Harry Wang: When Quantum Mechanics Meets Early-Stage Investing — An Alternative Reading of the de Broglie Formula | Linear View

A Rambling Conversation on Early-Stage Investment Thinking Across Dimensions

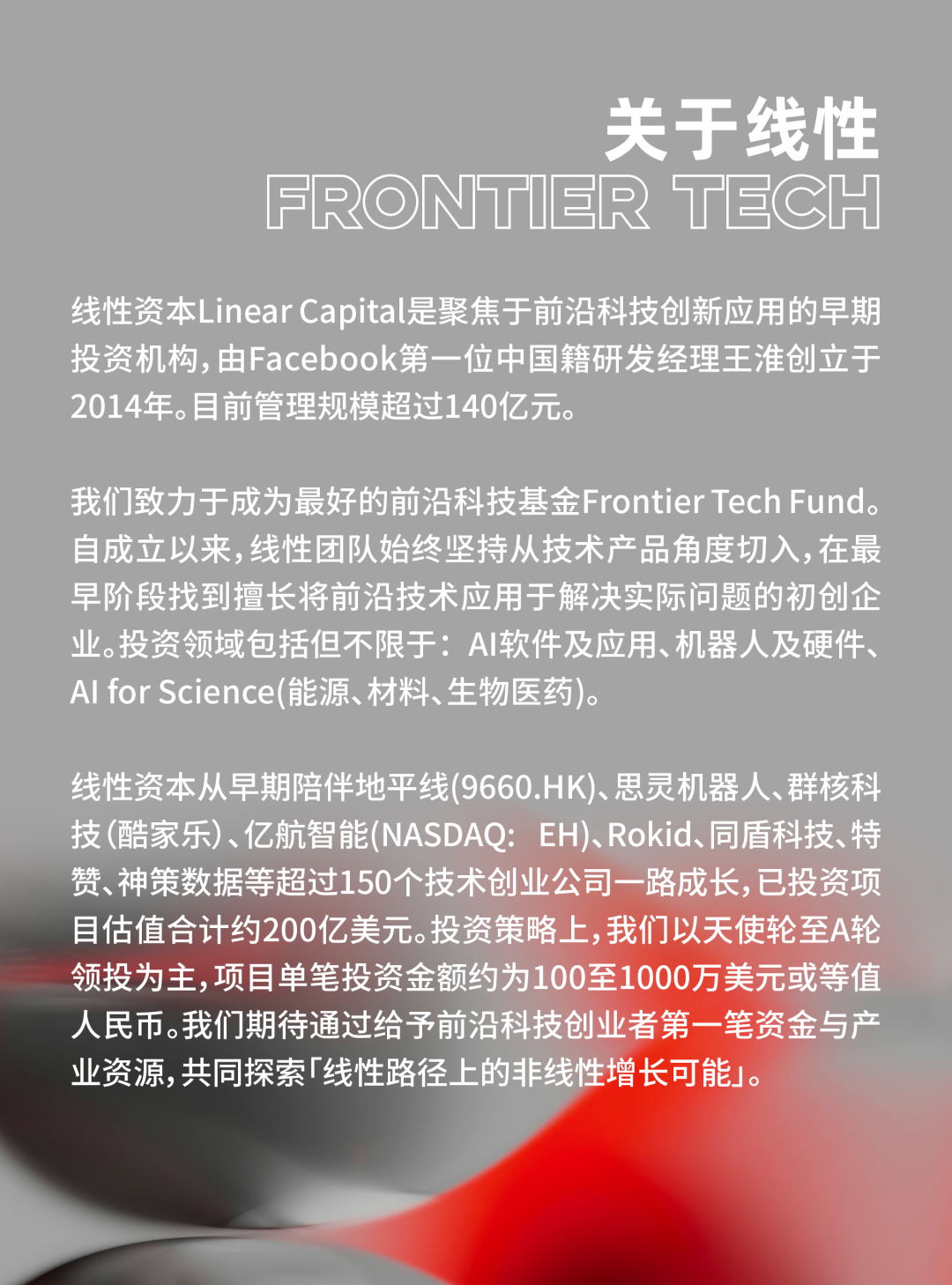

Founder, Linear Capital

Boosting Momentum (Strengthening the Founder's "Mass" and the Team's "Velocity")

In the unpredictable world of early-stage investing, we're always searching for a compass that can cut through the fog. Some rely on experience, others on intuition — but few would think to look to quantum mechanics for answers.

That might sound absurd. After all, quantum mechanics describes the strange behavior of subatomic particles, while early-stage investing is about business decisions in the macro world.

Yet when we set aside scientific rigor and approach it with an open mind, certain patterns from the quantum world might offer fresh insight into how we understand early-stage investment.

The inspiration for all of this comes from a classic physics formula: de Broglie's equation

In this formula, h is Planck's constant (a fixed, unchanging value), p is momentum, and λ is wavelength. This equation reveals the "wave-particle duality" of matter — the principle that all matter simultaneously exhibits both particle-like and wave-like properties.

Now, let's boldly apply this formula to the context of early-stage investing.

If we analogize λ (wavelength) in de Broglie's equation to "uncertainty about how things will unfold," then p (momentum) becomes the force we use to counter that uncertainty. The formula tells us that when the constant h remains fixed, if we want to minimize uncertainty (shrink λ), we must increase momentum p.

