Chen Yaochang: World Factory + Social Media + Talent — More and More Global Brands Will Emerge from China | Ronghui

Over the next five years, we're bound to see more and more international consumer brands emerging from China.

Under China's "dual circulation" development paradigm, consumption's role as an economic engine has become even more pronounced, creating enormous entrepreneurial opportunities in the country's consumer sector.

What new global patterns have emerged in consumer businesses post-pandemic? What revolutionary infrastructure shifts are reshaping China's consumer industry? What's the latest in hot sectors like social commerce, fresh grocery retail, and C2M? And which other major consumer categories hold the most promise?

At a recent Gaorong Ventures · Ronghui closed-door online session, Gaorong partner Peter Chan drew on his years of strategic management experience in consumer industries to share insights with a global perspective and full-industry-chain outlook.

Chan previously served as Operating Partner at SoftBank's $100 billion Vision Fund and Vice Chairman of CP Group. From 2006 to 2011, he was President and CEO of Walmart China, and also held roles as Director for North Asia at Dairy Farm — Asia's leading retail group and the largest single shareholder of Yonghui Superstores — and Managing Director for Greater China at Bertelsmann Music Group (BMG). He currently serves as an independent director at Yum China (which operates KFC, Pizza Hut, and other brands), Hong Kong's Link REIT — Asia's largest real estate investment trust by market cap — and Australia's Treasury Wine Estates (owner of Penfolds and other brands).

Edited transcript below:

For many years, I've been in the consumer retail space and witnessed major industry transformations. In China today, whether it's the maturation of underlying infrastructure or the emergence of new technologies, new demographics, and new media, all of these are bringing endless vitality to the consumer sector. I believe today is the best era for entrepreneurship in consumer industries.

Global Consumer Business Shifts Under COVID-19 and China's Opportunities

The sudden COVID-19 outbreak this year posed major challenges to consumer retail industries worldwide. But compared to Europe and America, China's consumer sector has rebounded faster. Beyond effective pandemic control, there are more fundamental reasons.

1. Why Offline Retail Recovery in Europe and America Lags Behind China

We've seen that offline retail and shopping malls in the US and Europe have been hit far harder than in China. Among Europe and America's top ten REITs focused on shopping malls, the best-performing one has yet to recover to 40% of its pre-pandemic market cap. Many are now at just 10% of pre-pandemic levels, with several on the brink of bankruptcy. Beyond the immediate revenue collapse, many investors feel their medium- to long-term transformation efforts have been inadequate.

I don't attribute this solely to poor pandemic control in Europe and America — they'll eventually overcome COVID-19. The more fundamental issue is that even before the pandemic, they lagged far behind Chinese offline retail in new technologies, new business models, and especially the use of online social media. A quick look reveals that many shopping mall developments in Europe and America remain overly dependent on department stores, which have been in steady decline. This includes some rather antiquated retail formats that haven't been operated in ways suited to today's digital era.

First, they haven't followed the lead of many Chinese offline retailers in driving traffic and sales online. China's offline traffic continues to provide substantial dividends for both online and offline businesses — the key lies in digitalization. This includes China's restaurant industry, which has nearly a decade of history in digitalization and delivery services. The sector's online sales, data capabilities, and technology are far ahead of Europe and America. Today, Meituan's market cap on the Hong Kong Stock Exchange has surpassed $200 billion, while the largest digital food delivery platform in Europe and America hasn't even gone public and is valued at roughly one-tenth of Meituan's — illustrating the gap in restaurant digitalization.

Second, in China, many online-native brands were already expanding offline before the pandemic. They've helped numerous shopping malls reshape their customer composition to better suit the post-pandemic environment. This includes tea drink brands like HEYTEA and Nayuki; online-offline hybrid stores like Hema and Super Species; and Gaorong Ventures portfolio company Perfect Diary, which besides being a top online brand has accelerated its offline store rollout in recent years. This phenomenon is relatively rare abroad.

Additionally, Chinese social media has brought the influencers and viral moments it creates back into physical spaces, reviving offline traffic — an area where China has advanced far beyond Europe and America. Douyin has reinvigorated many offline scenes, and the entire WeChat ecosystem has become a multi-channel platform for our personal and professional lives, playing an important role in connecting online and offline traffic.

