Heart Capital's Yanchen Liu | When Energy Stands at the Edge of Its Next Leap: Controlled Nuclear Fusion Through a VC Lens | VOICE

"The ultimate energy source" is moving from science fiction to engineering reality.

At a time when AI, aerospace, and manufacturing are all moving toward energy-intensive models, human civilization is reaching a new inflection point. Traditional energy systems are approaching their limits, while the "ultimate energy" — controlled nuclear fusion — is advancing from science fiction toward engineering reality.

| Heart Capital, Yanchen Liu

| 5,000 words total, estimated reading time 8–10 minutes

Over the past three centuries, every major technological leap in human history has been accompanied by a shift in energy systems: the steam engine ushered civilization into the industrial age, electrification drove urban expansion, the petroleum system shaped modern transportation, and solar and wind power opened the renewable energy wave. But as we enter the AI era, energy demand is rising rapidly. "Controlled nuclear fusion," hailed as the ultimate energy source, is a term that once existed only in sci-fi films and laboratories — now it's re-entering the public consciousness.

What is controlled nuclear fusion?

Controlled nuclear fusion means building an artificial "mini sun" on Earth. The sun's energy comes from hydrogen atoms fusing into helium atoms under extreme temperature and pressure, releasing enormous energy in the process.

The essence of fusion is getting two light atomic nuclei close enough to merge. However, two positively charged nuclei naturally repel each other, so to get them "close," extreme conditions must be created: temperatures exceeding 100 million degrees Celsius, extremely high particle density, and sufficiently long confinement time — the product of these three is called the "fusion triple product." When this exceeds a certain critical value, the fusion reaction produces net energy gain, i.e., Q>1. For deuterium-tritium fusion, for example, the fusion triple product needs to exceed 3×10²¹ keV·s/m³.

To use a simple "furnace" analogy: to get two positively charged nuclei to "willingly approach" each other on Earth, they must be placed in an extremely high-temperature "furnace," where "plasma" collides and undergoes fusion.

The difficulty of this furnace is on an entirely different order of magnitude from steelmaking. Different fuels require vastly different "ignition temperatures":

- Deuterium–tritium (D-T) furnace: at least 100 million degrees

- Deuterium–deuterium (D-D): even higher, hundreds of millions of degrees

- Deuterium–helium-3 (D-He3): even higher, hundreds of millions of degrees

- Hydrogen–boron (p–B11): no neutron irradiation, but requires 3 billion degrees

This is beyond what any material on Earth can withstand, so magnetic fields must be used to confine the plasma — imagine the plasma being "bound" by invisible magnetic forces within the furnace.

And why is controlled nuclear fusion called the "ultimate energy"?

First, fusion has extremely high energy density. The deuterium extracted from one liter of seawater, no bigger than a fingernail, can release energy equivalent to several hundred liters of gasoline. Converting global annual electricity demand into fusion fuel would require only dozens of tons of deuterium and tritium — practically "infinite" in human energy terms.

Second, fusion is inherently safe. Unlike fission, fusion reactions cannot sustain themselves; once external energy or fuel supply is interrupted, the reaction stops immediately. Therefore, there is no core meltdown and no runaway chain reaction.

Third, fusion produces almost no difficult-to-manage nuclear waste. Emitted neutrons have short lifespans and do not leave behind high-risk long-term radioactive materials.

How? Three main fusion pathways

The key to controlled nuclear fusion lies in plasma confinement. Magnetic confinement, inertial confinement, and magneto-inertial confinement are the three core confinement technology routes:

1) Magnetic confinement: Uses strong magnetic fields to form an "invisible cage," isolating high-temperature plasma from container walls and maintaining plasma confinement, such as tokamaks and stellarators. These devices are suitable for high-power fusion installations.

2) Inertial confinement: Uses lasers/ion beams to instantaneously bombard fuel pellets, utilizing the fuel's own inertia to achieve millisecond-scale compression and heating (such as the U.S. NIF facility). Characterized by compact structure but difficult steady-state operation.

3) Magneto-inertial confinement is a compromise solution, using magnetic fields to assist confinement while combining with the instantaneous high pressure of inertial compression, balancing structural simplification with confinement efficiency and reducing device cost. This is the route that has attracted the most startup attention in recent years.

What? Mainstream fusion devices

Corresponding to the three confinement methods above, here's a brief introduction to the main device types on the market — think of different devices as different-shaped "furnaces."

