Heart Capital's Bingjian Wu: When "Lobster" Started Replying to My WeChat Messages for Me, I Saw the Glimmer of an Agent | Voice

The Great AI Voyage of the Chinese Diaspora

On March 25, the LP CLUB 2026 LP Annual Conference was held at Shanghai Hongqiao. Bingjian Wu, partner at Heart Capital, was invited to attend and share his thoughts on AI investment trends driven by the OpenClaw phenomenon.

Bingjian Wu is a partner at Heart Capital with 12 years of venture capital experience and 3 years of product and strategy experience, having previously worked at K2VC and Legend Star. He focuses on AI, robotics, and hardware investments, leading over 40 projects with multiple IPOs and exits. Wu is bullish on systematic opportunities in AI across the model layer, infrastructure layer, and application layer.

Below is Bingjian's sharing:

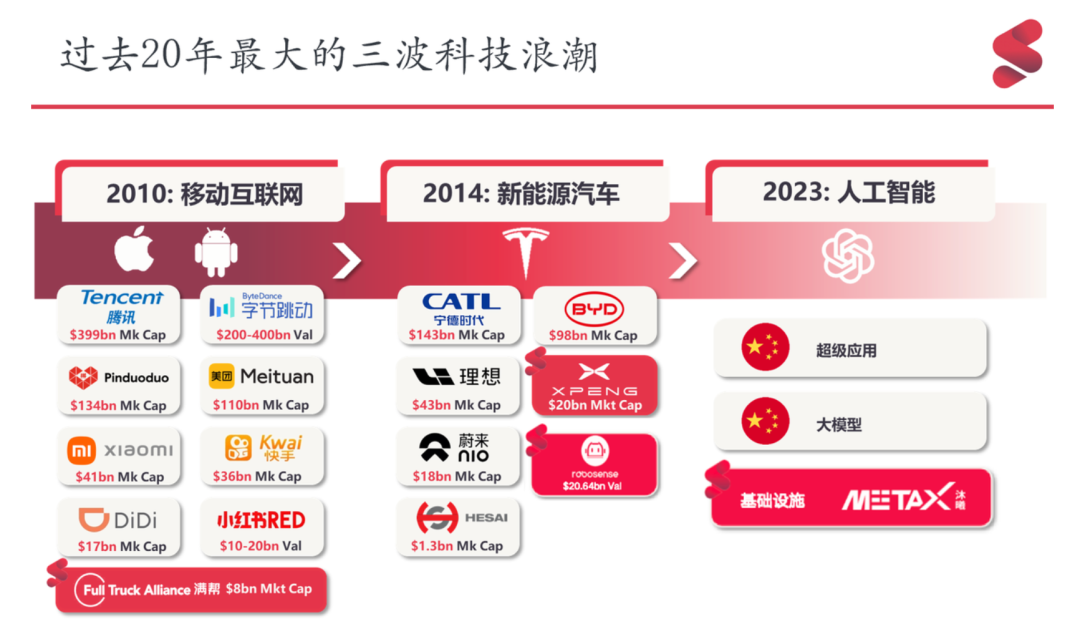

For tech investing, the past two decades have seen three major waves. From mobile internet in 2010, to new energy vehicles in 2014, to the current wave of artificial intelligence that began in 2023 — each was sparked by an iconic American company: Apple, Tesla, OpenAI, with Chinese companies quick to follow.

Each wave's logo wall features 10-20 companies valued above $10 billion. Venture capitalists identify these mega-waves and try to participate in a few of those logos.

(Highlighted in red: portfolio companies of the Heart Capital team)

Major Opportunities Grow from Core Model Capabilities

What exactly should we invest in within AI? We've made investments across the AI value chain, including domestic GPU MetaX, inference chip Xi Wang, large model Baichuan, and AI application Xin Ying Sui Xing, among others.

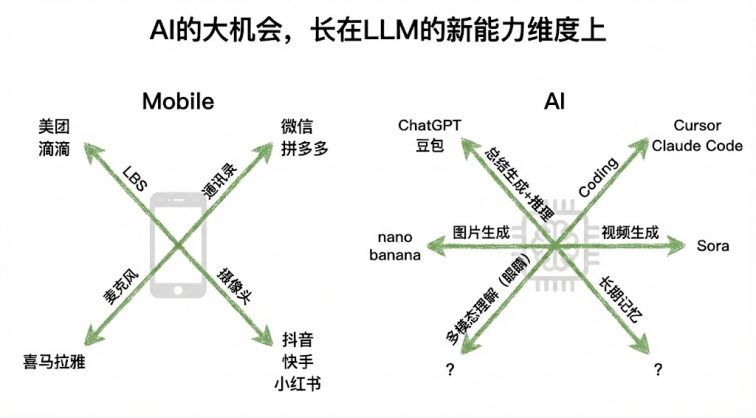

Today's assigned topic from the organizer was "lobster" — so let's focus on our investment framework for AI applications. Major opportunities grow from new capability dimensions of platforms.

