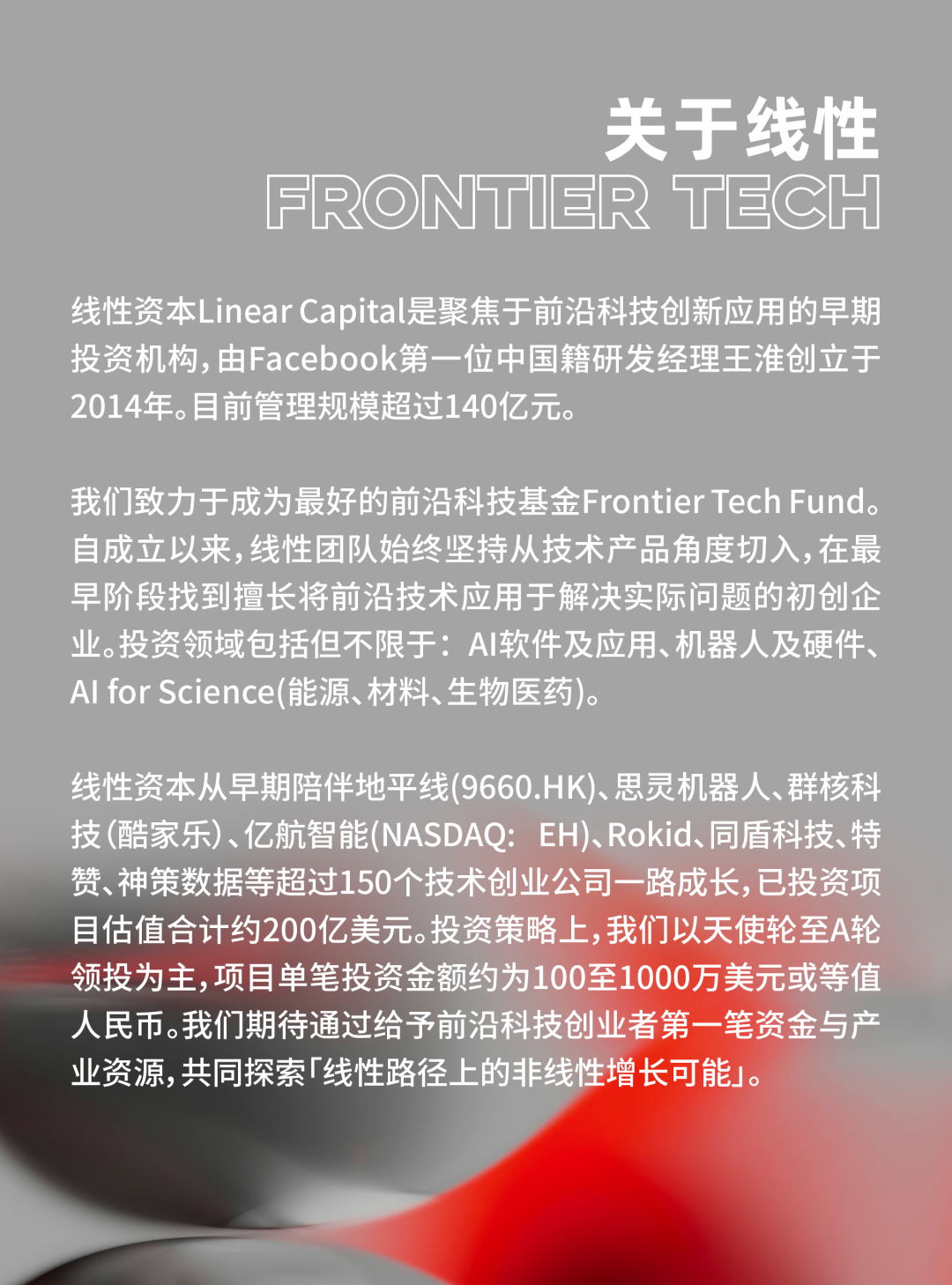

Linear Yang Jun: Young People All Want to Retire Early — I Tried It, and It's Not as Great as You'd Think | Linear View

The hardest thing in life is figuring out what you want.

Recently, Linear Capital partner Jun Yang sat down with nearly thirty students from the University of Pennsylvania for a live Q&A and in-depth exchange.

Over the course of two hours, Yang shared his reflections on his personal journey from PhD to entrepreneurship to investing, his take on the "FIRE" (Financial Independence, Retire Early) movement popular among young people, Linear Capital's criteria for evaluating founding teams, and how to spot opportunities in seemingly mature markets. We've distilled the highlights into this piece. We look forward to more young friends connecting with us in the future.

In July, the Penn Venture Club visited Linear Capital, where partner Jun Yang engaged in a live Q&A and deep discussion with nearly thirty students from the University of Pennsylvania.

