Floodgate founding partner Mike Maples' year-opening podcast: How to invest in the next 100x startup

Every great startup exists to build a future that is destined to arrive.

Z Talk is ZhenFund's column for sharing ideas and perspectives.

Mike Maples is an entrepreneur and venture capitalist, and the founding partner of the renowned VC firm Floodgate. He has been named to the Forbes Midas List eight times and is widely recognized as one of the pioneers of the seed investing movement in the mid-2000s. His investments include Twitter, Twitch.tv, Clover Health, Okta, Outreach, and Chegg.

In 2024, Maples published Pattern Breakers, a bestselling book sharing its title with his personal tech podcast. The book uses "inflection theory" as its core framework to examine the pivotal transformations of well-known startups like Slack, Pinterest, and YouTube. He argues that seizing inflection points is the decisive factor in a startup's success. The only way to challenge industry giants, he believes, is to rewrite the rules.

In his first interview of 2025, drawing on Floodgate's experience running a $150 million seed fund, Maples shared his investment logic: the core of investing lies in whether a founder possesses "future fitness"—the ability to stand on a non-consensus but correct position and bring about an inevitable future as quickly as possible.

From ZhenFund's earliest days, Mike Maples has been a Silicon Valley early-stage investor we've held in deep respect. Pattern Breakers was also the 2024 book recommendation from Anna, ZhenFund's founding partner and CEO. Like Maples, ZhenFund has always been on the lookout for outliers—those who dare to break patterns, step outside established frameworks, and redefine the world through unconventional lenses.

This content comes from the 20VC podcast. Below is the full translated interview.

Key Takeaways

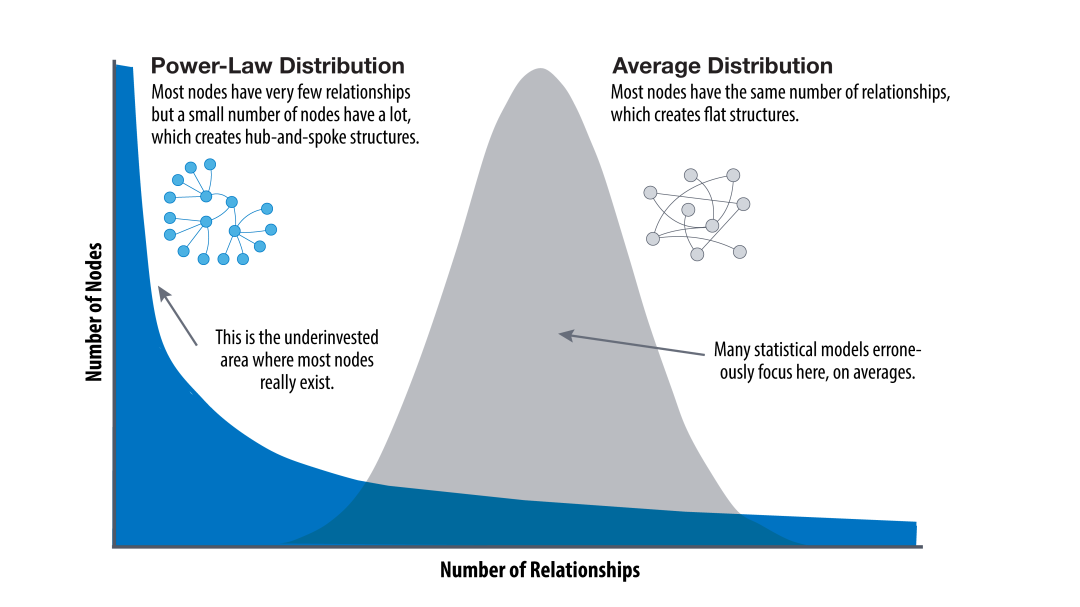

- Fund size dictates investment strategy: Fund size is like setting the bar height in pole vaulting. According to power law and the 80/20 rule, top-performing projects typically determine overall returns. Therefore, seed funds must align size with team execution capability and formulate a clear investment strategy.

- Pro-Rata Rights: The first check in a seed round is active offense with capital; pro-rata rights are the exclusive advantage of seed investors. Performance at the Series A stage is a critical benchmark for deciding whether to follow on.

- Three Criteria for Evaluating Founders: Exceptional founders need three core capabilities: capturing inflection points, taking a non-consensus but correct position, and high future fitness. Understanding of the future matters more than business experience.

- The Cyclical Nature of Exit Markets: Venture capital exit cycles occur roughly once every 15 years, with an optimal window of 18 months to 2 years each time. Seizing that window is central to achieving 100x returns.

01

Capturing the Pulse of the Era Going on Offense with Capital at the Seed Stage

Harry Stebbings: This is the first episode of 20VC in 2025. Today we're returning to the core theme of early-stage venture. Mike, I can't believe we're finally recording this face-to-face. Dude, we've known each other for nine years.

Mike Maples: Yeah, I knew you back when nobody was listening to your show.

Harry Stebbings: God, back then the audience was probably just you and my mom. But I want to start with the current seed funding ecosystem. The fundraising environment seems tougher than ever. Do you think seed funds with less than $100 million under management can still exist?

Mike Maples: They can, but they'd need to be well below $100 million, making investments of less than $100,000. For example, looking at your fund, you probably wouldn't let a co-investing angel put in more than $100,000, right?

Harry Stebbings: Absolutely not, no way.

Mike Maples: If someone said, "Hey, I'm an angel investor participating in some $750K rounds. Harry, let's partner up," you'd probably say, "Great, really happy for you, but goodbye." Would you actually work with this person? Probably not.

Harry Stebbings: No, because rather than taking $500K from a smaller fund, you'd rather have five great angels each put in $100K.

Mike Maples: Right. But let's say you're making investments of less than $100K. If Tim Ferriss came to you and said he wanted to put $100K into something that might benefit from his brand and promotion, you'd definitely say yes, right?

If you say, "Hey, I'm making $100K investments," that's fine, but that fund is probably around $10 million, not $100 million.

Harry Stebbings: So why did your fund size go from $70-80 million before to $150 million now?

Mike Maples: For me, fund size is your investment strategy. People always hear me say this, but I've never really explained it. Simply put: the power law is real.

People don't realize that the Pareto Principle isn't just 20% and 80%—it's a continuous curve. 20% of investments generate 80% of returns. 4% of investments generate 64% of returns, because 20% squared is 4%, but 80% squared is 64%.

Say you have 25 companies in your fund. Your best investment needs to account for 64% of all returns, just that one. If you want 5x fund-level returns, that single best investment itself needs to generate 64% of 5x the fund's total value. That's why fund size and investment strategy are deeply intertwined.

Fund size is like the bar height a pole vaulter sets. You're committing to clearing that height. If you can't, the fund doesn't work.

Unlike normal distribution, power law distribution's defining feature is its long tail: output becomes increasingly concentrated among a small number of winners

Harry Stebbings: Have you ever felt your fund size didn't match your investment strategy?

Mike Maples: Honestly, I've never really felt fund size itself was the problem. Weirdly, we performed better with a $150 million fund than with a $75 million one. I don't think it's entirely about fund size. Looking back at our history, our first few funds were absolutely spectacular.