2. China's Position as the World's Factory Won't Change

During the pandemic, we also observed China's key industries evolving from light industry — apparel, footwear, general merchandise — to consumer electronics — mobile phones, home appliances, 3C products — and now to higher-value new industries like intelligent robotics, renewable energy equipment, batteries, autonomous driving, and new energy vehicles. I believe that despite trade war and tariff pressures, some low-value industries may relocate, but many will remain in China because the production ecosystem China has built is irreplaceable by other countries and continues to iterate, creating ever-larger moats. China's position as the world's factory will not change.

Another major realization: previously, most B2C commerce happened within a single country. During the pandemic, B2C truly began crossing national boundaries, with cross-border e-commerce developing very rapidly. During the outbreak, many items unavailable through traditional retail shifted online. For instance, numerous small Chinese merchants opened stores on Amazon, allowing overseas customers to directly purchase Chinese-made goods.

During the pandemic, Amazon China's business was two-sided. US customers could directly buy from Chinese brands and merchants; Chinese consumers could also purchase overseas goods through Amazon. During Amazon China's 2020 Prime Day "64-Hour Peak" period (October 12, 23:00 to October 15, 15:00), average transaction value per user far exceeded last year's figures, achieving double-digit growth, while new paid memberships grew 19x year-over-year.

Cross-border logistics infrastructure has also improved dramatically in recent years, making logistics costs affordable for merchants and further boosting cross-border e-commerce development.

