it can help us blind men touching the elephant see slightly more clearly. I hope this model can help us think more clearly about the mountain at certain stages — it's just about the path choices in between.

Jianshi: Back to the Linlinyi investment. Was this deal fast?

Han: Their fundraising timeline was very compressed. Our previous round investment closed in October or November, and just one or two months later they completed this latest round. However, valuation and fundraising speed don't matter — what matters is still endgame value.

Jianshi: Now it's the so-called capital winter — did valuation have any impact?

Han: We didn't negotiate on price. Because in growth-stage projects, static valuation is a dangerous thing. Valuing based on current revenue — this is what some secondary market investors do. What's more important is still the endgame value I just mentioned. If it can only grow to 200 million, then even 100 million is expensive. If it can grow to 10 billion, then 100 million is absolutely cheap. Though cash flow issues in between are considered, the most critical thing is still the endgame — how big this thing can grow is what matters most.

Jianshi: Is community group-buying explicitly being called a star track or trend now?

Han: This terminology is rarely used internally at Gaorong now. We don't care whether it's a trend. When investing in many projects, what matters most is the mega-trend and judgment of the endgame.

Jianshi: So you feel relatively settled in your minds?

Han: Yes.

Jianshi: What's Linlinyi's ARPU?

Han: Per user per month we've seen 260-300 RMB. Monthly standing above 200, over 2,000 RMB per year. This is actually quite good. And it's continuously rising.

Jianshi: Roughly how much room is there to rise?

Han: This has a lot to do with assortment strategy. For example, if they start selling iPhones someday, that month's number will definitely jump. The key is that whether looking at trends or frequency, both are rising. ARPU growth may be more like stairs than a slope. It depends on whether new category supply chains can run smoothly, and whether channel-acquired consumer trust can be leveraged.

What might eventually happen? If you tell consumers: come buy tissues on the 1st of every month, this day's group-buy is the cheapest, stock up welcome. Then for the following month, very few people in the neighborhood will buy tissues at offline retail stores. The demand rhythm is captured by community group-buying. If fewer and fewer people buy tissues nearby, surrounding shops will start reducing tissue inventory and shelf display, further pushing consumers out to the community group-buying channel. It can control the purchase rhythm of planned consumables — this is what we hope to see.

Jianshi: Will it go in the direction of something like Yanxuan's low-price, high-quality custom production?

Han: After entering through fresh produce and establishing trust with the household decision-maker, the channel itself becomes the brand. Finally, gradually customizing more cost-effective products based on consumer demand — this next step is something everyone will likely do.

Jianshi: So community group-buying will unhesitatingly go down this path?

Han: I think it definitely will. If you completely trust Linlinyi, Linlinyi is the best brand.

END

Recommended Reading

Gaorong Ventures 2018: New Consumption and New Technology for Long-Term Value

Advanced Retail Formats Need to Intercept Consumers Across Time and Space | By Gaorong

- Gaorong Ventures manages US dollar and RMB funds totaling approximately 15 billion RMB, focusing on early-stage and growth-stage investments in the TMT sector.

- Limited partners include top global institutional investors as well as corporate giants in China's finance, retail, advertising, and other industries.

- Meanwhile, dozens of successful entrepreneurs — including founders of Tencent, Baidu, Taobao, Xiaomi, Meituan, Dianping, 360, Focus Media, Weibo, Sohu, JD.com, Vipshop, Tudou, Autohome, Ganji.com, and other companies — are also limited partners of Gaorong Ventures.

- Founding partners have led investments in multiple outstanding companies, including Xiaomi, Razer, Baofeng Technology, G-bits, Tudou, Wondershare, Archermind, 91 Assistant, 3G.cn, Mogujie, DOTA Legend, Yuanfudao, and others.

- Since its founding, multiple companies Gaorong has invested in or taken stakes in have grown into national or global leaders in their respective industries, including: Pinduoduo (NASDAQ: PDD), HUYA Inc. (NYSE: HUYA), Huami (NYSE: HMI), Mogujie (NYSE: MOGU), Lepu Medical (300562.SZ), Meituan (03690.HK), Ping An Good Doctor (01833.HK), Zhongrongjin (acquired by Homa Appliances), DeePhi Tech (acquired by Xilinx), Qian Dai Bao (acquired by Meituan), Fanpu Jinke, Beibei.com, Leqi E-commerce, DotC, Nuro, YITU, Roborock, Tiangong Intelligence, Zhuiyi Technology, Tigerobo, Oasis Labs, Beitai Haoche, QuantGroup, Shuidihuzhu, Testin, Doumi, BIGO LIVE, Danke Apartments, Qian Damai, Perfect Diary, Ucommune, and others.

- Gaorong Ventures has investment teams based in Beijing, Shanghai, Guangzhou, Shenzhen, and Hangzhou.

Long press QR code to follow Gaorong Ventures

Thank you, good friend of Gaorong