We accurately captured the pulse of the era, hitting the market at exactly the right golden moment. Just this morning I was recording a video for Josh Kopelman's 20th anniversary at First Round, reflecting on our early meetings. Back then we'd constantly wonder: why doesn't anyone realize what a massive business opportunity this is? We'd ask ourselves: "Are we stupid, or are we deluding ourselves?" Because nobody thought these ideas had value, while we believed they were once-in-a-century opportunities.

Every time I discovered something, I'd bring it to Josh, and he'd do the same. Neither of us had money; we just kept seeing all these potential opportunities. After a while, I found myself sitting on 22 boards simultaneously, but my thinking was no longer as sharp as before. When you're fielding endless calls and constantly putting out fires, even if Pinterest came to you, you couldn't see its potential clearly.

Our performance with the $75 million fund was far weaker than our earlier funds. I remember being extremely anxious, so I flew to Yale to see one of our LPs, Dave Swensen of the Yale Endowment. I told him that if I didn't tell him the truth, I'd regret it. So I laid out the mistakes we were making and my ideas for improvement.

One improvement was adjusting fund size to match our execution capability. We made other changes too, like having a partner, Iris Choi, specialize exclusively in follow-on investments, making her responsible for their returns. I think more seed funds should do this.

Harry Stebbings: I don't quite follow this logic. We don't do follow-ons at all, because the data shows we consistently overestimate our ability to pick winners. But as an investor, you have an information asymmetry advantage—you can make better decisions. Why would you give up that edge?

Mike Maples: Indeed, pro-rata rights are a right. Of all my investments, I have two most important principles: first, you need to be compensated for the risk you take; second, you should always be going on offense with your capital.

For a seed fund, the first check is theoretically going on offense with capital. If that's not what you're doing, you're not even in the fight.

Sometimes you find yourself owning pieces of truly exceptional companies—like Applied Intuition, Figma, Twitter, Okta—and you know it's a great company, more excellent investors are coming in, the price will get bid up, but whether you exercise your pro-rata is your choice. Remember, this is a right only you have. To me, this is a classic example of "going on offense with capital."

Harry Stebbings: The thing is, when round pricing is sky-high and your fund is small, exercising that right might cost several million dollars.

Mike Maples: Exactly. I think the first question to answer is: do I abandon follow-on investing entirely? You can choose not to invest, but that means giving up a valuable right. Another way to look at it: this right has value greater than zero. Then the question becomes: how much greater? We ultimately decided to allocate 70% of capital to initial investments and 30% to reserves. And Iris has full control over that 30%. Ann and I can't force her to defend a failing investment.

She'll say: "Maples, I'm responsible for the returns on this portion of capital. You can't make me pay up for a bad investment."

Harry Stebbings: But doesn't that lose a lot of crucial context? I know the founder better than anyone. I know how fast the contract is moving. But none of that shows up in the data, and Iris won't necessarily know.

Mike Maples: Iris is well aware of that. She's part of Floodgate. She gets to know every founder as well as she can, and she treats all of our investments as if they were her own prospective deals. Take Applied Intuition — she even bought additional shares beyond her pro rata, a Super Pro Rata.

She successfully increased her ownership on top of our initial investment. She'd say, "Look, this is the best company in Fund VI. We should own as much of it as possible."

Most seed funds think they know a company better than the market. So even if the company can't raise financing, they're willing to invest. But in those situations, I often say: "I don't think you actually know what you think you know."

I have tremendous respect for the market's ability to identify great Series A companies. If firms like Benchmark, Sequoia, General Catalyst, and a16z all pass on one of our portfolio companies, I think: "Well, nobody's going to have better judgment on this company than that."

But if those firms decide to invest aggressively, that's an extremely strong signal. Because they're not just choosing from companies we invested in — they're selecting from all seed investments. That means they believe this company is among the most promising of all seed-backed startups.

In that case, I'd seriously consider exercising my pro rata. You can't blindly follow Sequoia or Benchmark. But if they think this is one of the best opportunities in the market right now, the value of that right is obvious.

Harry Stebbings: Don't you think you should just follow what the top firms invest in?

Mike Maples: Not exactly, but you're not wrong. Look at our first fund — what performed best? Demandforce. Who followed us? Bill Gurley at Benchmark. What was second best? Twitch. Who followed Twitch? Ethan Kurzweil at Bessemer.

Second fund — what performed best? Lyft. Who followed us? Navin Chaddha at Mayfield Fund, Founders Fund, and a16z. Second biggest winner? Okta. We invested alongside a16z, then Sequoia and Greylock followed.

One way to think about it: your follow-on investments can be viewed as a subset filtered from the best firms' portfolios. Of course there are exceptions — Sequoia was aggressive on VarageSale, and that didn't work out.

For seed funds, follow-on investing is a bit like index investing. If you just follow the best firms, you'll typically generate far better follow-on returns than most people. Most LPs, if they really looked at the return differential between follow-ons and initial investments, would probably revolt — the gap is that large.

Harry Stebbings: Do you buy into the idea that every investment needs to return the fund?

Mike Maples: Our seed business is hard but not complicated. Five percent of investments need to return 100x in cash. Ten to fifteen percent need to return 20x. Hit those targets, and your fund returns 10x.

From a 3x fund to a 10x fund, the loss ratio is about the same. What matters is the magnitude of the big winners. This brings us back to the Pareto principle. If your best company returns 64% of the fund, then follow-on investments in that company will likely return another 20x.

Harry Stebbings: The problem with that assumption is that it assumes you can predict outcomes, but it's actually very hard to know which companies will become the big winners.

Mike Maples: You certainly can't predict it, but we hold ourselves accountable. Ann and I are measured by what we call "stock picking" — what percentage of our initial investments become 20x or 100x outcomes. Iris is measured by what percentage of her follow-on investments hit the best companies. It's completely objective.

You can rank companies by their current valuations and look at what percentage of our capital is in those top companies. That metric has a huge impact on our returns.

Harry Stebbings: Do you do outcome scenario planning when you invest? Like, how does this become a $5 billion company, and work backwards from there?

Mike Maples: No. I think: what would it take to return 100x on the initial investment?

My scenario planning for initial investments goes like this: given there's an 85% probability it won't be in the top 15%, if it is in the top 15%, how big does it need to be? Is that possible? What does the world where it succeeds look like?

A lot of the debate around valuation, I think, is wrong. People say: "If the company is good enough, you can pay any price." That's true to some extent, but only if you can return 100x on your initial investment. That's the more important logic. If we invest $1 to $2 million, can we return 100x? Take Applied Intuition — their Series B was $40 million, and they just raised at a $6 billion valuation.

Harry Stebbings: The problem with that is it assumes the company eventually becomes a $5 billion company. But there are embedded assumptions — dilution could be massive, half or more. If so, the company ultimately has to be worth $5 billion.

Mike Maples: So we do that math, but that's also why price matters, right?

Harry Stebbings: Our entry price is $25.

Mike Maples: If that's your entry price, then the exit price has to be at a corresponding level. That's unavoidable. Some people say, "That was then, this is now." But that's not true. I've studied venture capital return patterns over the past 50 years. The fundamental mechanics of what makes great funds great haven't changed.