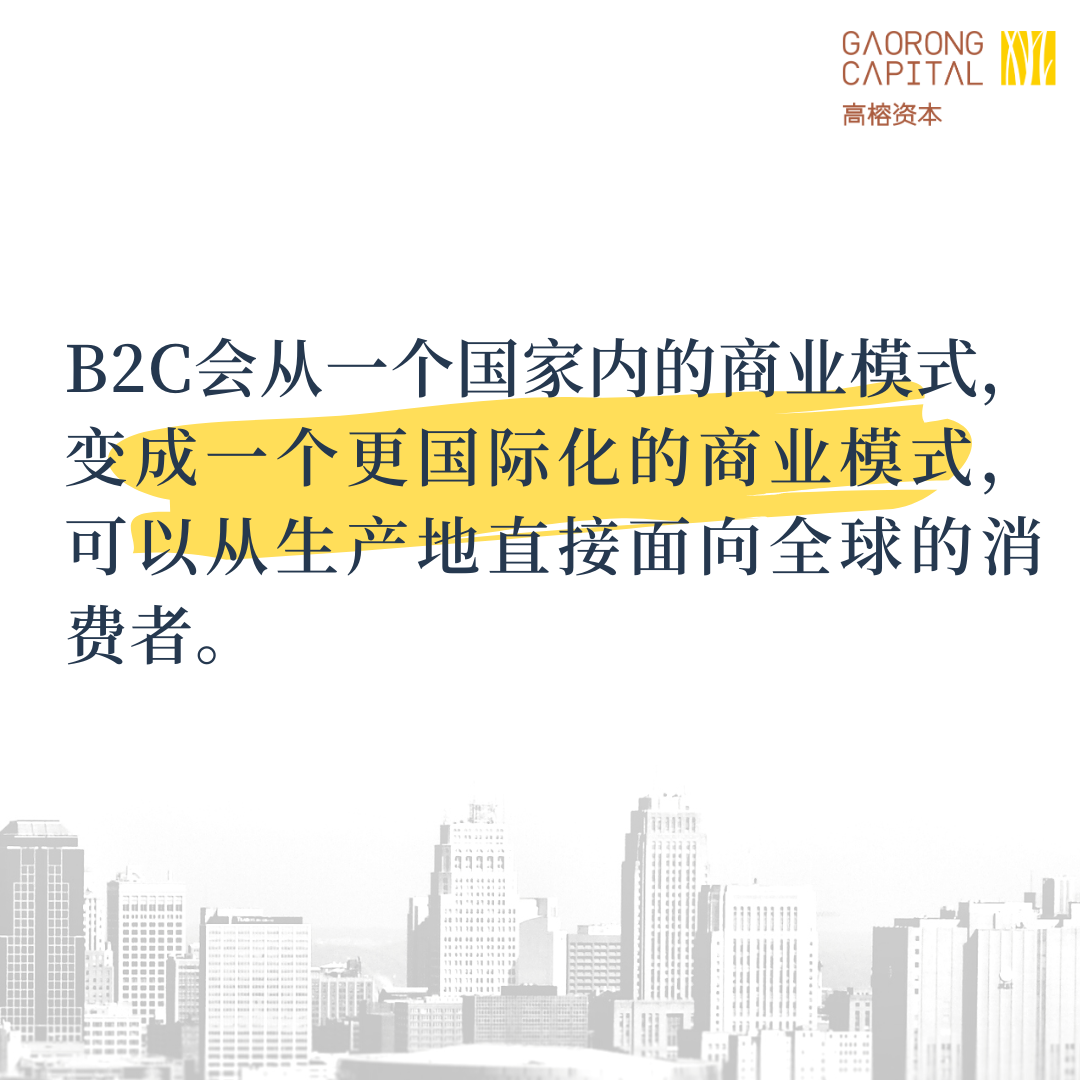

We believe B2C will evolve from a business model confined within individual countries to a more international one, enabling direct-to-consumer sales from production locations to global consumers.

China's position as the world's factory, combined with rapid cross-border e-commerce growth, can help offset the impact of trade wars and tariffs.

Revolutionary Infrastructure Changes in Consumer Industries

Let's examine some revolutionary infrastructure changes in today's consumer industry, starting with medium- to long-term technology drivers.

1. Medium- to Long-Term Technology Drivers

In recent years, we've seen continued investment in more traditional infrastructure including highways, aviation, high-speed rail, and subways. But the truly major investments are flowing into "new infrastructure" — 5G, cloud computing, big data, IDC (Internet Data Center), AI, and IoT. These investments form the foundational layer needed for new consumption, new retail, new logistics, and new supply chains going forward.

Second, robotics and automation have already found applications across many industrial and retail scenarios, continuously improving accuracy, precision, and safety while reducing costs, and helping achieve standardization in both industrial and consumer applications.

Another area I follow closely is new energy and new energy vehicles. If China is to meet growing energy demand, reduce emissions, and avoid massive dependence on imported coal and oil, the only path forward is large-scale renewable energy development — an inevitable long-term trend. This includes the enormous power demands from new infrastructure like 5G and IDC. Electricity may become the sole energy source for our industrial and consumer lives, creating vast development space for power generation and storage — battery technology.