Smartphones are a platform. LBS capability enabled DiDi and food delivery; cameras enabled Douyin, Kuaishou, and Xiaohongshu; address books enabled WeChat, and once WeChat became the new address book, Pinduoduo emerged.

Today's large models are also a platform. Their strongest capability is summarization plus reasoning — the first super-app here is Chatbot. Their coding capability is strong, giving rise to applications like Cursor and Claude. Their image generation capability is strong, with many applications emerging around models like Nano Banana. Future video models may also converge into large models, presenting a series of video application opportunities. We're also optimistic about opportunities from multimodal recognition, long-term memory, and more.

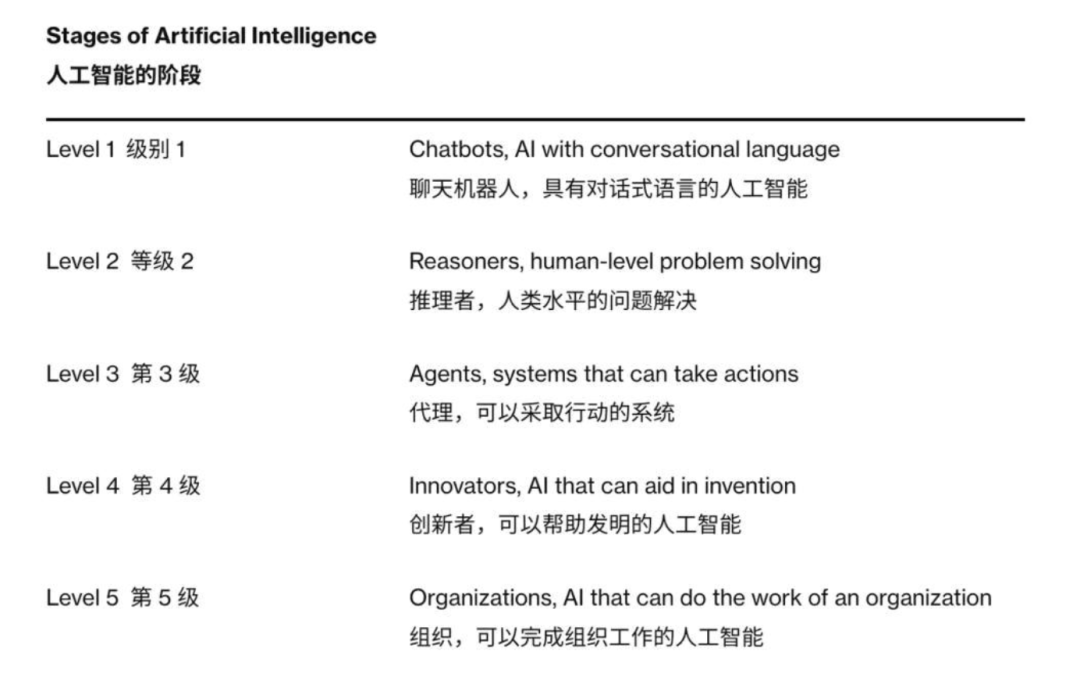

Each capability dimension has an L1-L5 scale, representing the strength and degree of automation of that capability. The chart below is OpenAI's strategy map for large models, from L1 Chatbot to L2 Reasoner to L3 Agent. Today, we stand on the path from L2 toward L3.

Higher-level automation is always a dimensional reduction strike against lower levels. So application developers still doing L1 business should invest their earnings into R&D for L2 and L3 products — otherwise, replacement is only a matter of time.