Be Greedy When Others Are Fearful, and Fearful When Others Are Greedy

Harry Stebbings: Do you think venture capital is a less attractive asset class?

Mike Maples: I don't think so. It's just that many people have forgotten what the right target is. I tell myself I need to return 100x on my first check. That's achievable if everything goes right, but I can't get there by acting like an efficient market operator. Seed investing that focuses solely on efficiency is no longer a good business. To make money, you have to find inefficiency in the market.

If someone asks me, "What if you can't find inefficiency?" My answer is: "Then you shouldn't be doing seed investing." As an active investor, you need to find inefficiency in the market. Otherwise you're not suited for this business.

Harry Stebbings: I completely respect that, but you're in the center of San Francisco. This is the heart of the seed market. It's the most efficient market there is. When you and Josh started, there was massive inefficiency in the market. But neither of us is in an inefficient place now.

Mike Maples: The mistake people make is thinking of startups as some kind of "market." Compared to when Josh and I started, more companies are now priced efficiently. But to me, that's the fun, that's the romance of venture — finding what others don't see, or at least trying to, and occasionally getting into deals others can't. It's like solving a puzzle or a riddle. There are so many startups. Every year, roughly 30 great companies emerge.

Harry Stebbings: If you think a company could return 100x, are you willing to invest a smaller amount?

Mike Maples: Yes. But the investment has to meaningfully move the needle on fund returns. The minimum I can accept is $500,000.

Harry Stebbings: Have you missed great companies because of this strategy?

Mike Maples: That's a good question. Looking back, I don't think I've ever missed one for that reason.

Harry Stebbings: That's been our biggest miss. Looking back, we could have invested in ElevenLabs. It's a $3 billion company now, probably the best startup in Europe right now.

Mike Maples: Yes, you could have gotten in with $250,000 at the time. If you had invested, would that company return 100x?

Harry Stebbings: It's at 150x now. We should have done it. We could have even just put in $250,000.

Mike Maples: There will always be cases like that. Our business is hard but not complicated. There's a 5% chance of 100x on the first check. To achieve that, you need to select opportunities with sufficient potential scale, while being mindful of price.

Harry Stebbings: How do you think about inception rounds? A lot of initial checks are now $10 million, even higher in AI.

Mike Maples: Can that return 100x on the first check?

Harry Stebbings: If it meets that condition, would you participate in such a round?

Mike Maples: If I think there's a chance of 100x, I'll participate. If it's a Qasar Younis deal, I'll invest. Sometimes younger colleagues come to me and say, "This is a $10 million round at a $40 million post-money valuation — similar to what we did with Applied Intuition." I ask: "Okay, is the founder Qasar Younis?"

Qasar is one of the best founders I've ever worked with. If the founder doesn't have that same capability, the valuation isn't worth it. This company has to reach at least a $5 billion-plus valuation to justify the investment.

Going further, if I think the return won't reach 100x but only 20x, even with an exceptional founder, I probably won't invest. Because there's an opportunity cost. My fund only has 40 investment slots. If I miss one, that's one less chance at a potential 100x return.

Harry Stebbings: Do you think everything is getting harder?

Mike Maples: Of course, but we're also getting stronger and smarter. Competition is fiercer now, and certain traits help you stand out that weren't as important in the past. Today, being nice has actually become a major advantage.

Harry Stebbings: What do you mean by being nice?

Mike Maples: Back in 2021, we saw many projects raising at $30 million, $35 million, even $40 million valuations. Ann and I looked at each other and thought: we don't have to do this.

Some younger investors might complain: "We haven't done any deals this year." I'd say: "That's fine, we just haven't found anything that meets our standards." Ann and I have been in this business long enough. We have nothing to prove to each other, and no metrics to hit this month, this quarter, or even this year. Silicon Valley will create more opportunities, and we'll be there for them.

I've spent a lot of time with Ann thinking about what we're good at, analyzing our past successes, and figuring out what opportunities will emerge in the future. We have to see deals that meet our criteria. We'd rather miss out than arbitrarily lower our standards.

Harry Stebbings: Do you agree with Gurley's view that you have to be in the game no matter what the field looks like?

Mike Maples: You have to be in the game on the field you're currently on.

Harry Stebbings: But what if that "field" doesn't match your conditions?

Mike Maples: If conditions on the field aren't ideal, you need to be more discriminating. Buffett once said something classic: investing is like a baseball game with no "called strikes." So you can let pitch after pitch go by without swinging.

When everyone else is yelling "Swing, you bum!" you can stick to your own rhythm: no need to swing, because you haven't seen the right opportunity. Wait for that perfect pitch, then swing with everything you've got.

If the ideal pitch never comes, just keep waiting — someday it will. This mindset is perfectly suited to the pace of investing. In 2009, for example, when everyone else was pulling back, Ann and I saw numerous projects that fully met our investment criteria.

Ann invested in Lyft at a $5.5 million valuation, putting in $750,000. That investment returned roughly 250x. The environment at the time was that nobody dared to invest; people thought the world was about to collapse. But we firmly believed that as long as a project met our standards, we would act regardless of market conditions.

Similarly, in 2021, I made only one investment all year, in a company called Hadrian. Why? Because I couldn't find anything else that met my criteria.

One important concept I learned from Buffett and Munger about the "Circle of Competence" is this: if you know the boundaries of your circle, when everything in the market is overvalued, you'll do fewer deals because fewer things meet your criteria; when everything is undervalued, you'll do more. That's the rhythm you want.

Harry Stebbings: What about when the rules on the field become an entirely new game? Like AI right now — prices are crazy, market enthusiasm isn't dying down. But if AI really is the next disruptive technology, as everyone says, this is the most exciting moment in 30, 40, even 50 years. Salesforce founder Marc Benioff even said this is the most exciting period of his career — so shouldn't you be in this game?

Mike Maples: You have to be in the game on the field, but you don't have to play it the way everyone else is playing it. Ultimately, if you can't find inefficiencies in the game, you should ask yourself: what am I doing? What's the goal?

Our job is to find opportunities where we can make money. Nobody's interested in investing in a broadly overvalued early-stage market — that's not a good business. You have to look for attractive opportunities. In AI, we've focused on enterprise-related companies, like Applied Intuition. A more recent one is Cicero, which is more focused on legal tech. But we've set very clear conditions for our AI investments — what we'll invest in and what we won't.

Harry Stebbings: Are these projects priced crazily?

Mike Maples: No. Applied was expensive, sure — it was at a $40 million post-money valuation.

Harry Stebbings: Are your most successful investments always your most expensive ones?

Mike Maples: Quite the opposite — usually the lower-priced ones perform better. Though I'm not sure that will always hold true.

Harry Stebbings: But these projects are very competitive, right?

Mike Maples: Applied definitely was. Qasar Younis could have raised from virtually any firm he approached. His capability, ideas, and preparation were exceptional. He only talked to two firms, got two term sheets, and ultimately chose to work with Mark, who joined the board.

At that point, I judged that the risk in Applied's Series B had decreased considerably, so I decided to participate in that round as much as possible. The moment our capital came in, Iris tried to buy even more shares.

