ZhenFund's Yusen Dai: A Guide to Entrepreneurship, Investing, and AI for Young People

Abundant energy, an intense desire for success, and a fearless spirit of innovation.

Z Talk is ZhenFund's column for sharing perspectives.

Entrepreneurship isn't for everyone. It demands extraordinary courage, unwavering conviction, and relentless effort. These qualities are precisely what make success in entrepreneurship possible.

Under the theme A Young Person's Guide to Entrepreneurship, Investing, and AI, ZhenFund Managing Partner Yusen Dai shared why the fund focuses on technological innovation, why it believes young founders hold the advantage, and how it identifies and invests in promising entrepreneurs amid the wave of technological innovation.

Here is the full transcript.

01

Entrepreneurship: A Lifestyle for the Few, a Game for the Brave

These days, when people hear "entrepreneurship," it probably doesn't feel as hot as it did ten years ago during the "mass entrepreneurship, mass innovation" era. But I believe as long as you carry that entrepreneurial spark in your heart, opportunities are always there.

We're in different cycles. When times are good, don't get too impulsive or blindly optimistic. When challenges pile up, take a breath — there's no shortage of opportunities if you look closely.

But entrepreneurship really isn't for everyone. Because at its core, it's a lifestyle choice — and one that only a minority will choose. As my senior, Meituan founder Xing Wang, once put it: "There aren't actually that many people who truly crave success with extreme intensity, and among them, even fewer are willing to pay an extraordinary price to pursue it."

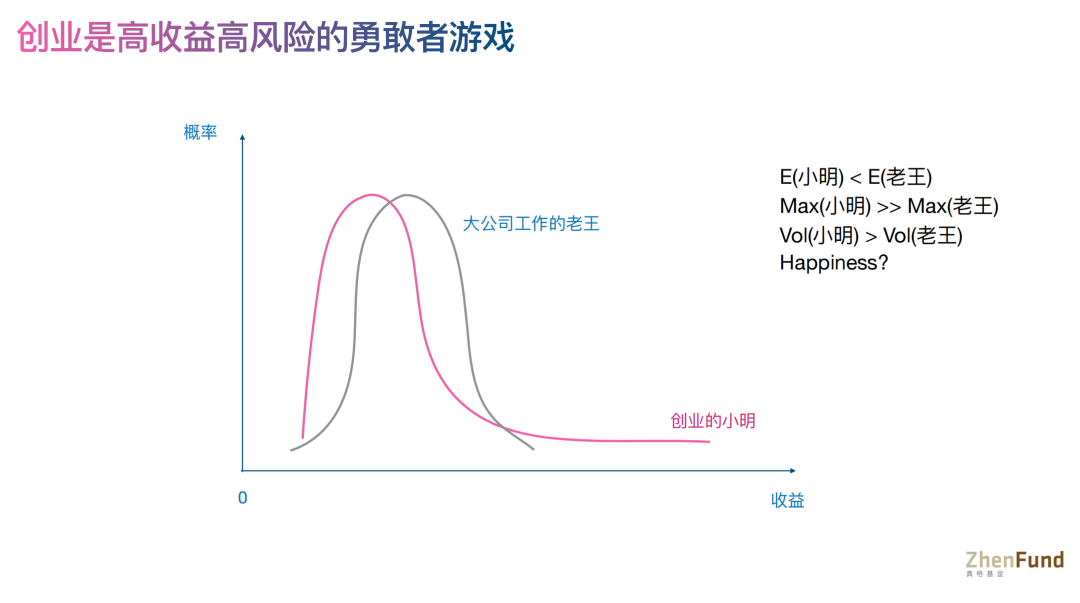

I'd like to illustrate entrepreneurship in a particular way, using a coordinate system built on probability of success and magnitude of return.

Of course, we know entrepreneurship isn't just about making money. Impact and social responsibility matter too. But let me focus on returns for now.

Lao Wang, who works at a big company, and Xiao Ming, who chose to start a company — these represent two fundamentally different lifestyles, two different probability distributions.

Working at a big company roughly follows a normal distribution — a decent expected value, but the extremes typically aren't that high.

On the entrepreneurial side, Xiao Ming faces the risk of losing everything. But if he succeeds, the payoff can be substantial.