1. Tokamak

The tokamak is the magnetic confinement device with the longest global research history. These installations are typically massive, like a "doughnut-shaped furnace." The tokamak essentially uses toroidal magnetic fields to make plasma run at high speed in a toroidal chamber. The magnetic fields in a tokamak act like steel reinforcement, building the "skeleton" of the doughnut, binding the plasma like cement firmly to the rebar. The spherical tokamak is a variant structure of the tokamak.

Advantages of tokamaks: long research history, rich data accumulation, and potential for continuous steady-state operation. But they are also among the highest-cost, most engineering-complex routes, with very long construction cycles, generally requiring investments above tens of billions of RMB. For historical reasons, most national teams have chosen the tokamak route. However, several major scientific problems remain to be solved through engineering experiments, such as plasma disruption prevention, tritium self-sufficiency, and first-wall materials.

Because tokamaks are so complex and costly, ITER (International Thermonuclear Experimental Reactor), jointly initiated by China, the United States, Russia, the European Union, and three other parties, is currently the largest tokamak device under construction globally. Its core goal is to verify the engineering feasibility of controlled nuclear fusion, with total investment exceeding €20 billion and a construction cycle of 30 years (construction began in 2008; after a 9-year delay, the latest plan is to complete experiments by 2035).

On the private company side, CFS in the United States is a leading company in high-temperature superconducting compact tokamaks, and Tokamak Energy in the UK is a typical spherical tokamak company.

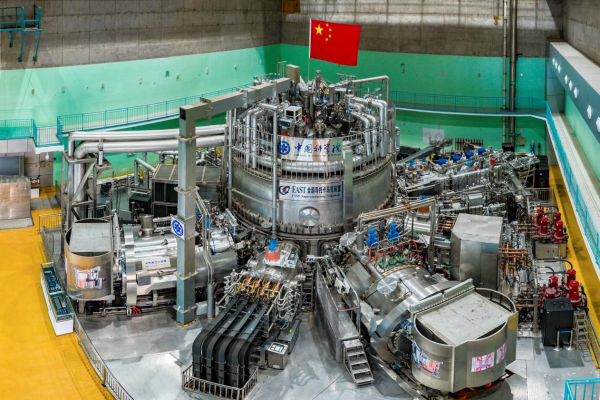

In China, the HL-3 device at the Southwestern Institute of Physics (CNNC), the EAST device at the Institute of Plasma Physics, Chinese Academy of Sciences, and BEST, launched this year, are all tokamak devices. Among private companies, Energy Singularity belongs to the high-temperature superconducting compact tokamak category, while China's ENN Fusion and Star Ring Fusion focus on the spherical tokamak route.

EAST, the world's first fully superconducting tokamak device

2. Stellarator

The stellarator is a toroidal structure with three-dimensionally twisted coils, somewhat like a "twisted dough twist," with advantages over tokamaks in plasma steady-state operation. The downside is complex structure, extreme engineering difficulty, and considerable cost.

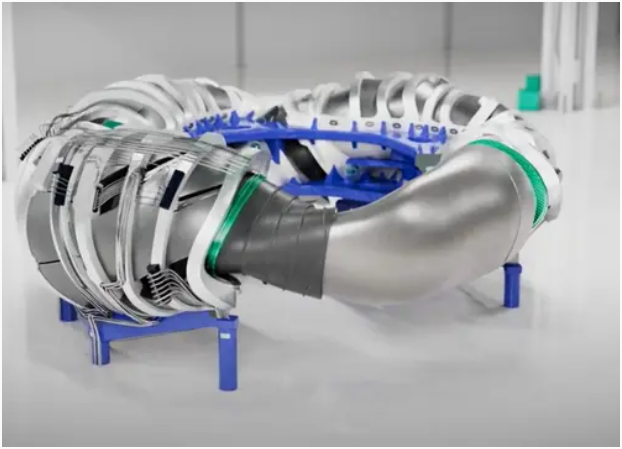

Type One Energy in the United States and Proxima Fusion in Germany are relatively leading stellarator fusion companies. China's first quasi-axisymmetric stellarator was built by Southwest Jiaotong University.

Proxima Fusion's publicly released commercial-scale stellarator design

3. Laser Fusion

Laser fusion compresses fuel spheres to extremely high density in extremely short time through lasers or particle beams, triggering fusion. Imagine instantly igniting a fuel sphere with super-intense lasers, compressing the sphere to extremes before releasing energy. But all of this happens transiently, not through continuous ignition.