Renewable energy has a distinctive characteristic: extremely low marginal costs. Early capital investment is high, but subsequent maintenance costs are very low. The result will be substantially lower energy costs. This will positively impact agriculture, industrial production, logistics and delivery, and retail spaces near residential areas. For example, energy costs account for 70% of total costs in large-scale greenhouse cultivation; commercial electricity costs for retail spaces near residential areas can run 20-30% of total costs. When power costs decline, these businesses gain enhanced competitive viability.

We believe power development will strengthen Chinese industrial and consumer industries' competitiveness relative to other leading nations, and together with China's leadership in batteries, will be a key factor in next-generation consumer product development.

2. China's EV Strategy and Global Position Are World-Leading

Alongside maturing new energy and battery technology, China's electric vehicle industry has also developed rapidly. Why does the EV industry hold such high value? The US auto industry supports 10 million jobs and contributes 3.5% of US GDP. According to official 2018 statistics from China's Ministry of Commerce, the auto industry directly and indirectly supported one-sixth of retail employment, with sales accounting for 10% of total retail sales. Moreover, as electric vehicles become a significant item in the oil-centered global energy market, they become part of a new ecosystem encompassing autonomous driving and ride-hailing.

We see China actively developing its new energy vehicle industry chain and expanding overseas. In September this year, China's NEV sales hit a record monthly high, up 67.7% year-over-year. Tesla has announced it will sell China-made EVs in Europe, representing recognition that China's EV manufacturing has reached world-class levels. CATL plans to increase its overseas market share from 2% in 2019 to 14% by 2025.