Harry Stebbings: Have you ever participated in a project investment through common stock rather than preferred stock?

Mike Maples: There have been situations. Sometimes a founder wants to work with me and I'm willing, but the price is too high.

That's one benefit of convertible notes — I can tell the founder, you can issue a convertible note at any price. Say you're raising at a $20 million valuation; you can do half at $20 million and half at $5 million. They might say other investors don't want that arrangement. I'll say I understand, but it's your call whether you want me in or not. Through this approach, you quickly find out whether they truly value your participation.

Harry Stebbings: Regarding common stock investments, we previously interviewed Nicholas Chirls from Notation. He mentioned that to align with founders' goals, investors should buy common stock. I like Nick a lot, but I think he's talking nonsense. What do you think?

Mike Maples: If it meaningfully increases my ownership stake early on, I'd consider it.

Harry Stebbings: Is this a make-or-break difference in getting a deal done?

Mike Maples: It's actually not that complicated. I might say to a founder: "Hey, we can try to find a way where we both win. I know you need a price that meets your expectations, and you have your reasons, but maybe we can agree through a hybrid approach." For instance, I buy some preferred plus some common stock, so I hold more shares while also taking more risk. But if I believe in the company, that's not the key factor — I've never made or lost money in a successful deal because it was common versus preferred stock.

Harry Stebbings: Would you accept uncapped convertible notes?

Mike Maples: Very rarely, like with Applied, where after the Series A we wanted to hold more shares. If you have strong conviction in a company, you're willing to pay a discount on the future price without fixating on the exact number. Otherwise, why would a founder give you any preferential treatment in the next round? If you're bullish on the company, you have to position yourself for the next financing.

Harry Stebbings: Have you ever done anything like Chris Sacca's "sweeping" — what I call "sweeping," buying early shares from Twitter employees?

Mike Maples: Never. There was definitely temptation, but I ultimately didn't do it.

Harry Stebbings: You mentioned Ann's exceptional investment in Lyft — $750,000 for a 250x return. If you sold shares now, it wouldn't be a 250x return. How do you judge when is the optimal time to sell?

Mike Maples: This operates on several levels. Incidentally, this is an advantage of seed funds we haven't discussed yet. Say it's 2015, Lyft is trading around $25 per share in private markets, significantly higher than today. At the time we said: "We need to sell some of our position." Our investment sat behind a $1.5 billion preferred stock layer; we got in at a $5.5 million valuation. Our competitor was Uber's Travis Kalanick, whom I respect — he was genuinely formidable. This would directly impact our fund performance.

Ann put a sticky note on her monitor that said "IQ Test." She wrote it in January of that year, meaning she had to find a way to sell some Lyft stock. She ultimately did sell quite a bit, though less than half.

Harry Stebbings: What was the price at that time?

Mike Maples: $25 per share, roughly a $4 to $5 billion valuation. It was a good price. The peak was roughly in that range.

Harry Stebbings: That must have returned the entire fund principal, right?

Mike Maples: Exactly. We decided then to sell enough shares to ensure the entire fund's capital was returned. Ann pulled it off. Many seed funds don't realize there are two ways to make money: one is exploiting inefficiencies in entry pricing, the other is exploiting inefficiencies in exit pricing.

In Lyft's case, a16z was also invested, but they couldn't pursue this strategy. The reason: their selling shares would send a negative signal, and a few hundred million dollars would be a drop in the bucket for a16z's fund.

Seed funds can exploit this. The key consideration is whether the market is pricing the company on a perfect-execution assumption, leading to overvaluation?

Harry Stebbings: Do you think there are also exit pricing inefficiencies in the current AI boom?

Mike Maples: Exactly. Usually when you sell in certain rounds, every investor wants a piece of that company. What I've learned is that it's actually a win-win for the founder. You can't trade on a whim. But you can say to the founder: "Let's be realistic — in the long run, you're better off with an investor like Fidelity in your cap table than a seed fund."

We'd develop the strategy together. At first the founder might hesitate, but by the time the financing is about to close, they'll come to you and say: "Please, you promised to sell some of your position, you need to sell more. Because everyone's fighting to get in."

When everyone is rushing to buy, seed funds should actually be thinking about exiting. Iris even named this strategy the "Initial Liquidity Event" — meaning it has the same impact on fund economics as an IPO, not a small $10 or $15 million exit, but a liquidity event large enough to meaningfully move the needle on overall fund performance.

Harry Stebbings: Brian Singerman has mentioned to me many times the value of "the next double." He believes it's much easier — and much faster — to get a company from $2 billion to $6 billion in valuation than to add $4 billion of value across the rest of your portfolio. For example, Bessemer sold their Shopify position early, at roughly $2 to $3 per share. That was probably their worst financial decision.

Mike Maples: Every trade comes with some regret.

Harry Stebbings: But your move on Lyft was a massive success.

Mike Maples: Yes, though Lyft traded up to around $75 post-IPO, and we sold near $75. If we'd waited longer, we might have made more, but from a risk-adjusted perspective, it was still the right decision. When your fund is already in the carry zone and doing well, even though there's still upside potential, your psychology shifts.

Harry Stebbings: Does your psychology change when you're "in the carry"?

Mike Maples: More or less. In some cases the volatility of potential outcomes is simply too extreme. I agree with one of Brian Singerman's points: Some investments do go much further and higher than expected.

The thing is, sometimes both things can be true. You might have a 100x return in five years, and no matter how great the company is, its valuation may have reached its ceiling. In that case, even if it doubles or quadruples again, you should still keep enough to participate in that growth. But I think 100x outcomes are incredibly rare — I keep a list of companies that achieved 100x returns over the past 20 years.

Harry Stebbings: How many companies are on your list?

Mike Maples: There are about 100-plus exited companies on the list, and another 100-plus that haven't exited. I don't track many of them because I don't think they have real potential.

Harry Stebbings: So how many 100x cases do you have?

Mike Maples: Roughly three or four. Twitter was over 300x; Lyft was 205x; Applied came close to 100x; Twitch hit 94x. There are a few others that I think have potential to reach 100x.

Harry Stebbings: Would you sell Applied when it hit 100x?

Mike Maples: Yes, but you can't be selfish about it. We did sell some of our Applied position, but this was done in full collaboration with Qasar. I told him, "I'm not going to do this behind your back, or against your wishes. Can we find a way that works for both of us?"

This conversation needs to happen — you can't wait until the day the trade closes. You need to communicate early, ask: "Here's my thinking, does this make sense to you?" Qasar is a sophisticated partner, and he said, "I understand, you need to run your business and I have my responsibilities too."

Harry Stebbings: Completely agree. Usually the best founders understand this.

Mike Maples: Yes, as long as it's not a surprise and you're not being greedy.

Harry Stebbings: Or operating behind their backs.

Mike Maples: If you can be honest with the founder and say, "Do you want this investor on your cap table after the next round?" If so, we can structure something that achieves that goal without excessive dilution.

Harry Stebbings: Does your psychology change when you're in the carry?

Mike Maples: Hopefully not too much. But sometimes I also agree with Brian Singerman's view: When you're in the carry, you may lose the opportunity to make even more money.