The advantage of laser fusion is its ability to instantaneously simulate stellar cores. But the problems are laser efficiency, repeated ignition capability, and device lifespan — all engineering thresholds that need to be overcome.

The most famous is the U.S. National Ignition Facility (NIF), which achieved Q=1.5 in its 2022 experiments, realizing net energy output in a laboratory for the first time. Typical startups include Xcimer Energy and Longview Fusion in the United States.

U.S. National Ignition Facility (NIF)

4. FRC Field-Reversed Configuration

FRC (Field-Reversed Configuration) is a linear magnetic confinement device. Its core principle: the magnetic field generated by the plasma itself is opposite to the external magnetic field, forming a closed toroidal magnetic field that confines high-temperature plasma like a "magnetic cage."

Imagine this linear device as two "barrels" connected together, with the center being the "firebox." The fusion reaction ignites two plasma masses simultaneously at both ends, accelerating these two "flames" to extremely high speeds through magnetic fields, colliding them in the central "firebox." The pressure and density at collision are extremely high, with rapid magnetic compression pushing temperatures above 100 million degrees Celsius, triggering fusion.

Compared with traditional "furnaces" (such as tokamaks), FRC has simpler structure, faster iteration, and costs only 1/5 to 1/10 of a tokamak, making it promising as the first fusion technology to achieve commercialization. It is also a technical route that has attracted considerable VC attention both domestically and internationally.

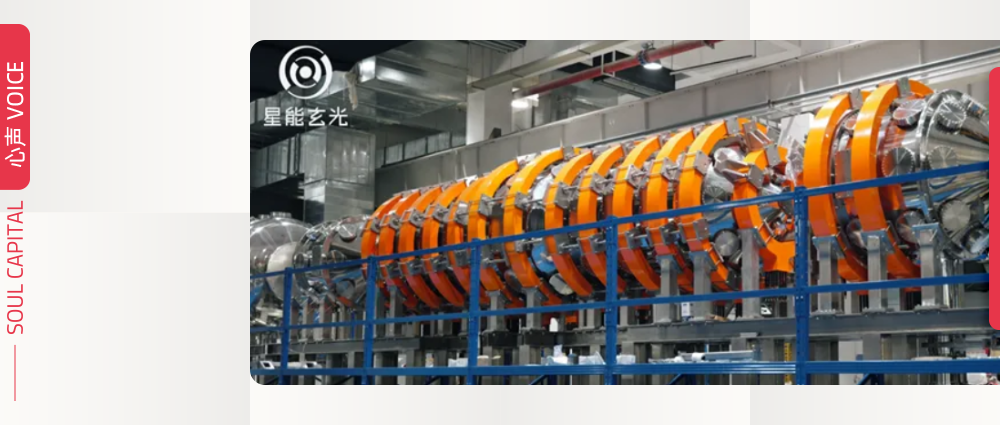

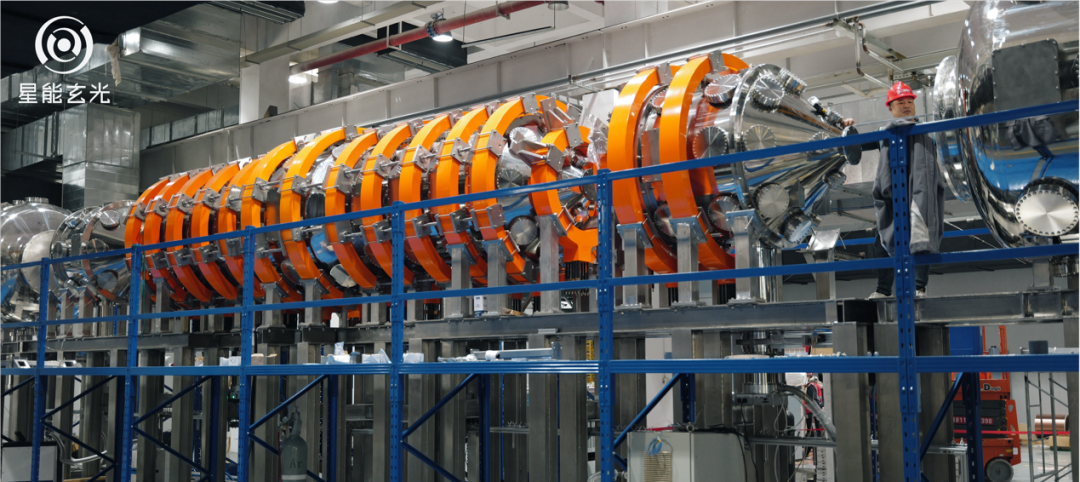

Leading international companies on the FRC route include TAE and Helion Energy in the United States. In China, Star Energy X-Photon — which we invested in — is a leading FRC company. Its team has over a decade of R&D and engineering experience with linear devices (linear devices include magnetic mirrors, FRC, etc.).