As China's EV supply chain advantages continue concentrating, it has potential to become a global EV industry leader. According to a Securing America's Future Energy (SAFE) report, of 142 lithium-ion battery gigafactories under construction globally, 107 are in China versus 9 in the US. Over the next 5-10 years, global automakers are expected to invest $300 billion in EV R&D and production, with nearly half of that investment occurring in China.

We're also seeing companies like NIO promoting automated battery swap models, which enjoy national policy support. Battery swap stations and charging networks have been written into government work reports as important components of new infrastructure. Swap models may further advance electricity as a mass-market daily consumer energy source.

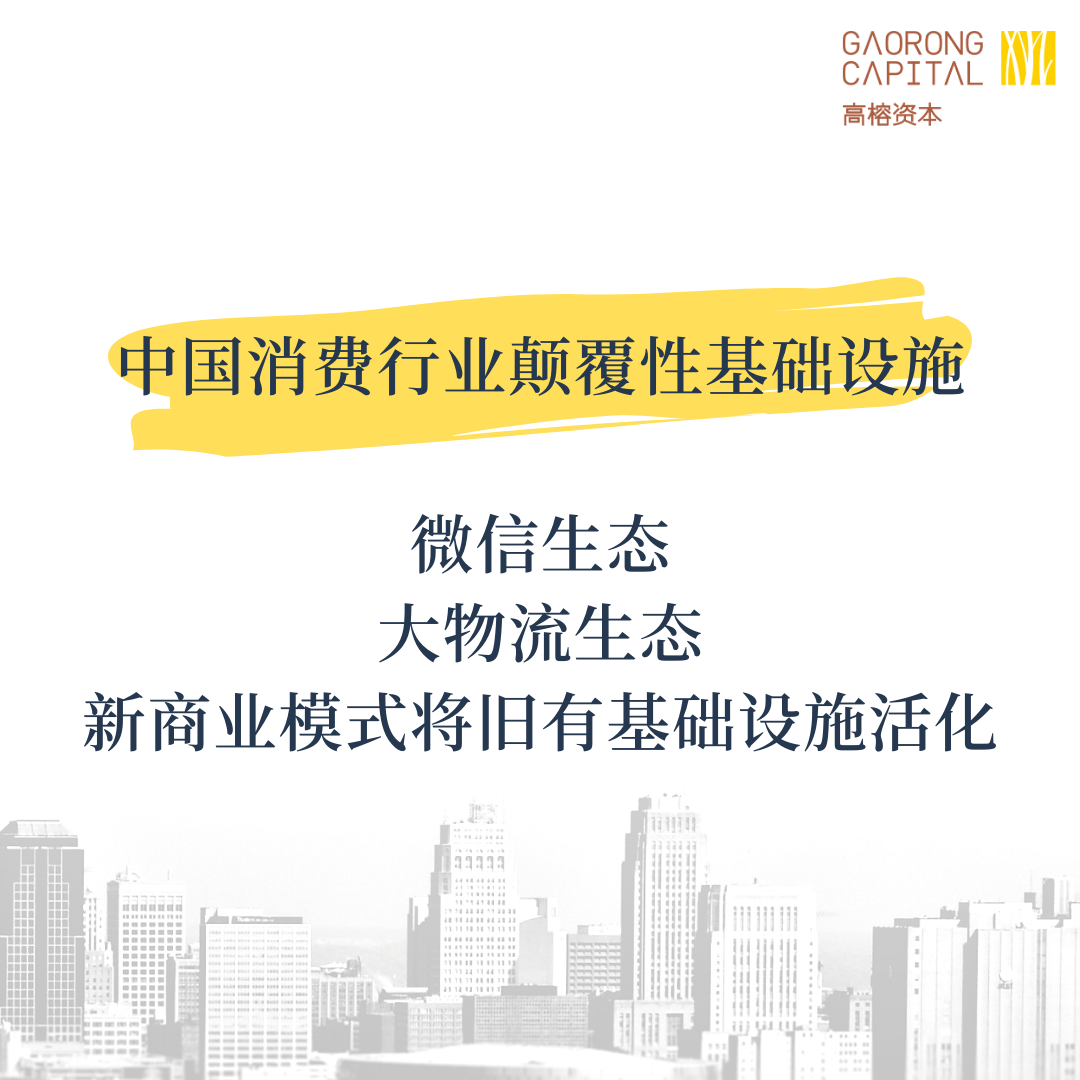

3. Disruptive Infrastructure Transformation in China's Consumer Industry

Looking at some disruptive infrastructure in China's consumer industry: first, China's WeChat ecosystem is continuously becoming an increasingly powerful and complete infrastructure layer. From e-wallets and online payments to now encompassing daily life, social networking, and local city services, this is a rather distinctive infrastructure for China. Social media platforms in the US including WhatsApp haven't achieved ecosystems as expansive as WeChat's.

Second, China's "macro-logistics ecosystem" has been continuously improving over the past two to three years. By "macro-logistics," we mean upstream factory and agricultural origin logistics, millions or even tens of millions of last-mile delivery drivers, and millions of community group buying leaders — a number still growing — who are connecting the entire ecosystem through various data communities and digital networks.

Third, we're seeing new business models revitalizing existing infrastructure. For example, with the rise of community group buying, countless mom-and-pop shops across China have been reactivated. Xingsheng Preferred, Pinduoduo, and Meituan have developed these shops as community group buying pickup points, serving as micro-logistics centers playing a low-cost role in last-mile fulfillment while also becoming important points for capturing traffic and providing membership services. These previously undervalued small shops have now been reactivated by new technologies and new models.