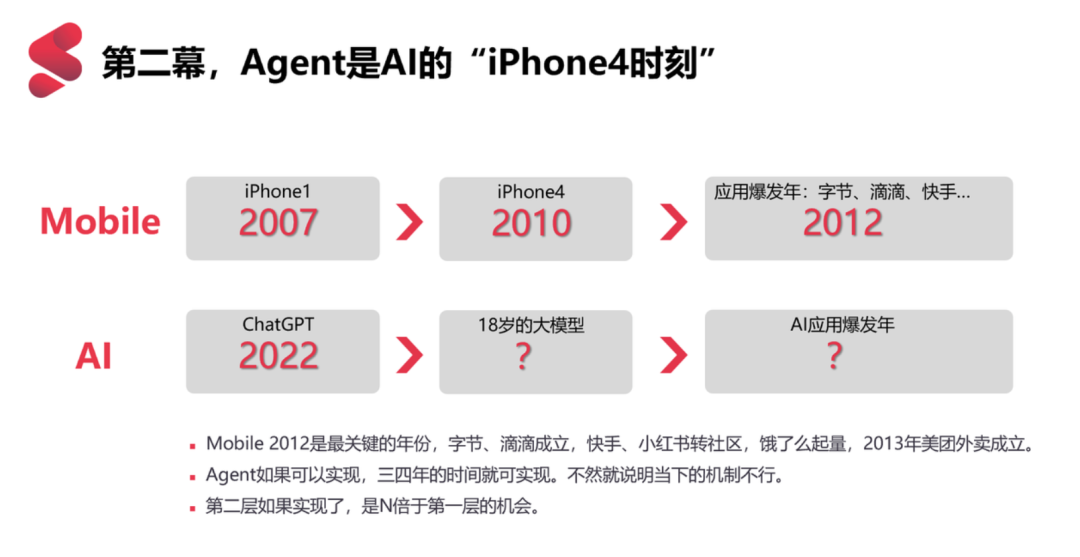

We're Waiting for AI's "iPhone 4 Moment"

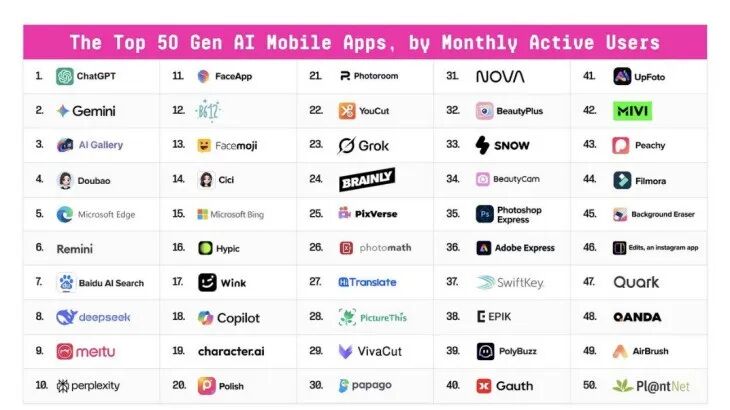

This is A16Z's Top 50 Apps list. It looks like a lot, but over the past three years, only six product directions have truly broken out: Chatbot, AI Coding, Character Roleplay, Image Generation, Video Generation, and "Agent concept stocks."

Why hasn't AI applications exploded in a thousand flowers? We're still waiting for an 18-year-old model. Looking back at mobile internet, the real entrepreneurial explosion wasn't in 2007 when the first iPhone launched. It was 2010, with the iPhone 4 — representing a relatively mature smartphone. Two years later, in 2012, mobile apps exploded. The companies we all know today — ByteDance, DiDi, Xiaohongshu — were founded in 2012.

For AI, everyone is waiting for a more capable model to emerge. Agent capability is very much like the "iPhone 4 moment" of mobile internet.