Harry Stebbings: More often, people may focus on potential upside while ignoring risk. I've always believed that Sequoia succeeds in large part because they've already achieved so much that they're not afraid of downside risk. They always focus on the maximum possible value, and this fearlessness toward downside gives them broader vision.

Mike Maples: This ultimately comes down to the most basic principle: you can make money on the buy, and you can make money on the sell. What most people don't understand is that seed funds actually have an advantage over multi-stage funds when it comes to selling. This requires seed fund managers to have greater sophistication, rather than simply thinking "should I sell or not."

You need your own fact-based judgment. Why do I track 100x companies? I'm like a trainspotter, fascinated by a long list of train numbers.

Harry Stebbings: Do you like structured selling strategies? For example, Avi from Entrio — his strategy is to sell a third at the growth round, a third before IPO, and a third after IPO.

Mike Maples: It depends on the situation. But you can set a strategy while you're still "sober," saying, "If the following conditions occur, we might sell." When those conditions appear, you execute.

Founders Live in the Future

Investors Part with Love

Harry Stebbings: What's the most "not sober" decision you've made?

Mike Maples: Most mistakes happened in our early fund days, when we followed on in too many rounds that were never going to move the needle.

Harry Stebbings: What was the least sober decision?

Mike Maples: Our biggest failures weren't about that — they were failures of imagination, missing Airbnb and Datadog.

Harry Stebbings: But do you beat yourself up over missing Airbnb? It was a crazy idea at the time: the founders weren't from brand-name companies, they didn't fit mainstream investment criteria.

Mike Maples: I'm more focused on what I failed to see at the time, and maintaining rigorous reflection on that. This isn't self-criticism, but exploring whether we could have had a framework that would have led us to invest. We do this not just for Airbnb, but for all 100x cases — Marqeta, Zoom, we study them deeply.

Harry Stebbings: What did you learn from this research?

Mike Maples: We track certain metrics — if we had invested at seed, what would the return multiple have been? How long would it take? How much dilution? Then we apply our framework: did it have deep insight, did it capture an inflection point, did it have "Founder Future Fit"?

Harry Stebbings: What's "Founder Future Fit"?

Mike Maples: For example, Zoom's early positioning was as a video conferencing tool for the masses. At the seed stage, it was hard to see what inflection point it had captured. The initial vision was wrong. But founder Eric Yuan had spent 10 years on Cisco's WebEx team, thinking deeply about video conferencing the entire time, which made him excellent on "Founder Future Fit."

This concept comes from William Gibson, who said, "The future is already here — it's just not evenly distributed."

Great startup ideas never come from thin air. Founders live in the future, observe what's missing there, and make it real. This reminds me of Newton's story. Someone asked him, when the apple fell on your head, why did you suddenly think of gravity? Newton replied that he had been thinking about it all along. Founders who have "Founder Future Fit" are like obsessed trainspotters, constantly studying their domain.

Harry Stebbings: That makes a lot of sense. Every day I ask people, what's your insight? How do you see the world differently than others?

But the challenge is, many founders can't articulate it clearly. Even when they have such insight, I worry about missing it.

Mike Maples: It is difficult. Beyond whether the founder is excellent, we look at certain signals. First, did they capture an inflection point? Like Lyft — back then, the iPhone 4S came with a GPS chip, which made ride-sharing possible. Second, we ask founders: what do you believe about the future that is non-consensus but correct? Third is "Founder Future Fit."

Studying 100x cases made me realize that some signals are only obvious in hindsight, but we must learn to identify key points in the present. For this, we collect "time capsule" information on startups: the founder's background at the time, the pitch deck from when they raised, and all available information from that moment. Among these signals, "Founder Future Fit" is the most reliable indicator.

Harry Stebbings: The key being whether the founder's background aligns with what we believe successful founders in that space should have?

Mike Maples: Yes. I believe every great startup exists to bring about a future that is destined to arrive. And usually only one team is best suited to make that future happen, like Okta.

I met Todd McKinnon, and he said: "I worked at Salesforce for years. Early cloud computing users adopted Salesforce, and now they're starting to use other cloud applications. But they're going to run into identity management problems, and I'm going to solve that." He was VP of Engineering at Salesforce. Customers trusted him, and he knew these problems inside out. If anyone could do it, it was him.

Harry Stebbings: If anyone knew how to do it, it was him.

Mike Maples: Exactly. Todd's advantage was that he was living in the future alongside these customers. He had intrinsic motivation around this future, so he was more likely to know what to build. Second, it was easy for him to attract early followers because he was incredibly persuasive.

What we look for are founders who "live in a real future," are passionate about that future, and know exactly what to do.

Finally, we ask: Is this team the most likely team in the world to make this future happen fastest?

Harry Stebbings: Does this rule out founders who have never started a company before?

Mike Maples: No. Take Marc Andreessen — he was at the University of Illinois and had never run a business in his life. He was working in a computer lab. At that time, the internet was just starting to be allowed for commercial use, no longer restricted to academia.

Marc was trying to develop collaboration software for a group of researchers, so he started experimenting with early internet technologies. He created a browser. But was Marc targeting the browser market? Of course not. Marc didn't even know what a market was at that point. He was just trying to build the missing piece of the internet. He was trying to make the internet immediately more useful for himself and his team.

Why does this matter? Marc was essentially living in a "time machine." The computer he was using was similar to what everyone would use in the future. The network he was on was similar to what everyone would connect to. And the network protocols he was using were the kind everyone would soon be using. His knowledge of this space — his knowledge of the future — was more important than any business person's understanding of how to improve the status quo.

At the time, everyone assumed AT&T would build the Digital Highway, or Time Warner, or Microsoft Network, or AOL, or even the government. The common assumption was that this would be a top-down extension. Yet no one thought that some kid programming in a computer lab for minimum wage would have a better answer. It wasn't going to be top-down. It was going to be a bottom-up network, and that was the winning paradigm.

Marc's advantage wasn't his business experience. It was his knowledge of the future.

Marc Andreessen (far right) co-founded Netscape in 1994

Harry Stebbings: What's your biggest weakness when evaluating founders?

Mike Maples: My biggest weakness has always been being too optimistic that people can succeed. I fail to recognize how rare excellence is, how few truly great people there are with the willpower and resilience.

Harry Stebbings: If you don't like someone, would you still invest in them?

Mike Maples: Oh, absolutely. The two are completely unrelated. One of the defining characteristics of many great founders is that they're not particularly likable.

A disruptive startup is inherently an act of provocation. It's a rebellion against the current status quo. The more breakthrough it is, the more unpleasant it is. Many founders tend to be socially awkward because the existing system fights back, and that fight is not fair.

Harry Stebbings: What do you do when you lose trust in a founder? Say, a company you've invested in isn't meeting your expectations.

Mike Maples: I have a phrase: "Separate with love." I'll say, "Hey, it looks like I can't be very helpful here, and I'm not going to just sit here telling you you're not doing well enough. We disagree on a lot of things. If you change your mind and need my help, just let me know."

Harry Stebbings: Do you think winners are often in that "messy middle"? Because the ones that truly explode — Clubhouse, Hopin, BeReal — usually aren't sustainable. And the losers are obvious.