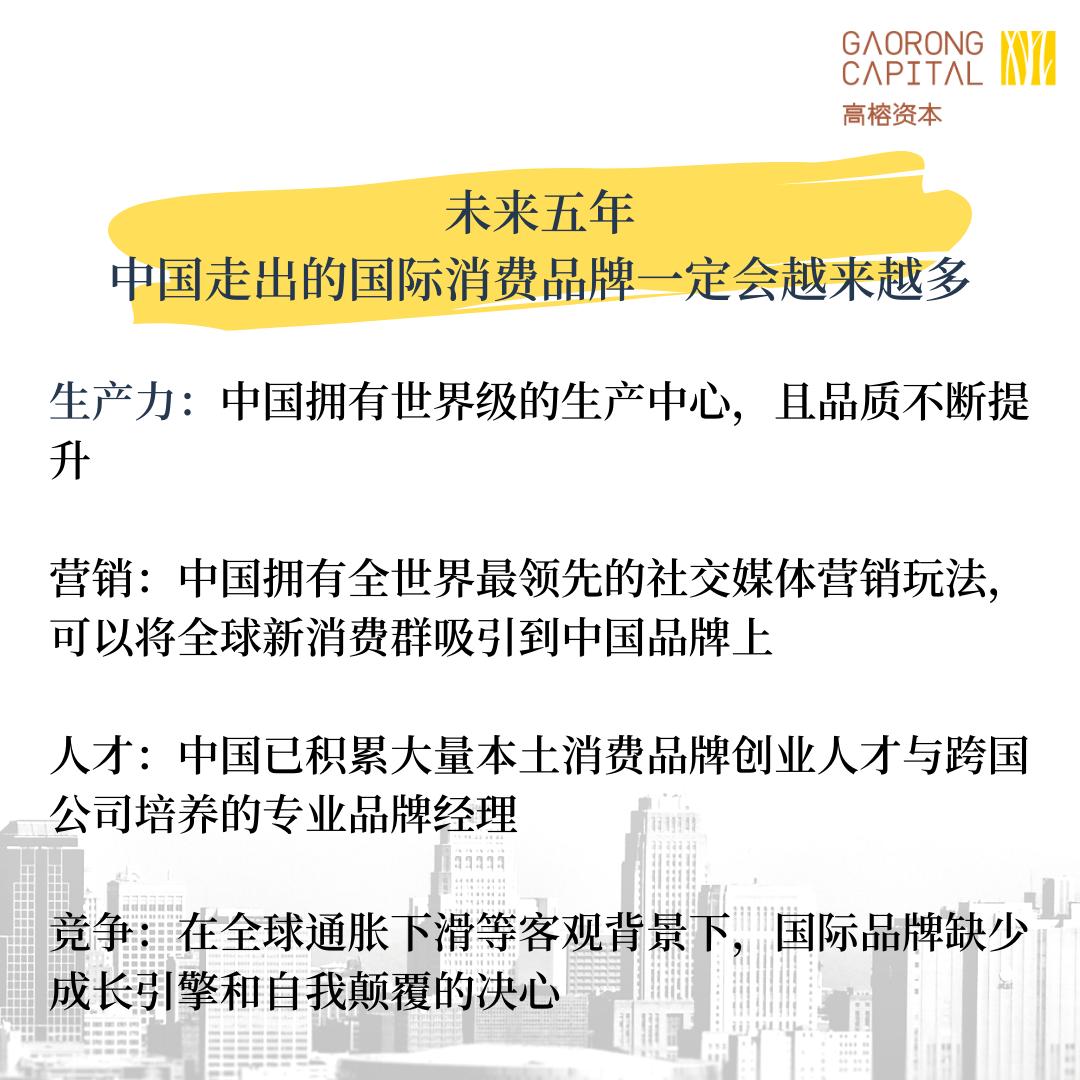

4. Over the Next Five Years, Increasingly More Chinese Brands Will Go Global

We believe Chinese brands will become more international going forward, and over the next five years, increasingly more Chinese consumer brands will expand internationally. Several major preconditions support this.

First, China has world-class manufacturing centers with continuously improving quality.

Second, China has the world's most advanced social media marketing playbooks — including social media, short video, and livestreaming — which we can take international, making it easy to attract global new-consumer demographics to Chinese brands.

Third, China has accumulated many excellent local consumer brand talents over the past two to three decades, plus professionally trained brand managers from multinational corporations — abundant human capital driving Chinese brands' internationalization.

A fourth driving force: major international consumer brand players are facing headwinds. First, global inflation has declined. When inflation was high, consumer goods companies could easily achieve revenue growth; today, traditional large consumer goods companies sorely lack growth engines. And they lack the determination to disrupt themselves through new R&D and new marketing. So as international majors face these objective challenges, numerous opportunities will be created.

5. In Chinese Brands' Internationalization, TikTok Will Play a Major Role

In the process of Chinese brands going global, TikTok will play a very important role. TikTok is the most successful internationalized product China has built in the shortest time. Its algorithms and AI match the needs of new consumer demographics. Across 30 countries worldwide, it ranks among the top in downloads, market share, DAU, and MAU — all through the same business model going global.

So if Chinese consumer brands understand how to market within the TikTok ecosystem, leveraging existing supply chains, brand management capabilities, and product strength, they can quickly reach many countries by following TikTok, replicating success across different nations with the same business and marketing models.

Comparing the TikTok and Douyin ecosystem with the WeChat ecosystem, WeChat has more B2B enterprise service elements, while TikTok is more globalized and its entire ecosystem is forming a closed loop — by which we mean traffic doesn't leave, and e-commerce transactions are completed within its own system. We're also watching developments following Walmart and Oracle's investments in TikTok.

Tracking Several Hot Consumer Sectors

Next, I'll share the latest trends in a few consumer sectors that have drawn considerable attention.

1. Traditional Retailers' Digital Transformation: Walmart

Among more traditional offline retailers transitioning online and into new media, Walmart has been relatively successful. Over the past three years, Walmart's stock has nearly doubled. Despite no major surge in sales or profits, its digital strategy and determination regarding new media, new demographics, and new retail development have received high marks from investors and investment banks.

First, its online business has maintained fairly strong growth — in fiscal 2020, Walmart's online sales grew 37%.

Second, they've made some very determined strategic moves, including selling offline stores in Brazil and the UK, and selling their India offline wholesale business; spending $16 billion to acquire Indian e-commerce company Flipkart; acquiring Latin American e-commerce platform Cornershop; and being a major investor in both JD.com and Dada Nexus.