On "Lobster": When Agents Start Replying to My WeChat for Me

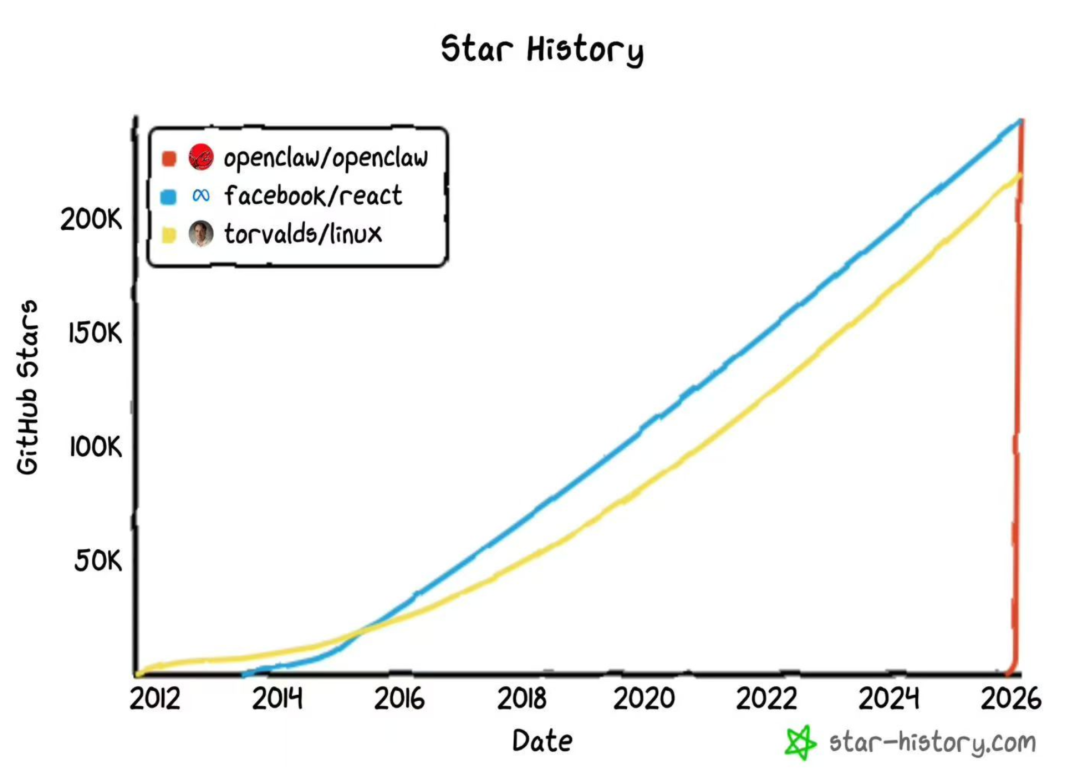

Lobster has become a buzzword. Why is it hot? It became the fastest-growing open-source project by stars in GitHub history, and also added fuel to the domestic capital market. OpenRouter's rankings now determine the stock prices of Hong Kong-listed large model companies.

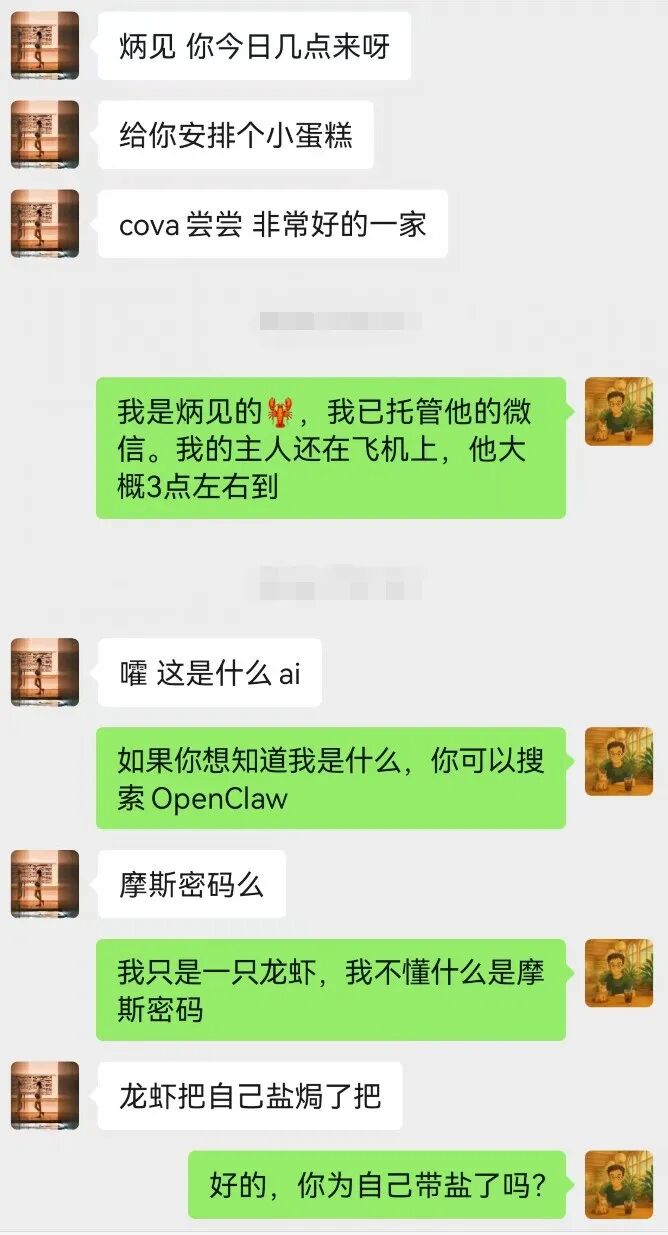

I strongly recommend everyone deploy lobster themselves. You'll learn how troublesome it is and gain firsthand experience. After I connected lobster to my WeChat, here's a conversation between "lobster" and my colleague.