Comparing the two, Lao Wang's expected return is higher than Xiao Ming's. But Xiao Ming's potential upside — the extreme positive outcome — far exceeds anything Lao Wang could achieve. At the same time, Xiao Ming's volatility, what we'd call "volatility," is much greater than Lao Wang's, which means the entrepreneur's life tends to be more demanding.

Entrepreneurship is a lifestyle choice you need to think through carefully. It's a game for the brave. That's why we keep emphasizing the importance of finding people who are truly suited for it.

02

Why Young Founders?

So why do we engage with young people? Why do we support young founders, even going out of our way to visit universities and share with students?

Because we firmly believe that entrepreneurship, in many ways, belongs to the young. Paul Graham, founder of Y Combinator, once said: "Young founders have some inherent advantages."

First, they have energy to spare — they can endure hardship and pull all-nighters without flinching. Second, having little to lose makes them hungry for more, giving them an intense drive to succeed.

Third, being immersed in a campus environment thick with entrepreneurial energy makes it easy to meet like-minded people and find co-founders. Most crucial is the "ignorance that breeds fearlessness" — many breakthrough innovations emerge precisely because their creators either didn't know enough about how things were "supposed" to work, or knew but simply weren't afraid, sparking novel ideas.

Today, any list of the world's hottest startups includes OpenAI. Sam Altman, one of OpenAI's co-founders, said in a YC talk that he wants to invest in young people with exceptional potential — not those with long track records that have already proven to be mediocre.

So we focus on potential. We believe entrepreneurship is something to try early, and young founders often have the edge.

03

Pursuing Technological Innovation: Mutation and Value Creation Through an Investor's Lens

Our primary investment theme is technological innovation, or "tech innovation" as it's commonly called. In my view, tech innovation is the wellspring of value creation in our era.

Looking from where we stand now, the tech innovation space holds even greater opportunities. It's also the main focus for most tech entrepreneurs and for us venture capitalists.

Why do I say this? For one, the scale has grown larger. Artificial intelligence represents a disruption opportunity across all industries — perhaps the most concentrated period of industrial transformation we'll see. This is undeniably a revolutionary, massive opportunity.

For another, we can clearly feel that the pace of innovation keeps accelerating. Twenty years ago in the internet era, a major breakthrough might come every few years. Now, in many fields, we're seeing various breakthroughs every year, even every six months.

We can observe that the trajectory of much tech innovation follows a curve: slow growth initially, then sudden explosive expansion.

The key question is: when standing at that inflection point before explosion, can we敏锐ly perceive the coming surge? This is where traditional investment thinking and frameworks often stumble when confronting disruptive innovation.

A common pattern emerges: "overestimating in the short term, underestimating in the long term." Why does every new technology trigger market bubbles? Because people assume the tech will deliver massive value immediately. Yet we routinely underestimate its long-term impact. We're accustomed to thinking linearly, but real technological change tends to be exponential.

In tech innovation, investing in the leading companies becomes especially critical. Looking back, China's internet giants were all category leaders. Other companies ended up delisting. This amply demonstrates the asymmetric returns characteristic of tech investing.

However, precisely because of this feature, many people mystify tech innovation — treating it as unknowable, patternless, a matter of pure luck, or simply spraying and praying.

We disagree. While luck certainly plays a role in tech innovation, anything that objectively exists can be understood and studied. So we've been working to identify patterns in innovation.

As investors, when we think about entrepreneurship, we're studying where mutations occur. This is why we're so drawn to tech innovation.

Because when mutation happens, it creates enormous value and profoundly reshapes existing structures.

04

"Look Backward": Putting Our People-First Principle into Practice

What makes our fund distinctive is our focus on investing in people.

We believe the core of angel investing is backing exceptional talent. Even with a flawed initial direction, outstanding founders can pivot quickly and find the right path. Conversely, even the right direction won't save a team that isn't exceptional enough to outcompete others.

What does investing in people mean? It means having the conviction to invest before you fully understand what they're building.

In public market investing, you typically buy after seeing the financials — "seeing is believing."

For us, we invest because we believe in the person — "believing is seeing."

Many investors claim they can predict the future and invest based on such forecasts. We don't think we can predict the future.

What we want to do is look backward — examine whether this person has demonstrated exceptional qualities in the past. If they match the traits we value, we're willing to back them. We call this "look backward," not "look forward."