Mike Maples: But you can't do much about it either way. I've never seen a company fail after achieving product-market fit. In the early days, PMF is the only thing that matters.

Harry Stebbings: I don't quite understand. I've heard you say this, but I have several companies that achieved PMF and still didn't succeed. Clubhouse, for example. They had millions of daily users with long session times. I would argue that was PMF.

Mike Maples: I don't think they truly achieved PMF. They were just a flash in the pan, like a sudden solar flare.

Harry Stebbings: How do you define sustainable PMF?

Mike Maples: Interestingly, I was just talking to Robinhood co-founder Baiju Bhatt about this last week. He said, "When we achieved PMF at Robinhood, that's when I understood what PMF actually meant."

Harry Stebbings: I feel like it's a phase, a chapter in the book, and you need to keep turning the page.

Mike Maples: But to return to your point, I don't think I have much ability to help founders achieve PMF. There are some things I can do, mostly addition by subtraction.

I can remind them that regardless of what anyone says, PMF is the only thing that matters. Like football coach Vince Lombardi said, "Winning isn't everything, it's the only thing." PMF is the same — not everything, but the only thing that matters.

To get PMF, eliminate all distractions. I'll ask: "Last time we talked, you mentioned this was our bottleneck to achieving PMF. Is it still? What help can I provide there?"

Another thing is, I've heard some of your previous guests say that being a founder isn't a fun job. It's almost like being an artist. Sometimes it's more curse than blessing — something you're called to do. It's genuinely hard work, not fun at all. It's terrible.

Harry Stebbings: One of my biggest concerns right now is that we're seeing a generation of growth investors or Series A-focused funds that have now raised billions of dollars. These investors believe that dollar efficiency should be the same regardless of what stage a company is at or how much it's already raised.

So they decide, "Screw it, we need to put in $50 million, $75 million, even $100 million. Even if we're investing too early, we can see several times return." But once you've put in $100 million, these companies start doing a dozen different things, making your chances of exiting at $10 billion increasingly remote.

Mike Maples: Exactly. That's why I particularly admire some founders I've worked with, like Qasar. He had enough money to do anything he wanted.

Many CEOs have no one around them saying: "Hey, you're about to raise a huge amount of money. That's great, but we can't let ourselves get overconfident. We don't have PMF yet."

Harry Stebbings: Even if we do have PMF, if we raise $150 million, we have to find ways to spend it.

Mike Maples: What's worse, what usually happens is these companies raise a lot of money without truly having PMF, and they hire teams prematurely.

Suddenly they start doing all kinds of random things that don't actually drive PMF forward, and it destroys the company culture. They never develop the muscle memory of figuring out how to find the right customers, which customers to avoid, or which features belong in the strategy and which don't.

Harry Stebbings: What happens to companies that raise over $100 million, get valued at over $1 billion, but never truly achieve PMF?

Mike Maples: I think most of them won't be able to return money to preferred shareholders.

Harry Stebbings: But they have five to seven years of runway. So they keep going, and the fund managers just tell LPs, "It's fine, it's fine."

Mike Maples: The problem is, everyone in the entire industry has incentives to keep these projects alive. This goes back to the first point we discussed. My business is hard. Your business is hard. But it's not complicated. The key to investing is whether you can find companies that return 100x. Even just two or three such companies in a fund — that's enough.

Harry Stebbings: Have you ever encountered companies that succeeded without PMF?

Mike Maples: We had one company that was really struggling, almost out of money — CoTweet. This is a fun story. Speaking of American football, I have an expression called the "Forward Fumble."

Steve Anderson at Baseline was negotiating with CoTweet and asked what I thought the company should be valued at. I said, I don't know, they don't have many users. If I were you, $3 million valuation would be generous. Steve came back and said they accepted our offer. I thought, "What? Weren't you just asking my opinion?"

He said: "Come on man, you can't leave me hanging. Let's do this together." I thought: "Damn, I really like Steve, he's a smart guy." So I said: "Alright, I am somewhat interested in this, but I need to think about it. Anyway, the price is decent." I ended up deciding to invest together. I put in a few hundred thousand, Steve put in more.

Before long, CoTweet was almost out of money. Steve said: "Hey, we're running out of cash." I thought, oh god, how did I get suckered into this, this was the dumbest decision ever, swore I'd never do something like this again. Then, not long after, Steve said: "Looks like ExactTarget is going to acquire us." I'd never even heard of ExactTarget at that point. They were doing a stock deal.

I thought, well, at least we didn't go under. Though now I'm holding ExactTarget stock, some company I'd never heard of. Then ExactTarget acquired CoTweet, and ExactTarget went public. I thought, wow, they IPO'd, I wonder when I can sell these shares. Before the lock-up even expired, Salesforce decided to acquire ExactTarget. So we ended up making 23x.

It's like a fumble in American football. The ball's just bouncing around on the field, and it keeps going. Every time we thought, "I wish I could get out," we never actually got out, and it just kept moving forward.

04

Best Company, Founder, and Fund of 2024

Harry Stebbings: I love this topic. Let's look back at 2024. In your view, what's the company of the year?

Mike Maples: SpaceX. They're launching rockets into space with real frequency now. It's incredible. I don't have to strain very hard to imagine that one day they'll be the most valuable company in the world.

If you're the most important, dominant company in outer space, that's a big deal. For instance, North Carolina gets hit by a hurricane, the US passes a $42.5 billion broadband infrastructure bill, and as far as I can tell, nobody has actually built any broadband connections. And everyone's asking, "Elon Musk, can you help?" So he puts satellites up and provides free broadband.

If someone says the problem with SpaceX is that they're too powerful, that they dominate the skies — I think that actually highlights what they've accomplished this year. They have the ability to provide broadband anywhere in the world, pretty much at will, and they can launch all kinds of cargo.

For example, Baiju Bhatt's company is trying to build those satellites with solar panels that beam energy to Earth via laser, covering base stations. Well, who's going to launch those satellites into space? Obviously SpaceX. They'll handle the launches. Going forward, we may see SpaceX become the platform-level dominant supplier for the space sector.

Harry Stebbings: What do you think is the fund of the year?

Mike Maples: I'm going with 20VC. Dude, $400 million raised. That's incredible. $400 million is not a small number in Europe. You should be proud of yourself.

Harry Stebbings: I remember when we met years ago, I really wanted you to give me a job.

Mike Maples: If you'd come to the US, I definitely would have given you a shot.

Sometimes I find it interesting — you don't always realize what you've pulled off at the time. When you accomplish something, you might not stop and think: "Wow, that was amazing, I really did something big." Maybe you haven't fully processed what this $400 million raise means yet. But give yourself some time. Take it slow. Stop and think about it.

Harry Stebbings: I feel the weight of that responsibility. It's a massive amount of capital, and I'm incredibly grateful, but the real work is just beginning. Who's your founder of the year?

Mike Maples: Elon Musk, of course. For investor of the year, I'd pick Munger, because I think the world is going to miss him tremendously. Of all investors, I think Munger and Howard Marks have influenced my investment philosophy the most.

Harry Stebbings: How did Howard Marks influence you?