Star Energy X-Photon linear device

When? Fusion commercialization timeline

For a long time, "always 50 years away" has been a refrain repeatedly joked about in fusion circles. Our observation is that 2021 seems to have been an important milestone for the fusion industry. After 2021, capital attitudes began to change noticeably. Behind this are three main driving factors:

First, breakthroughs in key engineering variables. The most typical example is Commonwealth Fusion Systems (CFS) announcing in 2021 the successful testing of its "20T high-temperature superconducting magnet," a technology that can dramatically reduce the volume and cost of superconducting magnets required for fusion devices, reportedly shrinking tokamak device volume and cost by 40 times. This breakthrough is widely seen as the threshold where fusion shifts from a "scientific problem" to an "engineering problem."

Second, significant parameter progress by startups, giving the market hope. For example, Helion Energy announced achieving plasma temperatures exceeding 100 million degrees Celsius in its sixth-generation Trenta device, while Helion signed a power delivery agreement with Microsoft for 2028. Another leading FRC company, TAE, achieved field-reversed configuration directly through neutral beam injection in its Norman device, and recently announced its decision to skip the sixth-generation prototype Copernicus and directly commence construction of its first commercial demonstration fusion plant Da Vinci, substantially shortening its commercialization timeline with expected commercial fusion energy delivery in the early 2030s.

Third, dramatically enhanced market demand for electricity. AI, data centers, computing expansion, satellite internet, and carbon neutrality goals mean energy demand will grow exponentially in coming decades. This means the energy technology revolution is driven not merely by laboratory technology, but by "hard industrial demand."

On the government side, after 2021, countries have increased fusion investment. The U.S. Department of Energy (DOE), the UK, Japan, China's fusion planning, and leading global companies have successively announced roadmaps, causing timelines to converge for the first time.

2025–2030: Engineering verification period The core of this stage is achieving "Q>1" — where energy output exceeds input. China's BEST plan aims to light the first bulb through fusion power generation by 2030.

2030–2040: Early commercialization Globally, 10–50 megawatt-class small fusion power generation units are expected to emerge, with equipment gradually moving from scientific experiments to energy facilities. Multiple countries' roadmaps currently view this phase as the "critical window for fusion grid connection."

Post-2040: Scaled expansion With cost reductions, modular solutions emerging, and equipment standardization, the fusion industry could enter a growth phase similar to photovoltaics.

Therefore, as fusion moves from "scientific verification" into the "engineering construction" phase, it acquires the foundation to be invested in and industrialized.

China's controlled nuclear fusion industry landscape

Compared with the United States, where private companies and universities drive development, China's fusion ecosystem is a strategically prioritized track dominated by national teams. The state has incorporated fusion into one of the "six major future frontier industries" in its 15th Five-Year Plan, giving it clear strategic positioning. Provincial and municipal governments have successively participated in layout, with resources tilting toward fusion — for example, Shanghai and Hefei have clearly stated their intention to build fusion industry centers.

China's current controlled nuclear fusion industry is mainly propelled by three types of forces. The first is the central state-owned enterprise system, with resource and scale advantages. The second is local state-owned asset-supported enterprises, emphasizing industry-city integration and industrial layout. The third is private innovative companies, characterized by technical flexibility, light structure, and fast iteration.

We believe these three forces do not replace one another, but form a complete ecosystem: a combination of scientific exploration, engineering realization, and commercial innovation, similar to the multi-layer structure China has formed in aerospace and semiconductors. This means state-owned enterprises undertake large-scale demonstration reactor projects, while private teams present a multi-route exploration pattern, complementing the national teams.

For example, besides China Fusion Energy Corporation undertaking large-scale demonstration engineering, local state-owned assets such as Fusion New Energy actively promote BEST construction; while private enterprises such as Star Energy X-Photon and Star Ring Fusion each carry out engineering exploration based on different routes. Meanwhile, startups focusing on Z-pinch, stellarators, laser fusion, and others are being established successively.