We often encounter this: we invest in someone, initially have no idea what they're doing, then a few years later it suddenly becomes hot, a major trend. So we realized: invest in people who can create trends, not those who merely chase them. This is the most straightforward, hard-won lesson from our people-first approach.

Adhering to this "people philosophy," ZhenFund developed its four-quadrant theory of founders — categorizing entrepreneurs as "Young Geniuses," "Serial Veterans," "Operators," and "Tech Scientists."

"Young Geniuses," for instance, bring unique insights to a field precisely because of their youth. Globally, think Bill Gates or Mark Zuckerberg. In China, Moonshot AI's Zhilin Yang fits this type.

"Serial Veterans" are repeat founders. "Operators" are people who've truly run core businesses at major companies. "Tech Scientists" are scientists who've mastered core technology while possessing strong commercial acumen.

05

The "Crossing the Chasm" Strategy

A renowned investor once said: "If you believe something is bound to happen eventually, try it every three years." From an investor's perspective, that might mean making a related investment every three years.

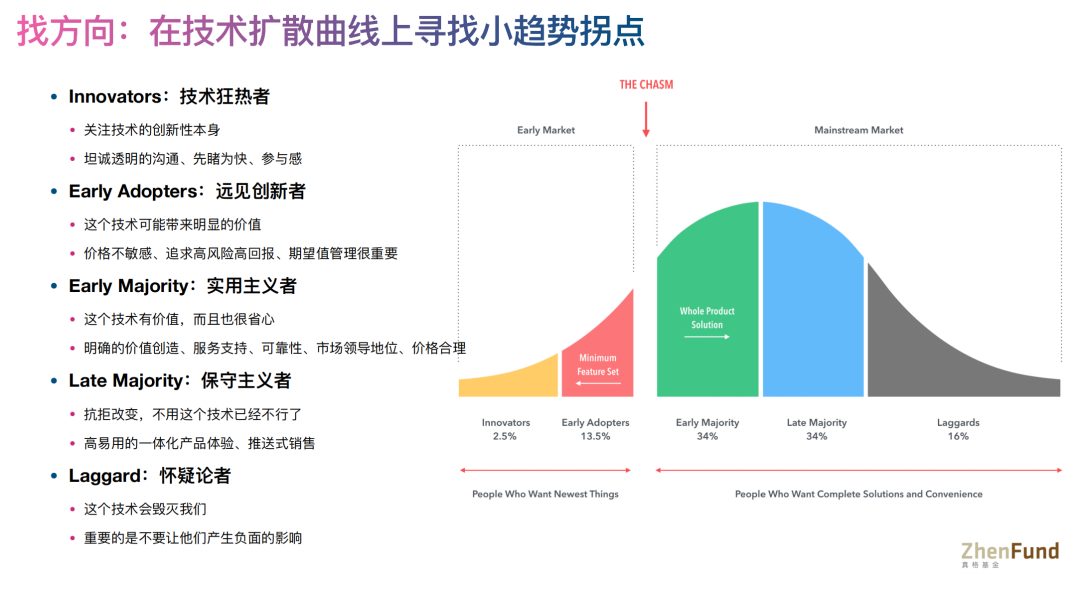

If you invest every three years, when is success more likely? This brings us to the "crossing the chasm" framework. The corresponding curve is called the "technology adoption lifecycle," or technology diffusion curve. Terms like "innovator," "early adopter," "early majority," "late majority," and "laggard" — I've attempted my own translations for these.

The first group, "innovators" — the technology enthusiasts. These are hardcore geeks obsessed with tech itself. What matters to them is the technology. As long as it's novel, they'll try it even if it's difficult to use, expensive, or currently useless — simply because it's fun and new. They want to be first to experience it.

The second group, "early adopters" — the visionary innovators. They're not particularly price-sensitive; paying more is fine if the product delivers value. They're willing to try new things first, but only if they see potential worth.

Typically, these two groups are combined into the early market — the stage inhabited by "innovators" and "early adopters."

The third group, "early majority" — the pragmatists. Their defining trait: the product must actually work well. Not "might work well," but must deliver clear value. It can't be too complicated to use; it needs stable performance without frequent failures. They prefer products with clear market positioning and care about reliability, supporting services, and design.

The fourth group, "late majority" — the conservatives. These users demand extreme simplicity and integration — preferably all in one product. Ideally, the product comes to them; they won't seek it out. They want it to be ubiquitous, unavoidable.