Mike Maples: His investment memos for Oaktree are just incredible. A lot of the ideas in Pattern Breakers come from this understanding that startups have to stand on non-consensus ground, and in a way that's massively, disruptively different.

He approaches it from second-level thinking — analyzing information that no one else in the market knows, then using that to generate above-market returns. Venture capital is premised on rejecting current rules, showing up with new ideas that shift where attention goes.

And the only way to achieve that is by being non-consensus and right. Only through being radically different can you create radical change. A lot of that kind of thinking I learned from Howard Marks.

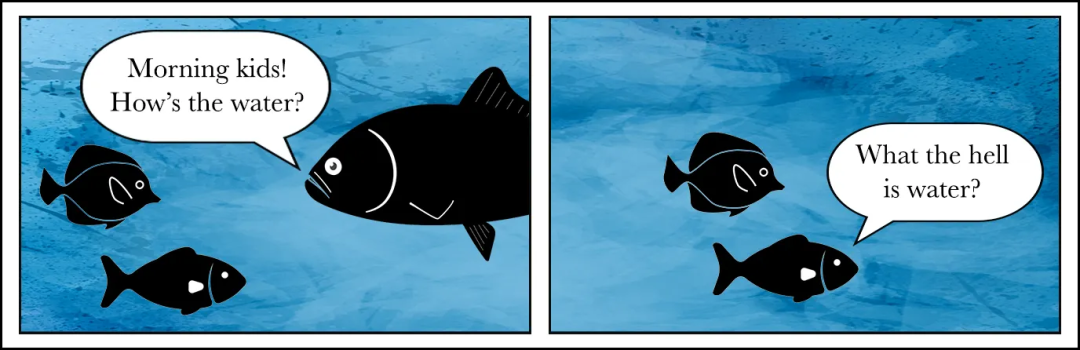

In an essay promoting Pattern Breakers, Maples referenced a story from David Foster Wallace's 2005 commencement speech: Two young fish encounter an older fish swimming the opposite way. The old fish says, "Morning, boys. How's the water?" The two young fish keep swimming. After a bit, one turns to the other and asks, "What the hell is water?"

Harry Stebbings: What's the exit of the year?

Mike Maples: I don't have a great answer for that one.

Harry Stebbings: I'll go with Loom, the $975 million exit. The timing was excellent.

Mike Maples: They really optimized their exit.

Harry Stebbings: What are your predictions for 2025? What will we see?

Mike Maples: I'm still very interested in Bitcoin's future. When I think about how the VC world views crypto, the smartest people I know are mostly focused on ETH or Solana. But when I look at Bitcoin, it feels like the thing hiding in plain sight.

I think one day Bitcoin will be worth more than gold, and more — a whole financial ecosystem and trading platform will form around it. If that's the case, Bitcoin has a lot of room to run, and I think you'll see a lot of startups building around it. That'll be very interesting.

Harry Stebbings: This morning I asked Reid Hoffman: end of 2025, what's the price of Bitcoin?

Mike Maples: I'm guessing $130,000.

Harry Stebbings: He predicted $200,000. What do you think happens with DOGE? Is it a success?

Mike Maples: To me, success means it changes the cultural understanding of accountability, what people consider acceptable standards. I don't think Musk is going to fire a bunch of people and change all the rules the way he did with Twitter.

Harry Stebbings: Walk in with a sink?

Mike Maples: He might actually do that.

Harry Stebbings: Someone might see a photo of him carrying a sink and think: "God, you've lost weight fast."

Mike Maples: Yeah. But it's not just DOGE. I think Joe Lonsdale's Cicero is great too.

The US government has a problem. There are agencies with huge budgets that consistently produce terrible results, and it's getting worse. At some point we need to reach consensus that if we're going to put money in, there should at least be clear goals. Hit the goals, get more funding. Miss them, get less. Can we agree on that? Republican or Democrat, can we at least agree to try to identify what the goals are and hold people accountable to them?

Can you imagine what the worst possible company would look like? Imagine: the worse it performs, the more money it gets. And the worst departments get the most funding, because they say, "The problem isn't that we're performing poorly — it's that you haven't given us enough money." That's how a lot of government works today.

So it's not just DOGE, what Musk or Vivek Ramaswamy are doing. What Lonsdale is doing matters too, because he's trying to bring this to the local level.

You can't solve these problems overnight, but you want to create a cultural mechanism where ineffective things naturally exit. If you can achieve a permanent shift on that, it would be a major breakthrough.

Harry Stebbings: What harmful elements in venture capital do you think need to gradually exit?

Mike Maples: There's just too much money in the market right now. That may shift somewhat.

Harry Stebbings: Yeah, I've talked to many LPs, sovereign wealth funds, new pension funds, endowments — today their allocation to venture capital is less than 3%, and they want to increase that to 10% to 15%.

Mike Maples: What most people haven't realized yet is that the exit market is cyclical too. In my career, there's typically a 15-year cycle where nearly half of all exit profits are realized in an 18-month to 2-year window.

Harry Stebbings: Horsley Bridge has done excellent analysis on the exit market. They've found that venture capital is indeed an extremely challenging asset class, but if you can exploit those very limited liquidity windows, it's also incredibly valuable.

Mike Maples: That's the venture business.

About once every 15 years, you get an 18-month to 2-year window, and if you want to do well, the secret is having a portfolio of really great companies during that period. The problem many large funds face is they raised money based on exit projections from 2020 to 2022. But there's a lot of evidence that won't happen again. We may go through a long dry spell before we see a market like that again.

Over time, these multi-stage funds will feel pressure to adjust their fund sizes. They'll adjust slowly, "deliberately" as they say.

Harry Stebbings: Fifteen years ago, having a $150 million seed fund was unthinkable. Now everyone takes seed funds over $100 million for granted. We used to never hear of trillion-dollar companies; now we have five or six.

Mike Maples: Yes, and another change is that a lot of people have forgotten what a seed round actually is. Now you see seed rounds reaching four to five million dollars. To me, the purpose of a seed round is that you have a deep insight about the future, you're taking enormous risk, and you're hoping to eliminate that risk.

The ideal seed round is one that provides just above the minimum viable capital and time to de-risk. Because that's when the company is at its riskiest and when capital is most expensive. Your dilution is greatest at the seed stage.

What founders should be doing in a seed round is demonstrating their unique insight about the future — I need to prove I'm right. Once you prove it, you've eliminated the company's biggest risk factor. What you've done is provide the most valuable contribution to the company, and then you'll raise at a higher valuation.

Harry Stebbings: I agree, but I have a different take. You prove you're right, but then you still need to scale it to enterprise level, and then prove you're right again.

Mike Maples: Actually, the more common scenario is that a lot of people raise four million dollars and then start doing a bunch of things without a clear plan.

What you should be saying is, I need to validate whether my insight is correct. If I can confirm my insight is correct, then the single biggest thing I can do is minimize risk. That's the most value-creating thing. If they raise more money after that, that's fine — that's a separate topic.

Then the question becomes: what's the value creation strategy at the Series A stage? But what happens now is that a lot of people raise four million dollars simply because that's the amount needed to dilute 20%. That's incredibly stupid. It's not a good way to start, and it hurts founders more than investors.