In terms of talent, China has research institutions including the Institute of Plasma Physics, Chinese Academy of Sciences, the Southwestern Institute of Physics (CNNC), University of Science and Technology of China, Huazhong University of Science and Technology, Tsinghua University Institute of Nuclear and New Energy Technology, and Shanghai Jiao Tong University, gathering a cohort of young backbone talent with "research + engineering" capabilities. Meanwhile, on the industry chain side, from superconducting tapes, high-field magnets, vacuum systems, and diagnostic equipment, to future reactor construction and operation-maintenance systems, the overall ecosystem is accelerating.

Therefore, we are pleased to see that China possesses several key elements: "government leadership," "research talent," "industry chain," and "capital support." Now is the optimal timing for VC investment.

VC "First Principles" for Evaluating Fusion Companies

Controlled nuclear fusion is a technology-intensive industry, but for VCs, the true investment value lies not in debating the merits of technical details, but in penetrating the fog and anchoring to three underlying judgment principles:

First, route selection: Focus on "private capital adaptability." Current fusion technology routes are blooming everywhere — tokamaks, stellarators, linear devices all have commercialization potential. We do not prejudge a "sole successful path," but rather focus on "paths that private capital can efficiently advance at this stage" — with three core criteria: input cost, iteration pace, and commercialization potential. For example, tokamaks require investments above tens of billions, more suitable for national team breakthroughs; while linear devices (such as FRC), with their low cost and fast iteration characteristics, are more suitable for distributed generation scenarios such as AI data centers, remote mountainous areas, or island power supply, becoming one of the most suitable paths for private capital entry.

Second, team strength: Bet on "formed, hardcore teams." Fusion entrepreneurship is never a "single-point breakthrough" by an individual scientist, but requires "veteran teams" with experience in complex devices — must assemble experts in physical theory, numerical simulation, diagnostic technology, and engineering implementation, forming composite teams of "scientists + engineers + doers," who understand underlying physics, can handle engineering implementation, and have a foundation of long-term collaborative磨合. Entrepreneurship is a long-term process; team cohesion and stability are paramount. At the same time, we believe that breakthroughs in plasma physics and industry chain maturation will benefit all fusion routes, so the ability to iterate technologically is also a core test of team strength.

Third, capital capability: Test "sustained financing ability." The long-cycle nature of fusion projects requires teams to have not only engineering hard power, but also capital soft power — whether they have compelling narrative ability, a roadmap that can be implemented and that lets investors understand the commercialization path, and the ability to bind government and industry partners to form strong backing behind them — importance no less than technology R&D itself.

Based on the above logic, Heart Capital chose to invest in Star Energy X-Photon: first, the linear FRC route's advantages in compactness and miniaturization better fit the "low-cost iteration" advancement logic of the AI era, comparable to SpaceX's successful path; second, the team originates from University of Science and Technology of China, a formed team whose R&D pace and cost control meet sustainable iteration requirements, and is currently the fastest-developing linear fusion company in China; third, having completed two consecutive funding rounds gaining recognition from industry players and market-based capital, it has already validated its financing and resource integration capabilities.

Fusion is advancing from science fiction toward engineering — the future is worth anticipating

Looking back over the past three years, the development speed of controlled nuclear fusion has exceeded most people's imagination.

From the VC perspective, controlled nuclear fusion is not a technology bet, but an engineering, industrialization, and commercialization opportunity. When an industry shifts from "scientific problem" to "engineering problem," the true window period often arrives accordingly. In this window period, we hope to practice our long-termism perspective, through forward-looking vision, in-depth research, and pragmatic judgment, to participate in this energy revolution.

We believe that with the combined force of policy guidance, talent influx, and capital support, controlled nuclear fusion power generation will ultimately be achieved.

Let us together witness humanity's next leap forward at the energy level.

Founded in 2022, Heart Capital is an early-stage venture capital fund focused on technology and digitalization in China. Heart Capital's team is mainly composed of Yan Han, founding partner of Lightspeed, core investors, the chief financial officer, and senior investors from industry. The team's past investment cases include Series A investments in Xpeng Motors (NYSE: XPEV, 09868.HK), Full Truck Alliance (NYSE: YMM), as well as FinVolution (NYSE: FINV), RoboSense (02498.HK), Baichuan, Manbang Cold Chain, Fan Deng Reading, World Logistics, Micro-nano Star, LandSpace, Lanhu, Starfield, and others. Rooted in China with a global perspective, Heart Capital is committed to finding true value in non-consensus. Heart Capital respects the value of "people" and advocates the potential of "heart," looking forward to accompanying more young Chinese entrepreneurs to strengthen China and go global.