Yang earned his bachelor's and master's degrees in computer science from Zhejiang University. After completing his PhD in computer science at Carnegie Mellon University, he worked as an engineer, engineering manager, and director of engineering at well-known Silicon Valley tech companies including Google, Facebook (Meta), and Square (Block). In April 2015, he returned to China as co-founder and CTO of Dada Group, leading the company to its NASDAQ listing in June 2020. After leaving Dada in 2023, he became an angel investor and advisor to multiple startups, and began sourcing deals alongside Linear Capital. This year, Yang officially joined Linear Capital as a full-time partner.

As a seasoned technical entrepreneur, during the nearly two-hour session, he drew on his own experiences and industry observations to explore topics the students cared about — from personal growth trajectories to industry trends and investment logic.

In his view, both personal career choices and entrepreneurship/investing require following certain internal logic and principles. For individuals, career decisions should be grounded in passion and growth — only by continuously absorbing new knowledge in a field you genuinely care about can you go the distance. For founding teams, capability is the foundation, vision ("yuanli") is the direction, and resilience ("xinli") is the support — all three are indispensable. Only with all three can one persevere through the grueling path of entrepreneurship. And in the world of investing and business, true opportunities often lie in insight into fundamentals and commitment to long-term value: not blindly chasing hot trends, but focusing on whether technology can solve real problems, uncovering latent demand, paying attention to offline executability, and waiting for breakthroughs brought by new technological variables — these are the keys to finding opportunity in complex markets.

When I graduated, I actually faced choices similar to what most students face now — either stay in academia for a faculty position, or go straight into industry. During my PhD, I was reasonably good at research and writing papers, so I had a decent shot at landing a respectable academic job.

But personally, I didn't find doing academic research that felt distant from reality particularly fulfilling. I was drawn to the process of technology landing in actual products — I found that pretty exciting — so I decided to go into industry.

At Facebook in the early days, there were so few engineers that everyone had a fairly direct line of sight to their impact. The first project I worked on was "People You May Know" — that little box on Facebook that kept suggesting "you might know this person." Only two or three people were working on it, yet the new friend connections formed through that feature every day were in the millions. At the time, it felt deeply rewarding that "tweaking an algorithm could mean millions of people becoming friends through our work every day."

Later, when I was an entrepreneur, although my title was CTO, that didn't mean I only cared about technology — I actually spent most of my time on operations. Business acumen isn't something you can only acquire through formal study or investment experience. If you're a core member who lives through a startup's growth, the training you get is comprehensive. For example, I considered myself an engineer with some business sense, but my experience building Dada really put my business skills through their paces.

After joining Linear to do investing, the business-minded skill that matters even more is figuring out how to spot opportunities before the market reaches consensus, and how to know talented people before they become successful founders. Our team is genuinely open-minded — whether you're still in school or working at a company, if you have entrepreneurial ideas, we're happy to spend time with you. By the time you actually start a company, we've built trust, and we can become better partners going forward.

The state young people often describe now is "lost" — many students complain that intense competition limits their options; others with impressive backgrounds still feel adrift at graduation despite having more paths open to them. For career choices, I have a principled suggestion: follow what you love, and embrace opportunities that maximize your growth.

First, do what you love. Don't force yourself to do things you resist. If something doesn't interest you, or you feel aversion to it deep down, you probably won't do it well. The foundation of a career should be "feeling it" — that internal drive is what sustains us.

Second, maximize your learning and growing. For young people choosing a job, many factors come into play: the work itself, whether you click with your manager, compensation... But among these, "can I learn new things" is especially important. Curiosity is the catalyst for growth — when an environment stops offering new knowledge and experiences, it's easy to grow restless. Among multiple options, the ones that expose you to the most new things and yield the most growth are usually the better choice. Being able to learn more builds a stronger foundation for whatever you do next.

"Retirement" is indeed a seductive word. It's not just young people today who have this trendy idea — I once craved it too. But my own experience trying it out: early retirement may not be as wonderful as you imagine. It can actually be pretty boring.

For the past two years or so, I was in a kind of "semi-retirement." Though I looked at some deals with Linear in an advisory capacity, I spent most of my time traveling the world with my family. But after I'd achieved the life goals I'd once wanted, I fell into a fairly boring state, and that was genuinely unpleasant. It's an unhappy state when life loses its sense of阶段性目标 (phased purpose), and this has nothing to do with whether you have the money to sustain that lifestyle. You'll find that even with financial security, you may not be happy. So my decision to return to investing full-time this year — sometimes I joke that I'm "re-entering the workforce at an advanced age" — actually reflects my re-clarification of what I'm passionate about at this stage.