As a founder, the most irrecoverable resource is time. If you raise four million dollars, three years go by, you've done your seed round, hired a bunch of people, and then discover your insight was wrong — it's too late. If you're wrong, it's better to know within a year.

Harry Stebbings: But raising more money gives you more time to adjust and iterate. I've looked at cases like Klaviyo, UiPath, and ServiceTitan.

Mike Maples: These companies barely raised any significant capital before product-market fit.

Harry Stebbings: They really didn't. But if they had raised money earlier, would they have been more at ease in some way?

Mike Maples: I think they would have been worse off.

Harry Stebbings: They said the same thing. I asked every single one of them, and they all said: "No, absolutely not."

Mike Maples: You know, constraints are incredibly powerful in the early stages of a startup, and constraints are what help you understand how your company actually works. If you don't have the constraints of time, profitability, and finding desperate customers early on, your company just gets worse.

Harry Stebbings: I want to do a quick-fire round. I'll say something, and you tell me your immediate thought. What do you believe that most people don't?

Mike Maples: I think more people should pay attention to the core teachings of Christianity. I'm not saying this from a religious perspective, but a philosophical one.

Christianity introduced some important ideas to the world. One is the concept of time moving forward, rather than cyclical time. Another is human rights as inalienable rights. Christianity also introduced "unconditional love." This is hard to explain in just a sentence or two, but it basically means, "true love has no conditions."

Harry Stebbings: Do you believe true love has no conditions?

Mike Maples: I do.

Harry Stebbings: But if you don't set boundaries for your love, then other people will.

Mike Maples: Yes, boundaries and conditions are different. Conditions are like, my feelings are hurt, so I deliberately say hurtful things to get back at you.

If you believe in unconditional love, you would see that as completely irrational — because you love this person, so why would you deliberately hurt them? If they say something unkind to me, I can say: "Hey, it seems like something's wrong between us, we need to talk about this differently."

"Unconditional love" is an incredibly powerful way of thinking. It makes you realize that if you love someone, you always want them to do better. That doesn't mean you always agree with them, or that you always have to tolerate their bad habits, but you genuinely want them to do well. And regardless of what they do, you show up in that way.

There's one thing in Jesus's teachings that I particularly like, which basically means that from a distance, everyone is the same. That doesn't mean if someone is hostile to you, you don't fight back. You fight back when you need to.

But you approach it from a different perspective, thinking: "I regret having to hurt you, because you made a decision that left me no choice." But you try to avoid saying anything else hurtful.

This is a very profound idea, but a lot of people don't really understand it, and don't realize its immense philosophical power. But everything around us, most of what makes up the Western world, comes from Christianity. The Jesus I'm talking about is not as a religious figure, but as a philosopher.

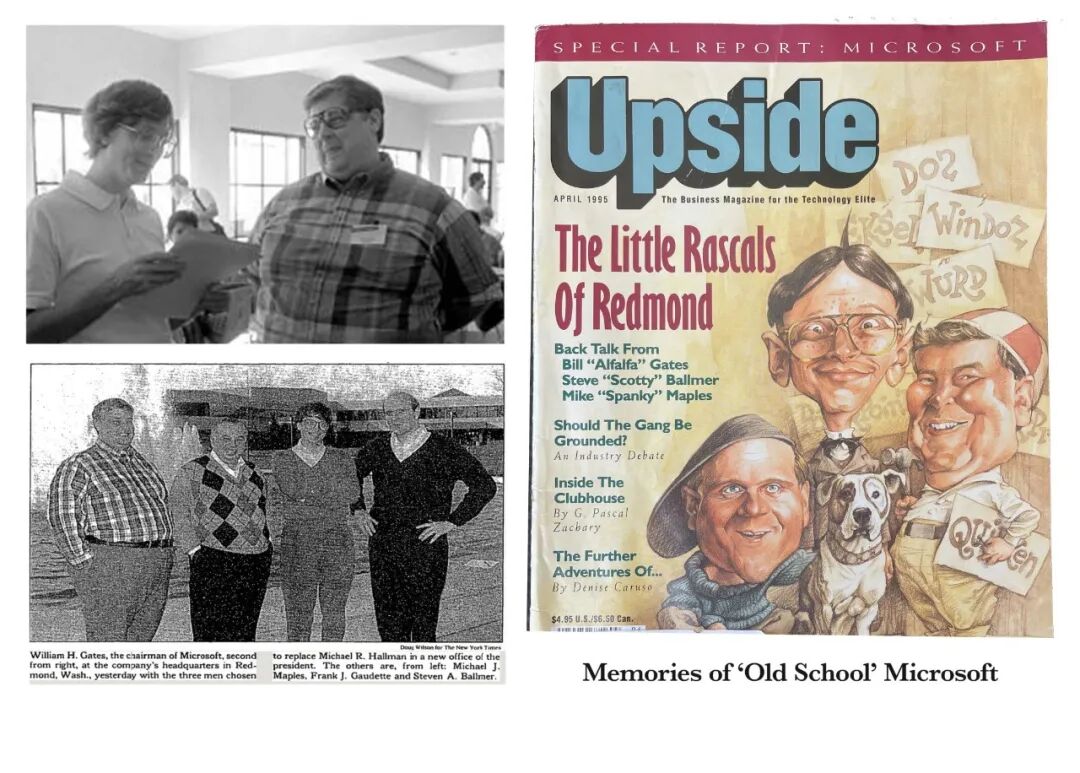

Harry Stebbings: I've seen a photo of your father, an early Microsoft employee. What's the biggest lesson you learned from him?

Mike Maples: That's another great question — it's to do your best.

Have you read The Wealth of Nations? It talks about the principle of comparative advantage. Most people misunderstand competition. You have your DNA, I have mine, and no one in human history has ever had DNA identical to someone else's. That means each of us is a node in the network, completely unique.

Every person in the world, whoever they are, has some comparative advantage. The reason many people fail is that they try to be the strongest.

What I learned from my father is: what you need to do is not be the strongest, but be your best self.

I think Peter Thiel is incredibly smart, but I could never surpass Peter Thiel in seed investing by studying Strauss, Goethe, Nietzsche. He would beat me at that game. But if the game is about who is better at developing the investment philosophy of seed rounds, at defining what makes seed rounds and startups great, I think I could beat anyone at that game.

It was my father who made me understand that as a person, you have an internal drive to provide value that the world needs, and to be compensated for it. One way to respect the limited time in your life is to strive every day to be the best version of yourself.

Mike Maples's father (bottom left, first from left) joined Microsoft in 1988 as Head of Applications

Harry Stebbings: Last question — this one's a bit hard but very revealing. How did your parents raise you? Were there deliberate choices you made to raise your children differently?

Mike Maples: That's a good question. One thing I think I could have done better is getting my kids to play outside more, to do more sports.

My father was extremely rational, almost buried in computers. Every topic we talked about was about computers, the computer industry, programming — he had no interest in sports. I wish I had encouraged my kids to do more of those things.

Harry Stebbings: Mike, it's been such a pleasure chatting with you. Thank you so much for joining.

Mike Maples: Thank you for your patience in listening to me.

Translated by Cindy

Edited by Wendi

Recommended Reading