In physics, momentum p equals mass m times velocity v (p = m⋅v). What's interesting about this analogy is that we can make the two variables "mass" (m) and "velocity" (v) concrete, mapping them onto key elements in early-stage entrepreneurship and investing.

In early-stage investing, the "particle" we invest in is the entrepreneur themselves. The "mass" (m) an entrepreneur possesses isn't about their body weight — it's the core traits and accumulated resources they bring to bear in pushing a project forward.

This includes their passion, commitment, depth of cognition, domain expertise, and prior experience. The stronger these traits, the greater the particle's mass, the more stable the project, and the lower the risk for investors.

Yet an interesting paradox emerges here. Many groundbreaking, world-changing ventures were created by young people lacking experience and capital. Their "mass" in the traditional sense (past experience, financial capital) was small, but what they demonstrated — an unstoppable passion, radical commitment, and unwavering belief in their vision — was a more pure and powerful form of "mass."

We can distinguish between these two types of "mass":

1) The "mass" (m) of experienced entrepreneurs

- Deep industry knowledge: Past accumulation gives them profound insight into specific domains, enabling more accurate judgment of market trends and potential risks.

- Extensive network resources: These connections help them quickly access resources, find partners, and receive support when facing difficulties.

- Steady risk management capability: Having weathered storms, they're better at assessing and mitigating risks — critical for long-term project stability.

2) The "mass" (m) of young entrepreneurs

- Disruptive innovative thinking: Unbound by tradition, they can propose entirely new business models or technical approaches that break industry conventions.

- Rapid learning and adaptability: Like sponges absorbing new knowledge, they can quickly adjust strategy in constantly changing markets.

- Fearless execution: Full of drive, they rapidly translate ideas into action without fear of failure.

Neither type of "mass" is superior. They represent particles at different energy levels. The experienced founder's "mass" comes from deep accumulation; the young founder's "mass" springs from pure explosive force. What investors must do is recognize and evaluate different types of "mass," matching them to project needs.

If "mass" (m) represents a founder's internal accumulation, then "velocity" (v) reflects their efficiency in converting that accumulation into concrete action.

In the entrepreneurial context, "velocity" isn't simply about speed — it's a composite capability: product iteration speed, market trial-and-error speed, and financing progress speed, among others.

In a startup's earliest days, the journey from zero to one is filled with unknowns and uncertainty. If a team cannot quickly land an idea, learn from market feedback, and rapidly adjust direction, then even the greatest "mass" cannot generate enough momentum to reduce uncertainty.

- Product iteration speed: This is the ability to translate strategy into action. A team with strong execution can rapidly develop prototypes, launch tests, and gather user feedback.

- Market trial-and-error speed: Entrepreneurship is a learning process racing against time. Quickly learning market needs, competitor movements, and new technologies is key to team growth. What matters is learning from mistakes and converting them into future success.

- Financing progress speed: Fundraising isn't just capital injection — it's validation of the team and project. Closing rounds quickly provides abundant "fuel," allowing the team to focus more on product development and market expansion.

These three are tightly interconnected, forming a complete "velocity" system for a startup team. Rapid learning helps teams avoid detours; willingness to trial and error extracts valuable lessons from failure; together they ultimately improve execution, accelerating product iteration and market expansion.

An interesting phenomenon: the greater the "mass" (m), the greater the inertia. In our analogy, this means experienced, deeply accumulated entrepreneurs sometimes struggle to change direction because of their past successes — like a massive truck unable to take a tight corner at speed.

So how do we pursue high "velocity" while avoiding a "crash" from excessive "mass"? This is a question worth deep reflection.

We believe the answer lies in openness and radical candor.

Whether founder or team member, everyone needs an open mindset — willing to accept different opinions and learn from internal and external feedback. Like a skilled race car driver, you need not only speed but also alertness to every detail of the track, with precise control when necessary.

This means:

- Courage to admit mistakes and learn: Successful entrepreneurs aren't those who never err, but those who quickly recover and convert errors into valuable experience.

- Listen to internal and external voices: Regularly engage with team members, investors, mentors, and users — examining your decisions from multiple angles.

- Let go of ego: Humility allows founders to truly listen to others and make wiser decisions.

This capacity for "high-speed cornering" is one of the key traits distinguishing successful from failed entrepreneurs. It demands that while maintaining rapid forward motion, we remain like a precision gyroscope — always balanced and stable.

Some might question whether forcibly applying a micro-world physics formula to macro-world early-stage investing is too much of a stretch. Does this analogy have any scientific validity?

Of course, from a strict scientific standpoint, no direct causal relationship exists between the two. We're not trying to prove that early-stage investment laws can be precisely calculated with physics formulas.

Yet the value of this analogy lies precisely in breaking down mental boundaries. It provides a fresh perspective, helping us make concrete and discussable the abstract, complex concepts of early-stage investing as "mass" and "velocity."

It reminds us that uncertainty (λ) in early-stage investing is objectively real — we cannot eliminate it entirely. But we can reduce it by boosting momentum (p): strengthening the founder's "mass" (m) and the team's "velocity" (v).

Ultimately, whether quantum mechanics or early-stage investing, both explore a common theme: how to find patterns, perceive essence, and make optimal decisions in a world full of uncertainty.

This cross-dimensional thought experiment may not provide a standard answer. But it can at least light a lamp, helping us see more clearly through the foggy path of entrepreneurship and investing.