The final group, "laggards" — the skeptics. They believe the technology is harmful, poses significant danger, and refuse to use it. Fortunately, this is the smallest segment.

Within this curve of five groups lies a chasm, positioned between "early adopters" and "early majority." What does this mean?

Initially, "early adopters" think the product might be useful, so they adopt it. But after using it, they find it fails to deliver real value, and the usability problems persist — they fall into this "pit."

This makes mass user acquisition difficult. Financially, returns may disappoint. From an investment standpoint, good outcomes become harder to achieve.

Let's look at a successful chasm-crosser: how did Tesla do it?

Early on, Tesla launched the Roadster sports car targeting "innovators," aiming to prove electric vehicles could be cool with great driving dynamics.

The subsequent Model S and Model X provided value for "early adopters" — rapid acceleration, massive touchscreen, Autopilot capabilities. But charging was inconvenient, range anxiety was real, and prices were high — significant usability barriers. Tesla crossed the chasm by enhancing value and reducing costs, successfully launching the Model 3 and Model Y to capture mainstream users. This illustrates how an industry moves from early to mainstream markets and creates massive value.

06

Old Wine in New Bottles: Where Do AI-Era Startups Find Opportunity?

In today's booming AI era, many people wonder: it seems like AI is all about big tech's opportunity. Does this mean in AI, all the advantages belong to the tech giants?

Actually, this isn't unique to the AI era. Looking back at every previous technological revolution, people had similar doubts. To address this, let's think deeply about how historical tech transformations gave rise to great companies.

I've summarized this and found that every tech revolution involves an "old wine in new bottles" process — new technology is typically used to solve old problems.

Take the early internet: information used to travel by physical mail; with the internet came email, near-instantaneous delivery. Yet while new tech addresses existing needs, truly massive value creation and transformative change usually come only when the technology deeply permeates every aspect of social life. This is when entirely new business models emerge with enormous growth potential. And these new business models are mostly pioneered by startups.

In the current AI era, I see a similar pattern — again, "old wine in new bottles." AI is handling many tasks people previously did themselves: writing code, drawing, drafting articles, and so on. This period does create opportunities for both new and established companies.

But I believe the truly significant opportunity lies in what happens as AI penetration deepens. Currently, the vast majority of value in this world is created by humans. But if most GDP eventually comes from AI, existing human business models will be fundamentally transformed. And in this process, I see enormous opportunity — one that will very likely require startups to uncover and seize.

07

Choosing a Direction: Finding the Intersection of Mega-Trends and Micro-Trends

So how should founders choose their direction? I have a simple framework: find the intersection of mega-trends and micro-trends.

What's a mega-trend? Simply put, any trend that will last ten years or more. In China's case, the 40-plus years since reform and opening have been driven by several mega-trends: urbanization, industrialization, marketization, informatization, globalization — these are all mega-trends.

But aligning with mega-trends alone isn't enough. Tech innovation often develops through disruptive mutations. If you're in the pre-explosion phase, it's grueling work. This is where micro-trends come in. Where do micro-trends typically come from, and how do we spot them?

Micro-trends usually emerge from changes in 1% to 5% of the population. If something has only 100,000 users in China, the group is too small to matter much. But if something has a billion users like WeChat, there's no opportunity left in building something similar. For us, when something reaches roughly 10 million users, that's often where significant opportunity lies.

How do micro-trend inflection points typically appear? Usually, some new development triggers the shift.

New technology emerges, like GPT bringing entirely new experiences. Or new demographics appear — Gen Z, Gen Alpha, each generation with its own culture and social circles. Or new markets, like the下沉市场 (lower-tier market): when Tmall and JD.com already dominated e-commerce, Pinduoduo targeted下沉市场 and rose. This represents micro-trend change driven by new demographics and new markets.

I believe the best approach is finding where mega-trends and micro-trends intersect. This ensures you're riding the era's wave while becoming a trend-leading "pioneer" rather than a prematurely early "martyr."

08

The Art of Recruiting: Trust, Complementarity, and Attracting Talent

Recruiting is fundamentally about judging people, so we've always believed people are paramount in entrepreneurship. However, recruiting typically happens in stages. Early on, the specific project matters less than mutual trust.

The second stage is finding complementary people. "Complementary" covers both capabilities and personality. This kind of well-rounded complementarity is crucial.