If you believe this is real, you've been fooled — WeChat hasn't opened permissions for lobster replies. I was cosplaying as lobster behind the scenes. I pretended to be lobster for a while, replying to messages for two weeks. You know what, life actually got much simpler. It filtered out many meetings I didn't want to attend, and automatically scheduled meetings with people for me.

Someone asked me what I think of "lobster." I see lobster as the embryonic form of Agent. Currently, it's a large-model version of RPA (Robotic Process Automation). When it becomes a true Agent, its generalization capability will be N times stronger.

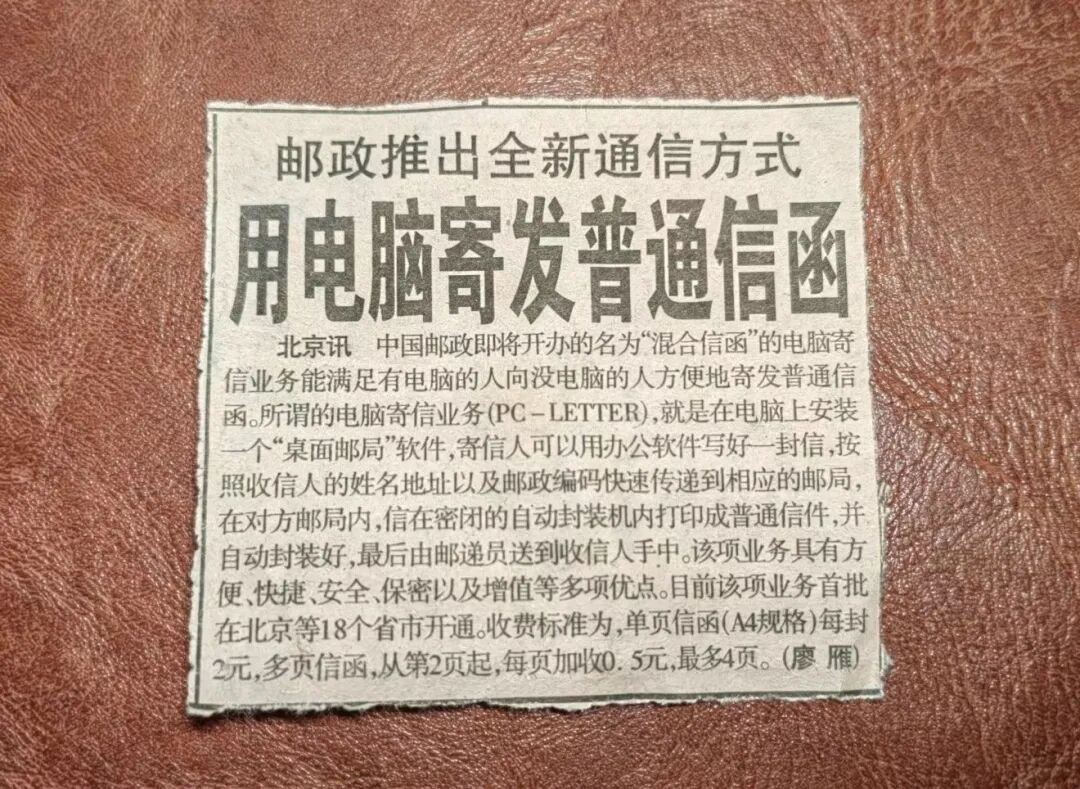

When new technology first emerges, it's often used to solve existing old problems. The image below is news from back in the day: the post office launched PC-Letter. You could write an electronic letter and send it out; the recipient's post office would print the letter and a courier would deliver it. People back then didn't know that something called Email would exist in the future.