More recently, they invested in TikTok Global. The rationale: as offline retail develops online, they urgently need to enter new social media — specifically social media targeting the most fashion-forward young people. Walmart's leadership has also stated they will collaborate with TikTok to provide e-commerce and other omnichannel services, developing social media shopping potential to attract young consumer groups.

So even though Walmart's strategy hasn't yet reflected in revenue and profits, their determination has won investor recognition — near-term profits aren't what investors care about most. Of course, this strategic transformation still needs to prove profitable in the medium to long term.

2. Social Commerce Is Capturing an Increasing Share of Consumer Spending

Social commerce has developed quite rapidly over the past two years, capturing a growing share of consumer spending. In 2019, social commerce transaction volume already accounted for nearly 20% of total national online retail; this year's share is expected to reach 30%.

Pinduoduo, as the sector leader, has maintained high growth rates in recent years. In Q2 2020, Pinduoduo's annual active buyers reached 683.2 million, up 41% year-over-year; GMV exceeded 1.2 trillion yuan, up 79% from the prior year.

Community group buying represents a major track that's continuously sinking deeper and becoming more grounded, well-suited to today's lower-tier market shopping behaviors. Spending just over ten yuan can satisfy many consumers' shopping and social needs, driving higher purchase frequency. After the pandemic, community group buying has seen a new round of growth with intensifying competition. Beyond independent leading community group buying companies — Xingsheng Preferred, Tongcheng Life, Shihuituan — major platforms have also entered: Meituan, Pinduoduo, JD.com, Alibaba, Meicai.com; and recently ByteDance and DiDi have joined the fray — something previously unexpected.

3. Fresh Grocery Retail: Who Wins?

In fresh grocery retail, the nearly 5 trillion yuan B2B2C market remains fragmented and will certainly become the largest source of growth in total e-commerce transaction volume.

New retail models and players in fresh groceries continue emerging. This includes offline new retail upgrades, represented by Alibaba (Hema, RT-Mart), Yonghui Superstores/Super Species, Walmart/JD.com, and Wumart/Dmall; front warehouses have also developed rapidly, represented by Gaorong Ventures portfolio company Dingdong Maicai and Pupu Supermarket; community fresh grocery stores, represented by Gaorong Ventures portfolio company Qian Damai and Yipin Shengxian in Hefei; and community group buying as previously mentioned, including independent leaders, major platforms, and new entrants.

4. AI and Big Data-Driven C2M Will Become Mainstream

The C2M trend will certainly become increasingly mainstream going forward. Based on developments in artificial intelligence and big data, the C2M model collects and analyzes consumer data, directly connecting to factories for production, achieving user demand-driven manufacturing, and in turn pushing upstream industry chain transformation and upgrading.

Several domestic leaders are already exploring this space. For example, Pinduoduo launched its "New Brand Initiative" at the end of 2018, using platform big data to provide R&D and production recommendations for small and micro manufacturing enterprises, reducing production costs and ultimately lowering end prices.

Also prominent in the past year or two is SHEIN, the international apparel company that's also representative of the C2M model. SHEIN's sales surpassed 40 billion yuan in June 2020 and are on track to reach 100 billion yuan this year. It ranks first among shopping apps in the Middle East, became the #2 shopping app in the US in June behind only Amazon, and is also wildly popular in Europe. Based on its data tracking system monitoring fashion trends and consumer changes, SHEIN can achieve rapid production — in 2019, it launched 150,000 SKUs.

Alibaba's Taobao Deals also focuses on "C2M custom goods as core supply"; including the recently launched Xiniu Zhizao, which in its initial phase targets the apparel industry, providing data-driven style selection, fabric joint releases, and e-commerce small-batch rapid-turnaround custom processing.

Currently, C2M is taking root first in highly fragmented, high-turnover industries. For example, the apparel industry has enormous SKU counts, with inventory and markdowns creating massive waste. Overall, however, C2M remains in early stages. The truly ideal C2M should achieve "thousands of faces for thousands of people," aggregating highly fragmented demand to drastically reduce supply chain waste and shorten production times. Even the most advanced cases we're seeing remain in early, exploratory phases.