Later, at the third stage, you need to find people better than yourself. As a founder scales the company, they often become the bottleneck. At this point, several things become critical:

First, can you identify people who are stronger than you in certain areas?

Second, can you attract these stronger people to join?

Third, can you retain and effectively deploy them? We often see: a good startup that recruits a strong person levels up; one that fails to do so stagnates or declines.

Truly exceptional founders have the ability to attract people far above their own level. So sometimes people feel like outstanding founders are "hyping" others. But look at Elon Musk, Steve Jobs — which of them lacked the ability to inspire others, to make people want to follow? So for ourselves, if we want to attract people to build with us, developing our leadership and personal charisma is genuinely important.

And in this process, there's something we must emphasize — especially in China's entrepreneurial environment: startups must be crystal clear about who's in charge. Authority, responsibility, obligations, and rewards all need to align.

This brings us to "compromise." On one hand, everyone recognizing a single leader is itself a compromise. On the other, the leader being willing to share rewards with co-founders — that's also compromise.

09

The Mechanics of Fundraising: Equity, Investor Selection, and Key Principles

Relatively speaking, fundraising is easier than recruiting or choosing direction — at least for excellent founders genuinely trying to build something, initial funding usually isn't too hard to secure. Still, there are things to watch.

First, equity allocation. We're strongly opposed to equal equity splits. We believe responsibility, authority, and rewards should be unified; equal splits usually mean people haven't thought these issues through, haven't had the hard conversations upfront. After all, dividing money is sensitive. Best to clarify everything from the start, get everyone's buy-in, then begin.

How to grant equity? My view: equity is a company's non-renewable resource, so treat it with extreme care.

We frequently encounter this: initially everyone thinks the company is small, so they hand out equity casually. Later, they find "free riders" — people holding equity without contributing much. Once the company grows, equity becomes precious, yet there's little left to grant to new, genuinely capable joiners.

So our advice: if money can solve it, don't use equity. For temporary relationships, avoid giving equity. Cherish what you hold. Consider what that equity will be worth when the company scales — if the company doesn't grow, more equity given is meaningless; if it becomes huge, equity value becomes substantial.

Only grant meaningful equity to those who will truly walk the long road with you as genuine partners.

On finding investors: if you have options, seek investors who share your vision. When selecting investors, you need deep understanding of them and their fund — whether your values align, whether personalities mesh, so that when problems arise, you can tackle them together.

On fundraising principles: first, raise enough money.

Second, even if market conditions improve later, don't raise too much — too much money can make you "dumb."

Truly skilled founders are artful spenders. They can spend a lot, but not burn blindly. They put money precisely where it matters, maximizing every dollar's impact. Also: don't fundraise for fundraising's sake. Don't assume that raising money at a high valuation makes you wealthy — that's all illusory.

Fundraising is a means, not an end.

10

The Four Stages of Entrepreneurship

Entrepreneurship doesn't happen overnight. It unfolds across several distinct stages.

The first stage is finding direction. Here, what matters most is determining what to do. You need a vision — something you genuinely want to build. Then iterate rapidly, test quickly, pivot if needed, and find the right direction as fast as possible.

Once direction is found, and it's a good one, you likely won't be alone — others will spot the same opportunity. Then it becomes a race to see who runs faster: the growth stage.

Especially in internet, there's the concept of "growth hacking" — taking growth extremely seriously. This stage tests fundraising capability and market expansion. Most founders face existential crisis here.

If growth is navigated successfully, the company is doing quite well. But new problems emerge: management can't keep up.

Because the company grew so fast, so "barbarically," efficiency was high but management was weak.

This is actually the most dangerous phase. Success can make founders feel invincible, that management doesn't need improvement. Yet this is precisely when team building, management elevation, systems, and culture matter most. If this stage is handled well, management catches up, the company becomes truly formidable — potentially a $10 billion-plus company.

But then new challenges arise: can you sustain innovation? Of course, maintaining innovation involves many theories and methods — innovation strategy, talent platforms, external investment and expansion, change-driven transformation, building second curves. These become another topic entirely, as different stages of entrepreneurship demand very different capabilities.

Finally, is entrepreneurship the lifestyle we want to choose? Is it truly a game for the brave? Not everyone needs to become an entrepreneur.

But if you decide to do it, then do it for real.