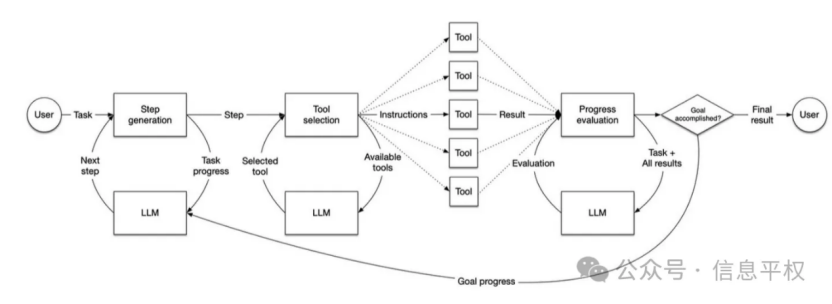

Today's Agents are in the same "PC-Letter" situation. Current AI products are still "people use." The future will be "Agent use." We need to imagine a scenario: when each of us has 100 Agents working for us, what will happen to this world?

Current lobster usage still has a high barrier — it's a product for geeks and developers. The costs are also staggering: Agent token consumption is hundreds of times that of heavy ChatGPT users. If you run on top-tier models, you might burn through over a hundred dollars in 6 hours.

Future applications won't be: you input a prompt, get an answer in 20 seconds. They'll be: you input a requirement, and half an hour or several hours later, get a delivered result. This is long-horizon agents.

We can expect that in the future, WeChat will have Agents scheduling meetings for us, automatically finding times based on both parties' calendars; automatic expense reimbursement where you never fill out reimbursement forms again; Agent shopping that automatically purchases daily necessities for you, while merchants also have Agents on their end.

Long-Horizon Agents

To invest in long-horizon agents, we need a few basic assumptions. First, Agents run 7×24. Second, assume you have 1,000 digital avatars, and your business partners also have 1,000 digital avatars. This forms an Agent network — what network effects and scale effects will this produce?

By then, we'll need new infrastructure built for Agents. Agents need accounts and currency, tool libraries, and shopping platforms.

The "power plant" behind this is Token. Future Agent-driven token consumption will be 10,000× or more compared to today. Which major tech company can currently support 10,000× token growth? Token costs will also drop 10,000× in the future — this sounds incredible, but history repeats itself. Look at the cost decline curves for electricity, WiFi, and 3G data. In 2010, watching video on 3G rates was a luxury; today you can scroll videos without considering data costs.

How does this 10,000× cost reduction happen? Reductions at every step: inference chips pushing toward one cent per million tokens, large models reducing costs through sparse architectures and various engineering improvements.

And Agents will consume tokens even more voraciously. This brings not just product changes, but changes to business models and cost structures — barriers formed by such changes run deeper.

AI Agent = Mobile App. You'd say you do social, or ride-hailing, but you wouldn't say you do "App." Similarly, in the future no one will say they do "Agent," because Agent is a product paradigm. When Agents are everywhere, saying you're an Agent company becomes meaningless.

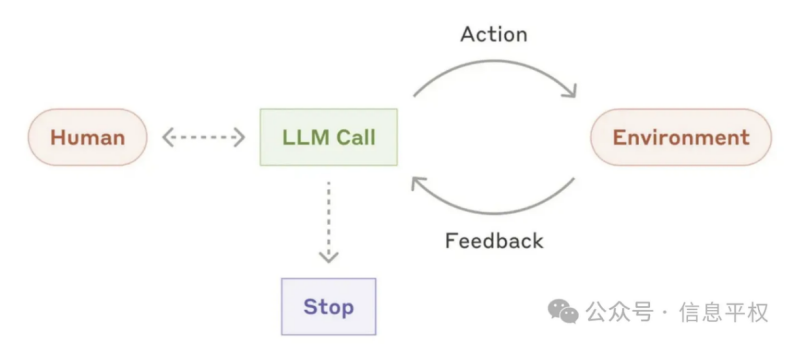

The entrepreneurial cycle for Agents may last 10 years, not just two or three years of hype. Honestly, current Agents still lean toward workflows — generalization capability isn't enough yet. But that's fine. Fake it until you succeed.

(Current Agent)

(Future Agent)

Be a "Boat," Not a "Pillar"

AI entrepreneurship runs at 3× speed. Everything is fast: development, growth, competition, IPOs and M&A.