Promising Major Consumer Industries for the Future

Finally, let me offer some thoughts on consumer industries we believe hold strong future potential, looking forward to more outstanding entrepreneurs continuously breaking new ground.

1. Health and Wellness Consumption

Across the health and wellness consumption track, there's still substantial room for evolution. First, combining AI, big data, and wearable device technology can help people better manage their health, opening many possibilities in lifestyle wellness. For example, Gaorong Ventures portfolio company NYSE: ZEPP has increased investment in healthcare-related functions, algorithms, cloud services, chip research, and new product development.

Moreover, over the past three to four years, China has made enormous strides in medical R&D investment and progress, with a batch of high-market-cap medical R&D enterprises emerging.

Health-related online-offline retail is also evolving, such as chain smart pharmacies and new-demographic-targeted health retail formats.

Additionally, as consumers today place greater emphasis on health, healthy, high-nutrition foods are gaining favor. People now consider overall internal health when purchasing food, including weight management or beauty connections. So food entrepreneurship can also consider how to help consumers better manage their health.

2. Opportunities in Lower-Tier and Rural Markets

We have high expectations for major developments in upstream agricultural digitalization. Currently, China's digital economy penetration has reached 36%, while agriculture stands at just 8.2%. Agricultural product supply chains remain highly fragmented, with costs accumulating layer by layer from origin to consumers and restaurants, and inefficient matching between demand and supply ends.

Some action is already underway. For example, Pinduoduo is building China's largest internet agricultural data platform; its "Cloud Farming" model uses big data and distributed AI to aggregate fragmented consumer demand, promoting origin-direct shipping — by the end of 2019, Pinduoduo directly connected with over 12 million agricultural producers. Meicai.com uses big data to forecast and analyze agricultural product prices and demand, helping B-end buyers adjust procurement plans and helping farmers adjust production strategies.

Compared to agricultural digitalization, what's developing faster is consumer goods penetration in lower-tier markets with over 900 million people. Beyond Pinduoduo continuously increasing penetration, Alibaba has launched Taobao Deals and Juhuasuan; JD.com is pushing Jingxi, its Lite App, and JD Daojia in partnership with Walmart; and community group buying continues sinking deeper, with Xingsheng Preferred already reaching down to township and village levels.

3. China Has Yet to Produce Chain Restaurant Brands on Par with America's

I pay considerable attention to the restaurant industry. Looking at global listed restaurant companies by market cap, we find the highest-valued companies are mostly American, especially fast food brands. Relatively speaking, Chinese chain restaurant brands — particularly fast food — lag far behind America. Fortunately, Haidilao's IPO gave us great encouragement.

By market size, we shouldn't be smaller than America, and Chinese restaurant enterprises have a decade of digitalization history. Why haven't high-market-cap chain fast food brands emerged? My preliminary analysis suggests the reason may be that Chinese chain restaurants haven't yet found effective standardization paths that can occupy a position in consumers' minds.

Compared to fast food, our chain tea drink brands — especially freshly prepared beverages — have grown faster in recent years, surpassing chain fast food brands in development, including HEYTEA, Nayuki, and Mixue Ice Cream & Tea. Why have excellent tea drink brands emerged? First, China has tea culture; second, it has domestic tea supply chains with abundant sources, plus abundant fruit production; and beverage standardization is much simpler than fast food.

I believe that based on China's massive market size, plus exploration of restaurant standardization and scale paths, China will absolutely produce a batch of highly valuable chain fast food brands in the future.

Today, China's consumer industry continuously sees new models and new brands emerging, with increasingly more companies mastering various playbooks. But as Chinese consumers mature, simply buying GMV through traffic will be far from sufficient. Only by returning to continuously strengthening and refining product capability, design capability, and supply chain capability will there be a foundation for long-term healthy development — truly winning in the new consumption wave.

Rong Report · October | Gaorong Ventures Completes Fundraising Exceeding 10 Billion Yuan

How to Manage Organizations and Incentives? Huawei's Former Financing Director: Respect Human Nature, Distribute Money Right, and Survive with Fear | Ronghui Gaorong Ventures' Rui Han Interprets Future Consumer Giants' "Battlefield": Transferable Trust Is What Makes a Brand