Many young people today talk about "retiring early," but what they really want is to earn enough money to do what they want. The important thing isn't "early retirement" itself — it's figuring out what you actually want to do. Unless you've identified something post-retirement that's deeply meaningful and worth devoting the rest of your life to, you may find that state isn't really what you wanted. The hardest thing in life is figuring out what you want. There's no need to over-plan the sequence of how to get there. You can never assume the outcome of a path not taken.

Of course, some people say their "early retirement" goal is to start a company. To that I'd say: if you don't genuinely want to start a company, or haven't mentally prepared yourself, it's better not to. People who truly want to start companies don't ask themselves "why start a company" too much — you can see a kind of "yuanli" (visionary drive) in them.

Linear focuses on seed to Series A, and as one of the few domestic institutions that invests in early-stage technology from Day 1, our style is fairly distinctive. First, relative to Product-Market Fit, Linear pays more attention to Technology-Problem Fit — mainly whether the technology can solve a problem, and whether that problem is a "real problem."

On the other hand, we've distilled our experience evaluating founding teams into three dimensions: First and most foundational, do they have "capability" — this needs little elaboration.

Second, "yuanli" (visionary drive) — can the team genuinely imagine what this product will look like when built and used by people, and can they infect investors like us with that vision, making us believe you have the strong original intention to achieve it? Rather than looking around at what friends with similar backgrounds are doing, thinking you could do it too, assembling a team, and starting to fundraise.

Finally, "xinli" (heart-force/resilience) — that's the grit to face the hardships of entrepreneurship, whether internally you can hold on and get through truly brutal moments. Saying it's nine deaths and one survival is no exaggeration. Along the way, there may be many moments where you feel years of work might be for nothing. At those times, it's not a physical contest — it's about whether your xinli can carry you through.

We see "capability" as the threshold for whether you can start, but whether a company can grow big depends more on "yuanli" and "xinli." Investing in early-stage technology isn't static — environment shapes founders, markets shape them — so as we accompany founders in their growth, we're constantly observing how they respond to various trials.

Many tech startups face questions about equity structure for technical teams. In the long run, an individual's equity should match their contribution to the company — that is, it should correlate with the technical co-founder's actual contribution to the business. Time is also a useful factor: generally, the earlier a technical co-founder joins, the higher their relative contribution tends to be, and thus the higher their equity stake. If someone joins after the company already has some business foundation, their equity percentage would be relatively lower.

From an investor's perspective, we don't judge a company's quality based on whether it gives its CTO high or low equity. For example, in finance-heavy companies where technology is just one component, the CTO's stake might be smaller. Correspondingly, in some technology-dominant companies, the CTO might have a larger stake that matches their capability and contribution — and investors are fine with that.

What people may worry more about is that "equity is hard to adjust later." But in fact, many startups now have mechanisms for this. Even founders' shares are subject to vesting rules. Typically there's a four-year vesting schedule with gradual annual cliffs — even shares under one's name are earned over time. Additionally, there are technical means to ensure an individual's equity returns match their actual contributions. And for companies, through ESOP (Employee Stock Ownership Plan) pools, there remains considerable flexibility to adjust based on employee contribution levels.

Seemingly mature markets still hold opportunities — the key is whether you can step back from chasing hot trends and return to business fundamentals. Linear stays fairly cool-headed in investment decisions; we have a hard time buying into things that slap AI buzzwords onto concepts, and instead focus on whether technology can genuinely solve problems and create commercial value, spotting opportunities before consensus forms.

The emergence of new technological variables can bring fresh opportunities to stable markets. This can be as transformative as changing an entire industry — before Tesla, the auto market landscape was basically settled, with no new brands rising for decades, but electrification broke the deadlock, not only enabling Tesla's breakthrough but also catalyzing the new energy vehicle explosion. Or it could be that an industry already has mature solutions, but if your technology brings something different, solves specific pain points that remain unaddressed, and delivers incremental value, we'll still pay attention to that opportunity.

Cases of latecomers surpassing incumbents abound across industries. For example, Agile Robots, which Linear previously invested in. If you're familiar with industrial robotic arms, you know that robotic arms themselves aren't new in industrial automation. Auto factories have plenty of robotic arms working, but they can't do particularly delicate tasks because they lack force control. Agile solved this pain point with technology, enabling robotic arms to perform very fine operations.

If we'd said "there are already so many robotic arms on the market, so we won't invest in robotic arms anymore," we would have missed that opportunity. We still carefully analyze whether your technology matches the problem you're trying to solve — whether it can solve problems others can't, or solve them better than others. We discovered Agile at the earliest stage and continued to double down; it rapidly grew into a unicorn within four years, now valued in the tens of billions of RMB, generating substantial returns for our fund.

Additionally, offline executability is a factor that can't be ignored. Especially for more "grounded" industries, online efficiency gains matter, but the offline implementation link matters too — some unavoidable "dirty work" is key to keeping operations running.