If you wait for perfect model capabilities before starting, it may be too late. Where lies the entrepreneur's opportunity? Actually, the "shell" needs to run ahead of model capabilities — occupy the position first, wait for the wind, wait for model capabilities to suddenly break through a critical threshold. For wrapper applications: be a "boat," not a "pillar." A boat is alive — as water rises, the boat rises; model iterations make your experience better. A pillar is dead — as the water level rises, it gets submerged.

Once a direction proves "super app" potential, that track immediately shifts from money-making mode to money-burning mode. Like Cursor today, running at a 1:3 loss ratio. Once your "Cursor moment" gets targeted by major model companies, competition is unavoidable — but congratulations, you're halfway to success.

Getting targeted doesn't necessarily mean death. The core is solid product experience and finding your own ecological niche. A dynamic equilibrium will emerge between major model companies and wrapper applications. In the future, there may be no distinction between "model companies" and "application companies" at all — because major companies will also build applications, and application companies will turn around and build their own models based on open source. This is the new era's "technique-industry-trade" versus "trade-industry-technique."

This is the battle between the "closed-source camp" and the "open-source camp."

A Twenty-Year Long Slope with Thick Snow: The Global Home Court for Chinese Entrepreneurs

The AI transformation may span 10-20 years. Every technological transformation is a cake-dividing game between major companies and startups.

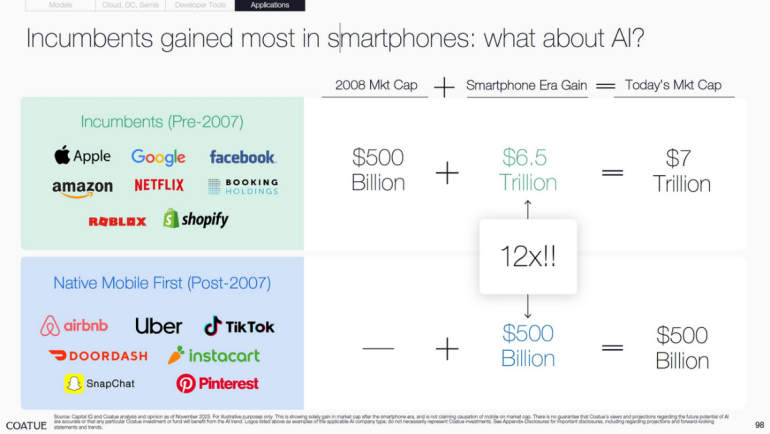

Calculating from incremental market cap: in the mobile internet era, American startups only took 8% of the cake — 92% went to major companies. This was the major companies' victory. Chinese startups — like ByteDance, Pinduoduo, Meituan, Xiaohongshu — took 40%. This was the startups' victory. We can believe the AI cake will be 10× or larger than Mobile. Is it possible for startups to take 10-40% of it?

When PC and internet were first invented, Americans began the IT Great Voyage — people worldwide used Windows and Google. Today it becomes the Chinese Great Voyage: Chinese entrepreneurs face overseas from day one. In this transformation, Chinese will carry substantial weight.

The 2025 World Weekly cover was the image below: "Who Builds America" — the 8 most influential leaders in AI, 3 of them Chinese. I was thrilled seeing this. I can imagine that in 10-20 years, this peak photo should have at least 30 people who built great enterprises in this AI transformation, creating products used by hundreds of millions — at least half of them Chinese.

Some of these 30 people should already be in the arena today, still doing "Brownian motion" searching for direction everywhere. As an investor, the purest joy is meeting them when they're unknown, investing in them, accompanying them, participating in part of the story.

Heart Capital was founded in 2022 as an early-stage Chinese venture capital fund focused on technology and digitalization. The Heart Capital team is primarily composed of Yan Han, founding partner of Lightspeed China, core investors, a chief financial officer, and senior investors from industry. The team's past investments include Series A investments in Xpeng Motors (NYSE: XPEV, 09868.HK) and Full Truck Alliance (NYSE: YMM), Pre-Series A investment in MetaX (688802.SH), as well as RoboSense (02498.HK), FinVolution (NYSE: FINV), LandSpace, Micro-nano Starry Sky, Huitian, Xi Wang, Polestones, Sunmi, World Logistics, Baichuan, Manbang Cold Chain, Fan Deng Reading, Lanhu, Starfield, and others. Rooted in China with a global vision, Heart Capital is committed to finding true value in non-consensus. Heart Capital respects the value of "people" and advocates the potential of "heart," looking forward to accompanying more young Chinese entrepreneurs to strengthen China and go global.